Chapter 24

TRUMP

O n July 21, 2016, a burly figure strode across a podium dressed seemingly to inspire memories of Captain America, Citizen Kane or a 1930s fascist rally. The man in the spotlight was there to deliver a speech with which he meant to change American history. 1 It was a flaming denunciation of the Obama administration. He evoked an alarming image of America harried by terrorism, violence and chaos. He told his audience 180,000 illegal immigrants with criminal records were that very night “roaming free,” terrorizing and murdering innocent Americans. Meanwhile, lives were getting tougher. “Household incomes are down more than $4,000 since the year 2000. Our manufacturing trade deficit has reached an all-time high—nearly $800 billion in a single year. The budget is no better. President Obama has doubled our national debt. . . . Yet, what do we have to show for it? Our roads and bridges are falling apart, our airports are in Third World condition, and forty-three million Americans are on food stamps.” Why were things this bad? Because “big business, elite media and major donors” had all conspired for decades to rig the system. Now those same forces were lined up behind his opponent. “She is their puppet, and they pull the strings.” At this point the crowd reacted with chants for her to be thrown in jail. Against this elite conspiracy the man in the spotlight promised to fight for the “neglected, ignored, and abandoned . . . the laid-off factory workers, and the communities crushed by our horrible and unfair trade deals . . . the forgotten men and women of our country. People who work hard but no longer have a voice. . . . History is watching us,” he declared, “waiting to see if we will rise to the occasion, and if we will show the whole world that America is still free and independent and strong.” His answer boomed around the hall. He promised one thing: “to put America First. Americanism, not globalism, will be our credo.”

If someone had written a script as to how an economic crisis and democratic decay would lead to a nationalist backlash in the United States, this denouement might have seemed a little cartoonish. But this was no script. It was real, or at least it was “reality.” The man giving the speech was the same property tycoon and TV personality who had helicoptered onto the Turnberry golf course in Scotland to revel in Brexit a month before. Donald Trump was running for election as president of the United States on the Republican ticket against Hillary Clinton. Trump’s closest confidante was his daughter Ivanka. And if you liked her convention outfit, Macy’s department store was promoting her clothing line on Twitter. 2

The following day, during a press conference in the Rose Garden, President Obama attempted to restore a sense of normality. “[T]his idea that America is somehow on the verge of collapse, this vision of violence and chaos everywhere,” the president told the press, “doesn’t really jibe with the experience of most people. I hope people the next morning walked outside and birds were chirping and the sun was out, and this afternoon, people will be watching their kids play in sports teams and go to the swimming pool and folks are going to work and getting ready for the weekend. And in particular, I think it is important, just to be absolutely clear here, that some of the fears that were expressed throughout the week just don’t jive with the facts.” 3

In July 2016 Obama’s riposte seemed to many like a welcome dose of common sense. With hindsight, the president’s lines talk about “chirping” birds and kids enjoying a long, hot American summer read differently. They remind us of the complacency that would cost the Democrats the election. The Clinton team did not take seriously the view of modern America summoned up by their opponent. On November 8 Trump imposed his reality on theirs. Though Clinton ran up huge numbers in New York State and California and won the popular vote, it was Trump who gained a slender majority of the electoral college and would become the forty-fifth president of the United States.

It was the most disorienting event experienced by the American political class in generations. The unthinkable had happened. The Democratic establishment had been confident about 2016. Admittedly, since 2008 congressional elections had not gone well. But 2012 entrenched the Democrats’ belief that the presidency was theirs for the taking. 4 Under their stewardship America had weathered the crisis. As Americans returned to postcrisis normality, the inevitable dominance of the more modern and diverse Democratic Party would make itself felt. American society had deep problems, no doubt. The economy was not running at the speed they would have liked. But once Clinton and the latest generation of Democratic Party technocrats got back on track, there was nothing that could not be fixed. Obama’s Affordable Care Act and Dodd-Frank were starters. What America needed was more of the same. Against this, what did the Republicans have to offer? Not only was Trump personally unfit for high office but his dark vision of American crisis was out of touch with reality.

As it turned out, 2012 had been misleading. Obama ran as a moderately popular incumbent, and his Republican opponent, Mitt Romney, a Mormon governor of Massachusetts with a much-trumpeted track record in venture capital, could hardly have been less well suited to harnessing popular discontent. Four years later Obama was out of the picture and the Republican field was wide open. As a result, the presidential race of 2016 turned out to be more about the financial crisis of 2008 than 2012 had been. The upshot was explosive and unpredictable.

I

The most obvious mark of the financial crisis of 2008 on the election of 2016 was the fact that Bernie Sanders was a serious contender for the Democratic Party nomination. Sanders wasn’t even a member of the party. He was a self-declared democratic socialist. He was a confirmed foe of Wall Street. In 2008 he had voted against TARP. He called for the big banks to be broken up. He wanted bankers jailed and a return to New Deal–era banking regulations. The spirit of Occupy energized his troops. With Independents and young voters he was wildly popular. 5 The fact that Sanders was viable as a candidate reflected the finding of opinion pollsters that among American voters under the age of thirty, more had a positive view of socialism than of capitalism. 6 The anger of 2008 was still very much alive and Sanders fanned it. Hardly a rally went by without crowds shouting their indignation at the bailout. Regular Americans were still struggling back from the recession. As Sanders pointed out in a typical flourish in September 2015, applauding the Fed’s decision not to raise interest rates: “At a time when real unemployment is over 10 percent, we need to do everything possible to create millions of good-paying jobs and raise the wages of the American people. It is now time for the Fed to act with the same sense of urgency to rebuild the disappearing middle class as it did to bail out Wall Street banks seven years ago.” 7

Harping on the historic injustice of 2008 not only played to “Bernie’s” base. It was an excellent weapon with which to beat the front-runner, Hillary Clinton. Clinton was the consummate insider. She was a former secretary of state and senator for New York, and as such irredeemably entangled with Wall Street. 8 By the spring of 2016 Clinton and Sanders were dueling over Dodd-Frank. Sanders wanted to go back to the decisive moment in 2009 and do it right, to break up the banks. Clinton’s answer was that Dodd-Frank should be rigorously enforced. This teed up Sanders to ask whether Clinton’s reticence had anything with the $600,000 in fees she had collected giving speeches for Goldman Sachs. Would she release the transcripts? 9

For the Left, Clinton’s Goldman Sachs speeches were what her Libya e-mails were for her opponents on the Right: a further sign of her untrustworthiness. How deeply was Clinton entangled with the bank now better known as the “vampire squid”? 10 Even the New York Times called for Clinton to release the text of the speeches. Weighing the issue, her campaign managers decided that Clinton’s words were not, in fact, fit for public consumption. She would look too friendly to the banks. 11 We know this because starting in July, as she closed in on winning the nomination, internal memos from the Clinton campaign began to be dumped en masse in WikiLeaks folders. Who, in fact, compromised the security of the Democratic Party machine was to become a matter of complex technical and legal dispute. 12 But at the time the conviction rapidly took hold that it was down to hackers with ties to Russia. 13 Was the mounting confrontation with Putin, which had reached a new pitch in intensity over Ukraine and Syria, blowing back on the United States, and on Clinton in particular? Behind the scenes America’s intelligence agencies scrambled to uncover the extent of Russian interference in America’s presidential election. On the basis of sources inside the Kremlin they were forced to conclude that given Clinton’s well-known hostility to Putin’s regime, Moscow was doing what it could to derail her campaign. Even if the Russians could not change the outcome, they would do their best to undermine the legitimacy of America’s already fragile political system. Moscow was serving notice that two could play at the game of regime change. By the fall Obama was seriously weighing his options, including sanctions that would, in the words of an anonymous administration source, amount to “cratering” the Russian economy. 14 That scenario did not unfold, because Putin pulled back. But it was clear that this would be no ordinary election. Quite how unusual it would be was becoming clear on the Republican side.

Whereas the battles within the Democratic Party had a clear-cut, Left-versus-Right logic, and the establishment maintained its grip, what was happening to the Republicans was more disorientating. The GOP was out of control. In truth, the party had never recovered from the shipwreck of the late Bush presidency, the shock of 2008 and the Tea Party mobilization triggered by the financial crisis. The splits within the party that had precipitated the congressional budget crises of 2011 and 2013 were wider than ever. In 2013 the shutdown was called off as default loomed, but the Right had had their taste of blood. First, in June 2014 they unseated the leader of the House, Eric Cantor, in a primary. Then, in October 2015, the ill-fated John Boehner was ousted as House Speaker by a mobilization of the right-wing Freedom Caucus. 15 With the party in turmoil, the establishment candidates who had been expected to dominate the presidential primaries—figures like Jeb Bush—rapidly faded. It was the darlings of the Right who surged to the fore. The “dark money” of the billionaire donors, led by the Koch brothers, swung behind Texas senator Ted Cruz. 16 But it was Trump who took the votes of the Republican base by a majority of almost two to one. 17

If Jamie Dimon quipped that to make sense of Dodd-Frank one needed the services of a lawyer and a psychiatrist, the same is no doubt true of the business of deciphering Donald Trump. But historians can contribute too. 18 Trump offered to a bewildered present a throwback to an earlier era. Born in 1946, the same year as Bill Clinton, Trump would take office at seventy years of age, recycling a rancid version of the baby boomer narrative, which in the 1990s had still seemed fresh. Trump’s racial attitudes reflected the animosities of the era of civil rights, desegregation and New York in the 1970s. His boorish manners and sexism echoed the Manhattan party scene of the 1980s, when bond traders toasted one another as “big swinging dicks.” The sense of national crisis that drove his campaign was a reflux not so much of the recent past as of the first moment when modern Americans felt the world changing around them—the late 1970s and early 1980s. The trauma of defeat in Vietnam, America’s urban crisis and angry Japan bashing—thirty years on Trump was still harping on those fears, but now transposed onto new enemies: China, Islam and undocumented Latino immigrants.

His main shtick was that he was a businessman, a deal maker. And because his business was real estate, Trump lived the American business cycle close up. As Hyman Minsky, the legendary analyst of financial crises, observed already in 1990, Donald Trump was the very epitome of a Ponzi scheme capitalist, living hand to mouth by borrowing against the expected appreciation of his assets. 19 As a result, crises punctuated Trump’s career. He was hit hard by the early 1990s recession, almost losing his business. By 2008 he was less vulnerable, having diversified into media and branding. But his real estate exposure was still significant. Indeed, he was seeking to increase it. In 2006 he started a mortgage brokerage and announced plans to open a mortgage lending business. Luckily for Trump, neither got off the ground. By 2008 his casino business was failing again and would ultimately close. But Trump’s real vulnerability was a gigantic condo development in Chicago. 20 It was a spectacular project, the tallest building to be built in the United States since the Sears Tower, and sales had originally gone well. But in 2008 Chicago condo sales stopped dead. By the fall it was clear that Trump and his business partners were in trouble. Since his bankruptcies of the 1990s, Trump was no longer on good terms with the major American banks, so the Chicago project got its funding mainly from Deutsche Bank’s North American real estate arm. In the first week of November 2008, as Barack Obama celebrated his election victory with his adoring Chicago base, Deutsche and Trump went to war. Deutsche sued for $40 million, for which Trump was personally liable. Trump responded with an astonishingly audacious legal broadside. He claimed that the greatest financial crisis since 1929 constituted force majeure, akin to a natural disaster. He therefore demanded more time for the project to pay off. Deutsche’s own suit was typical of a predatory and dangerous lender that had helped to bring on the crisis. Trump’s countersuit claimed $3 billion in compensation for the damage it was causing to his reputation. It was pure legal swordplay, but it bought him the time he needed.

In a tight spot Trump is nothing if not pragmatic, and he was certainly not one to be squeamish about the maxims of free-market economics. Faced with the 2008 crisis he knew that American business needed all the help it could get. He had decades of experience working the subsidies available from American government. He liked the cut of Obama’s jib; 2009 was not his moment to get on the anti-Obama bandwagon. As he remarked to a bemused Fox News host, commenting on an early Obama appearance: “I thought he [Obama] did a terrific job. . . . This is a strong guy knows what he wants, and this is what we need. . . . [I]t looks like we have somebody that knows what he is doing finally in office, and he did inherit a tremendous problem. He really stepped into a mess.” On Obama’s stimulus Trump was equally unabashed: “Well, something had to be done. And whether it’s perfect or not, nothing is perfect. And it’s a whole trial-and-error thing. . . . It’s a very, very tough—we are having . . . we’re having the worst year, the worst couple of years, since the Great Depression. And you mentioned the early ’80s. I mean, the early ’80s get blown away by this deal. . . . [W]hen you look at the banks, had trillions of dollars not been poured into the banks, you would have an insolvent banking system, and then you would absolutely have 1929. They did the right thing.” 21 Whereas Trump was reluctantly willing to support the bank bailout, he was positively enthusiastic when it came to helping Detroit: “I think the government should stand behind them 100 percent. You cannot lose the auto companies. They’re great. They make wonderful products.” When conservative interviewers tried to deflect Trump toward the cause of tax cutting, it was an easy sell. Trump doesn’t like paying tax. But he stuck to his guns on stimulus spending. “[B]uilding infrastructure, building great projects, putting people to work” was the right thing to be doing. 22

Six years on from the crisis, Trump’s enthusiasm for an activist, engaged, “strong” presidency remained. What had changed was his attitude to Obama, which had curdled from admiration to vituperative animosity. It was this that formed the bridge to the Right: not programmatic or intellectual affinity but the tabloid absurdity of the National Enquirer and the “birther” conspiracy. Despite having cultivated minority audiences early in his television career, Trump now played the race card. 23 In 2013, after Romney’s defeat radicalized the right wing, Trump positioned himself ever more aggressively as a spokesman of the anti-immigration wing of the Republican Party. By 2014 he had branded the idea of building a “Wall” and had literally trademarked the slogan “Make America Great Again.” Xenophobia, nationalism and an apocalyptic diagnosis of America’s situation formed the bridge. The right wing loved Trump’s slogan, as much for what it acknowledged about the present as for what it promised for the future: America, their America, was in trouble.

If in the Republican primaries it was above all Trump’s unabashed appeal to white male voters that swung the decision, what made this worrying for the party establishment was the way this correlated with his appeal to economic nationalism. Since the 1980s the party leadership had nailed itself to the mast of globalization. The idea of NAFTA was launched by the Reagan administration. It had been crafted by Bush senior only to be carried across the line in 1993 by Clinton. In the 1990s “globalization” was a bipartisan project of the Republicans and the Rubinite wing of the Democratic Party. Their push extended not only to goods and capital. It extended to labor too. The business lobby favored immigration reform, which would give residence rights to the large and cheap workforce of undocumented migrants. Opposition to regulation of all kinds, “freedom” for labor, goods and capital were the ideological bracket that joined American business interests in a single block, from small contractors to the Davos set. There were sectors, perhaps most notably in coal mining, where this alignment did not hold. In polluting industries such as fossil fuels, opposition to globalism, the rejection of the politics of climate change and the blue-collar appeal of American nationalism fit together all too neatly. 24 But those were exceptional cases. On the whole, the Republican Party preserved an uneasy truce between the nationalist base and the globalist leadership. In the 1990s the right-wing nationalist campaigner Pat Buchanan had twice threatened to undo that fragile balance. But it was the progressive breakdown of party coherence after 2008 that really tore it apart. In 2015 Trump exploded onto the scene with the alt-right squarely behind him and transformed the debate. Untouched by concern for economic doctrine, his updated version of 1970s Japan bashing energized the party, promising to keep “illegals” out and to bring blue-collar jobs back to America. Following their new tribal leader, Republicans abandoned free trade en masse. The percentage saying that free trade agreements were bad for America surged from 36 percent in 2014 to 68 percent two years later. By that point only 24 percent of Republicans were still willing to fly the flag for free trade. 25

For the Republican elite, as Trump stormed to the nomination, it was bewildering. “The pillars of the Republican economic agenda have completely collapsed into dust,” a member of the American Enterprise Institute acknowledged. “They’re gone, at least for this election.” 26 The US Chamber of Commerce did not go down without a fight, openly challenging the Republican nominee on the issue of trade. But to no avail. 27 Trump and the protectionist agenda triumphed.

The result by the summer of 2016 was a remarkable inversion. Though behind the scenes oligarchic megadonors were hard at work stoking the flames of right-wing radicalism, America’s name-brand corporations no longer wanted to be associated with the Republicans. When Romney won the party’s nomination in 2012, the money men had flocked to the party. Corporate America lined up to sponsor the Republican convention in Tampa. In 2016 no big names in American finance wanted to be associated with the platform from which Trump would give his apocalyptic acceptance speech. Even if some of the Wall Street top brass felt loyalty to the GOP, they could not stomach Trump and did not want to risk insulting their clients or their workforce. It was a matter of business culture. As one PR adviser commented: “Any corporation will look at this from the perspective of whether or not they would want their CEO sharing a stage at Davos, Aspen or Sun Valley with the Republican nominee. If the answer is no, they won’t be going to Cleveland.” Remarkably, the consultant felt necessary to explain: “The risk of violence in the convention,” between pro- and anti-Trump protesters, “is secondary as security will be strong inside the perimeter.” America’s incipient civil war atmosphere was less of a concern than the question of “whether Mr. Trump and the ideas he . . . represents are homogenous with a company’s brand and business plan.” 28 No one wanted images of “Confederate flags waving over corporate brands.” 29

And the 2008 financial crisis was on the mind not only of Sanders supporters. In the pages of the Washington Post , former Treasury secretary Hank Paulson put the question: “What would have happened if a divisive character such as Trump were president during the 2008 financial crisis? . . . The only reason we avoided another Great Depression was because Republicans and Democrats joined together to vote for the Troubled Asset Relief Program.” 30 In fact, as Paulson knew firsthand, the bipartisanship of 2008 had not come easily. Divisions within the GOP had almost derailed the Bush administration’s efforts to contain the global bank run. It was the Bush White House and the Democrats, not their Republican counterparts in Congress, who carried the unpopular crisis-fighting measures. Now, Paulson warned: “we are witnessing a populist hijacking of one of the United States’ great political parties. The GOP, in putting Trump at the top of the ticket, is endorsing a brand of populism rooted in ignorance, prejudice, fear and isolationism.” 31 This derailment of one of America’s ruling political parties posed a threat that was no less than systemic. For Paulson this left only one choice. He called on his fellow Americans to back Clinton.

In fairness, Trump might have countered by pointing to his track record. In 2008 he had vigorously applauded the bailout. But Trump in 2016 had no desire to remind his supporters of that. “Candidate Trump” was no longer the high-rolling New York wheeler-dealer of 2008. He had morphed into something altogether darker. The man running his presidential campaign was Steve Bannon, the sulfurous impresario of Breitbart and self-proclaimed “Leninist” of the 2013 shutdown. He was only too happy to take up Paulson’s challenge. In Bannon’s dark vision of American history, the moment on the morning of September 18, 2008, when Paulson and Bernanke confronted President Bush with the need for a massive bailout marked a new epoch, what Bannon called the “fourth turning,” the opening of an apocalyptic phase of struggle. 32 On the morning of September 18, 2008, the United States had come close to losing its soul. For Bannon, the mission of the Trump presidency was to seize back control from the globalist elite. As the extraordinary final TV spot of the Trump campaign declared: “It’s a global power structure that is responsible for the economic decisions that have robbed our working class, stripped our country of its wealth and put that money into the pockets of a handful of large corporations and political entities.” 33 The images accompanying the voiceover put faces to that global power structure: George Soros, Fed chair Janet Yellen and Lloyd Blankfein of Goldman Sachs. From the richest businessman ever to run for president, it was a remarkable antibusiness message. It was also the most transparently anti-Semitic campaign spot in recent history. Whether one agreed with Bannon or not, there was no denying that in the decade since the crisis began, American politics had traveled a long way.

Back in 2007, former Fed chair Alan Greenspan had been asked by the Zürich daily Tages-Anzeiger which candidate he was supporting in the upcoming presidential election. His response was striking. How he voted did not matter, Greenspan declared, because “(we) are fortunate that, thanks to globalization, policy decisions in the US have been largely replaced by global market forces. National security aside, it hardly makes any difference who will be the next president. The world is governed by market forces.” 34 This was the mantra of an age of globalization without alternatives. Of course, Greenspan didn’t simply approve of a world governed by market forces, he had done as much as anyone to create it. As Fed chair he had made the markets into the ultimate arbiter of American economic policy. In the early years of the Clinton presidency, he had helped to shepherd the Democrats into a new partnership with Wall Street, thus further limiting the political alternatives on offer. Globalization was not a natural process, opposed to politics. It had been shaped since the 1940s by an alliance of America’s politicians, business elites and policy experts like Greenspan. The election of 2016 revealed how severely the crisis of 2008 had shaken that alliance and the world it had fostered. Most fundamentally, the crisis had exposed the deep unreality of Greenspan’s conception of a world governed by markets. As the crisis revealed, government by market forces was at best a fragile condition. As the global financial system imploded it was the markets themselves that needed governing, by state action on a gigantic scale. And that meant that who governed and where they obtained their political support was not incidental. Elections and party politics did matter. Indeed, faced with the choices in 2016 even Alan Greenspan was no longer indifferent. Unlike Paulson he could not bring himself to endorse Clinton. But he did warn journalists that the “economic and political environment” was the worst he had “ever been remotely related to.” He was deeply concerned that “crazies” risked undermining America. And contrary to his confidence ten years earlier he now admitted that “politically, I haven’t a clue how this comes out.” 35

The Trump campaign may have seemed crazy, but it was not asleep at the wheel. Online media immediately hit back. “Who’s Greenspan calling crazy?” pro-Trump websites demanded to know. And then they turned the tables on the former Fed chair and his successors. Were Trump’s policy positions “[c]razier than negative interest rates? Crazier than paying banks to keep loanable funds in sterile depository accounts at the Fed? Crazier than having the Fed buy up trillions in government debt, remit the interest payments back to treasury, and then count that as revenue to the federal budget?” 36 If all of this now passed for normal monetary policy, was their candidate crazy for denouncing the Fed for fueling a “false economy” and an “artificial stock market”? With the Fed balance sheet expanded to $4.4 trillion in pursuit of a full employment target mandated by legislation passed in the days of Jimmy Carter, could one seriously deny that the economy was politicized? 37 Were the Trump and Sanders campaigns crazy or simply stating what should have been obvious: the fiasco of the project of Greenspan’s generation. Financial globalization that Greenspan and his ilk had worked so hard to institutionalize as a quasi-natural process had been exposed as just that, an institution, an artifact of deliberate political and legal construction with stark consequences for the distribution of wealth and power.

II

Disturbing as they were to the status quo, in the summer of 2016 the most common response to the Trump and Sanders campaigns was to dismiss them as a passing spook. Once Clinton had knocked Sanders out, she would beat Trump by a landslide. While the alt-right continued to fly the flag, Republican donors shifted their money from the presidential campaign toward House and Senate races with a view to ensuring that as president, Hillary Clinton would face a solidly hostile Congress. Only the inner core of Trump’s campaign and the audience of Fox News, swaddled in what the mainstream denounced as “alternative reality,” continued to believe in victory. On election night, even as the results swung Trump’s way the mainstream media could barely hide their disbelief and dismay. 38 Within hours the recrimination and finger pointing began. It was the white working class and the racists who had rallied to Trump. Women and minorities had failed to turn out for Clinton. Or, it was down to Russian meddling. There was a global alignment of forces against liberalism. President Obama himself weighed in to declare that Trump, like Brexit, was an expression of protest against globalization. 39

In fact, a deep dive into the poll data showed that Trump’s voters were better off than the average American. 40 The voters with the lowest incomes—overwhelmingly minorities—continued to vote Democratic. But a detailed accounting of the electoral statistics did show a significant shift to the Republicans among white male voters with less than a college education. It was less immediate misery than anxiety about the future that drove the Trump vote, fears that in the white population were associated with hostility to Latinos and black Americans, and among men with hostility to upwardly mobile women. 41 Trump improved on Romney’s miserable tally in the Rust Belt states. Dog-whistle racism and nationalism solidified this constituency. Even an issue such as trade was saturated with racial markers. 42 In one advertising spot after another, the face of the American worker displaced by foreign imports was that of a burly white man in a hard hat. And campaigning mattered. Concentrating their effort where it counted, the Republicans put in relentless legwork and media time in key midwestern states that the Democrats considered theirs by right. The complacency, the refusal to countenance the reality of Trump’s appeal went deep. The Democrats offered nothing to counter Trump’s manufacturing “cargo cult.” 43 In answer to Trump’s crude appeals to white male nationalism, Clinton offered anodyne conformity to the polite conventions of corporate globalism. That did not play with the 7 million Americans who had voted for Obama and now shifted to Trump. They were looking for a candidate who did not appear to represent the establishment. Though they constituted only 4 percent of the electorate their votes were enough to hand Michigan, Pennsylvania and Wisconsin to the Republicans, rendering Clinton’s huge tallies in New York and California irrelevant. What the Democratic operatives failed to understand was that the race was theirs to win, not to lose. 44 Clinton was running to succeed a two-term Democratic presidency. A change was in order. The economy might not be the disaster that Trump suggested, but it was not booming. To overcome these handicaps, Clinton needed to energize the Democratic base. That she utterly failed to do.

In the aftermath, the shock of Trump’s election produced a state of confusion and stunned puzzlement reminiscent of Brexit. If Donald Trump had been elected president, who actually ruled America? Surely some branch of the establishment would intervene to constrain or redirect this aberrant popular choice. 45 The idea of the “deep state” no longer belonged to the realms of marginalized conspiracy theory or radical critique; it was mainstream media discourse and it influenced the Trump team themselves, who circulated memoranda on which bits of the deep state they would have to do battle with first. 46 With the FBI and the CIA sifting through the evidence of Russian interference and with Trump seemingly bent on picking a fight, it was from the security apparatus and law enforcement that the pushback was expected. But in truth the entire establishment of the United States had lined up against the president-elect. In August 2016 the Wall Street Journal contacted every single surviving member of the president’s Council of Economic Advisers back to the days of Richard Nixon—all forty-five of them. Though twenty-three were Republican appointees, none would endorse Trump. 47

Trump did not back down. If there was one thing he had been elected to do, it was to stir things up. This meant conflict, the more and the noisier the better. He was set on his agenda of economic nationalism. It wasn’t even a choice. He simply did not know any different. In December 2016 he intervened at Carrier, an Indianapolis manufacturer of furnaces and air conditioners, to persuade them to keep one thousand jobs in the United States. The state of Indiana, where Trump’s vice president, Mike Pence, was governor, stumped up millions in tax rebates. Company spokesmen helpfully announced that they had confidence in Trump’s promise to reform the corporate tax code and to improve business conditions in the United States. Then the president-elect jetted in to Indianapolis to hail his first economic policy achievement and to reveal another reason why United Technologies, Carrier’s parent, might have wished to cooperate. “Companies are not going to leave the United States any more without consequences,” Trump declared menacingly. “Not going to happen. . . . [L]eaving the country is going to be very, very difficult.” 48 Or as he tweeted later that weekend: “Any business that leaves our country for another country, fires its employees, builds a new factory or plant in the other country, and then thinks it will sell its product back into the U.S. without retribution or consequence, is WRONG!”

For conventional commentators it was jaw-dropping. Did the president-elect not understand that the success of American business depended precisely on their ability to deploy labor and capital globally? As several commentators remarked, his threatening tone was “more like the populism of Hugo Chavez than even something Bernie Sanders would say. It’s the kind of threat that would find its ultimate expression in currency controls—that favored instrument of economic dictators around the world.” 49 Had a left-winger engaged in such provocation, barring intervention by the Treasury and the Fed, the markets would surely have plummeted. But nothing of the sort happened in the wake of Trump’s election. Trump was a challenger, but not all challengers are alike. Among Democratic voters deep political grief went together with economic gloom. But what was no less remarkable was the reaction on the other side. Republican supporters of all kinds—from regular voters to small businesses and traders in the financial markets—exploded with new optimism. 50 It was somewhat embarrassing to bigwigs on Wall Street who thought the new president was incompatible with their “brand values,” but bank shares were among those making the biggest gains. Trump liked to bang on about abolishing Dodd-Frank. If that happened it would be good for the banks, at least in the short run. Health-care stocks surged as markets anticipated a rollback of Obamacare and its cost cutting. There was also a bump in infrastructure stocks. Meanwhile, bonds sold off as the prospect of Trumpflation made it all the more likely that the Fed would raise rates. 51

And this “Trump bump” was only confirmed when the president set about recruiting a team. He kept loyalists and ideologues around him. He made no concessions on substance of policy, but he widened his coalition by stocking his cabinet with wealthy corporate managers and generals. The most astonishing thing, given the menacing rhetoric of his final attack ad, was the return of Wall Street. Trump supposedly canvassed Jamie Dimon of J.P. Morgan for Treasury secretary before plumping for the obvious alternative, Goldman Sachs. Both the number one and number two positions at the Treasury were to be filled by men—Steve Mnuchin and Jim Donovan—with Goldman Sachs pedigree. Dina Powell, who moved to the influential assistant position at the White House, had formerly headed the bank’s philanthropic efforts. National Economic Council director Gary Cohn was formerly Goldman’s president. Meanwhile, to head the Securities and Exchange Commission, Trump’s team proposed a partner from Goldman’s main law firm, Sullivan & Cromwell. There was some anxiety from the White House chief of staff about the optics, but that was assuaged when Donovan withdrew. 52

To a conventional programmatic political mind this was a flagrant contradiction and suggested that the establishment was reasserting control. But it was not clear whether Trump understood programmatic policy debate in the conventional sense. What Trump did understand, or at least what he inhabited, was a rawer world of power, a world dominated by a single logic: bully or be bullied. As one commentator put it, Trump viewed the world as a “kind of Manhattan real estate market writ large, a vicious snake pit where the strong and hungry eat the weak and soft.” 53 From this point of view, the fact that Trump had criticized the leaders of Wall Street then hired them as his subordinates was not a sign of contradiction or self-subversion. It was a sign of his triumph. Trump’s populism revolved not so much around policy as around the pure realization of power. He, Trump, was not only a successful businessman, he was also famous and had great TV ratings. He could challenge the establishment in his electoral campaign, pillory the chair of the Fed and demonize the CEO of Goldman Sachs and win. Having won, he could then audition Jamie Dimon of J.P. Morgan for Treasury secretary and reject him in favor of a minor Goldman Sachs alumnus who was more to his liking. If you could do all these things, you clearly were king of the hill, all the better for being king by popular acclamation. That is all Trump needed and it was a story to which he returned obsessively.

The revolving door that feeds government in America regularly rotates between public service and the corporate world. In firms like Goldman Sachs, the rotation is de rigueur for senior figures. It is not easy for a patriotic American to turn down an invitation from the White House to serve. But why, one has to ask, would a senior business figure be willing to be associated with such an administration? To which the simple answer is that Trump’s victory changed everything. His objectionable personality and outlandish policy proposals now had to be weighed against the more basic political question of who would do what for whom.

III

When it came to governing, it was not easy to fashion a coherent program out of such a mixed coalition. But there was one thing on which the Trump administration and the Republicans in Congress could agree: overturning the Obama legacy. In this sense, after a campaign shaped by the aftereffects of 2008, the first phase of the Trump administration was also molded by the legacy of 2008, but in negative. The first twelve months of the Trump presidency offered an audit on the robustness of the state-building project pursued by the Democrats since the crisis. How much of it would stand up in the face of the onslaught of a Republican president and a Republican Congress? In 2008, pondering the fiscal track record of the George W. Bush administration, Brad DeLong had wondered what was the right strategic and tactical course for the Democrats, “when there is no guarantee that any Republican successors will ever be ‘normal’ again.” 54 Nine years on the question was more pressing than ever. Since 2009 the congressional Republicans had been waging relentless political war, first against the stimulus, then the Affordable Care Act, also known as Obamacare. Twice in 2011 and 2013 they had taken the debt ceiling hostage. Now, with control of both the presidency and Congress, what would they do?

Obamacare was the scalp they wanted most and it ought to have been easy. As it had emerged from its congressional ordeal in March 2010, the Affordable Care Act was mangled and flawed. But for all their grim determination, in the critical first six months of the Trump presidency the Republicans could neither replace nor repeal it. What stood in their way was the inherent complexity of the subject matter and deep divisions within their party. But their failure also reflected the fact that the ACA, like any truly major piece of social or economic legislation, had created its own social constituency. Even an institution as deeply disappointing as the ACA was hard to budge once tens of millions of people came to depend on it and hundreds of billions of dollars began to flow through its channels. Indeed, among the states that benefited most from the extension of health coverage under Obamacare were Kentucky and West Virginia, diehard Trump country. 55 As Trump took office, support for the ACA among the most important group of voters, Independents, had risen from 36 percent in 2010 to 53 percent. 56 By the summer, when the desperate Republican congressional leadership made a last bid simply to repeal Obamacare without replacement, they had the support of only 13 percent of Americans. 57 Not surprisingly, sufficient Republican moderates refused to go along.

If they couldn’t repeal and replace Obamacare, what could they do? By the summer of 2017 it seemed that the incoherence of the Republicans, when faced with the complex reality of modern government, might prevent them from taking any effective action. 58 The ACA fight had left little room on the legislative agenda. Trump’s promised infrastructure program was a will-o’-the-wisp. Tax reform was much discussed with no apparent action. Meanwhile, basic financial questions could not be dodged. The debt ceiling remained in place, and when the Treasury hit its borrowing limit in the spring of 2017, it was forced to resort to the familiar makeshifts. 59 Treasury Secretary Mnuchin vainly called on Congress to raise the ceiling. But in the summer the House went into recess without a vote. In the meantime, the new director of the Office of Management and Budget was Mick Mulvaney, a founding member of the Freedom Caucus, which had diced with default in 2011 and 2013. 60 He did not want to make concessions to the centrists or the Democrats. The extreme spending cuts demanded by his old friends in the Freedom Caucus had no majority. For Trump’s budget director a shutdown was not the worst option. If the United States was to crash into the debt ceiling and be forced to prioritize claims, a default in all but name, so be it. 61 Astonishingly, the president seemed to agree. In May 2017 Trump tweeted blithely about a “good shutdown.” 62

As the summer came to an end, despite their control of both the White House and Congress, it seemed as though the Republicans would fail to resolve the budget issue. The real question was whether the Democrats would allow them to drive the United States off the fiscal cliff. When Obama was in the White House, the Democrats had pilloried the Republicans for failing to carry their share of the burden of government. Could they refuse to back the president, even if the president was Trump? Before this dilemma could really bite, natural disaster intervened. With Hurricane Harvey having devastated a large part of Texas and another hurricane roaring into Florida, neither Trump nor the Democrats wanted to look inactive. 63 At a meeting in the Oval Office on September 6 the president did an about-face. He not only abandoned the Republican congressional leadership but also cut off his own Treasury secretary in midsentence to strike a deal with the Democrats. It was a dizzying inversion that sent pundits scrambling for historical examples of “independent” presidents who had risen above the American party system. 64 The realities were more hard edged than that. With Chuck Schumer and Nancy Pelosi having saved the administration from a shutdown, Trump was only too happy to cheer on the Republicans as they returned to the attack. 65 Scrapping Obamacare might not sell as a political proposition, but cutting taxes surely would. The Republicans in the House and Senate began urgent work on “tax reform.”

The resulting tax bill that passed both houses of Congress in December 2017 was hugely controversial. The sugar coating, such as it was, consisted of across-the-board reductions in personal income taxation and cuts to exemptions that principally hit high-income local taxpayers in states that voted Democratic. But these were time limited. Within a few years many lower-income Americans would be paying higher taxes. Of more lasting benefit to the very wealthy was raising the estate tax threshold to $11 million. And what really mattered was a 40 percent cut in the rate of business taxation, which meant that profits could either be retained for growth or paid out to shareholders. Given the vast inequality in wealth holding and particularly in the holding of equity—the top quintile of the American income distribution owns 90 percent of corporate equity—the benefits go to the better off. Then for good measure, the Senate added the removal of the single-payer mandate that required all Americans to take out health insurance. Without this mandate, by most estimates, 13 million Americans would drop out of coverage. As many low-risk individuals left the insurance plans, the premiums for those who did remain would surge. DeLong’s fears were amply confirmed. In its redistributive impact and the scale of the giveaway, 2017 stood in comparison with the huge Reagan tax cut of 1981 and those of Bush in 2001 and 2003. 66

To ease the passage of their tax measures through Congress and to calm the nerves of fiscally conservative Republicans, the Treasury and fellow traveling Republican economists talked down the deficit implications. 67 They resorted to the old Reagan-era arguments that lower tax rates would boost growth and thus raise government revenues. Even the notorious Laffer curve, purporting to show a positive relationship between lower tax rates and government revenue, made a comeback. 68 But the vast majority of economists were scornful of these evasions. The tax cuts would clearly add to the deficit. Simpson and Bowles, who had headed Obama’s national commission on fiscal responsibility and reform, denounced the tax plan as a return to the era of “deficit denial.” 69 In fact, it was not so much denial as hard-nosed political calculation. There was no way to cut the corporate tax rate to as little as 21 percent without incurring deficits. 70 Nor did this scare the activist Republicans. As they saw it, the larger the deficits, the more urgent the need to move on to stage two of their program. 71 With the tax cuts threatening to add a trillion and a half dollars to the national debt, spending cuts would be mandatory. Medicaid would be pared back as far as the law permitted and the rest of the federal government would be cut to the bone. These were the Republican tactics not of the 1980s but the 1990s. The congressional Republicans were starving the beast.

Liberals were understandably indignant about the gross inequity of the tax proposal. The UN’s special rapporteur on extreme poverty, who happened to be touring the United States visiting some of the 40 million Americans who lived in conditions of deep deprivation, denounced the tax plan as “a bid to make the US the world champion of extreme inequality.” 72 But even setting equity concerns aside, starving the beast was a failed fiscal strategy. Historically, the spending cuts that were supposed to follow on the tax cuts did not arrive. It was easier to rail against tax breaks than it was to get them repealed. Key areas of welfare spending had supporters even in the Republican ranks. At the same time the Republican plans to expand the army by 10 percent and raise the navy to 355 fighting ships would increase military spending, the largest element of discretionary spending, by $683 billion, or 12 percent, over the decade to 2027. 73 Rather than shrinking big government, the main effect of Republican fiscal tactics was likely to be a further reduction in America’s already deeply inadequate tax base. Following the tax cuts, the federal government’s take of GDP would fall to 17 percent, a figure befitting an emerging market state rather than the government of an advanced economy. 74

In 2009, when a Democrat was in the White House appealing for Congress to provide a stimulus to the American economy as it plunged into the worst crisis since the 1930s, the Republicans had voted, to a man and a woman, against a stimulus. They denounced Obama’s Recovery and Reinvestment Act as a ruinous demonstration of fiscal irresponsibility. Now, with unemployment at lows not seen since the boom time of 2007 but with Trump in the White House, they were working hard to deliver a ten-year $1.4 trillion stimulus. In their defense it might be said that given the sluggishness of the recovery and the large number of people who had retreated from the workforce during the crisis, there was a case to be made for running the economy hot. 75 But even those who advocated such an adventurous policy found it hard to justify the Republican tax plan. 76 America’s wealthiest did not need further benefits. Investment was certainly depressed, but it was not for lack of funds. America’s corporations had trillions of dollars in cash on hand. What was clearly long overdue was a public investment program, to make good the embarrassing deficits in America’s infrastructure. But there was little enthusiasm for that from Congress. The Republicans needed to end Trump’s first year in office on a high. They needed to deliver for their donors. 77 The 2017 “tax reform” did both.

When budget hawks inside the Clinton and Obama administrations had worried about deficits, what was on their minds was market confidence. How would the markets react to the latest round of spendthrift Republican policy? Increasing the debt by perhaps as much as $1.5 trillion over ten years ought surely to produce a reaction. Following the surprising election outcome, bond markets had been twitchy. 78 Anticipating that the Trump administration would launch a major infrastructure drive and add further stimulus with tax reform, the markets expected the Fed to bring interest rate increases forward. Over the winter of 2016–2017 this prompted bonds to sell off and yields to rise. With the ECB and the Bank of Japan both engaged in QE, the dollar appreciated sharply, sending a ripple of uncertainty around the world of dollar borrowers. Their debt-servicing costs were going up. But then, as the reality of the shambolic Trump administration and the continuing self-paralysis of the Republicans in Congress became clear, the fever broke. Driven by tech euphoria, the stock market continued to boom. The Fed insisted that it would continue its stepwise increase in interest rates. But there were few signs of panic in the bond market. 79 The tax cuts with which the Republicans ended the year produced a shrug from the bond markets. As one analyst commented: “Whatever grade you assign to the end result, the bond market and economists are adding an extra ‘minus’ to the grade. So, if you think it’s a ‘B’ effort, the market’s grade is a ‘B minus.’” 80 The markets weren’t cheering but neither did the Trump administration have vigilantes on its tail.

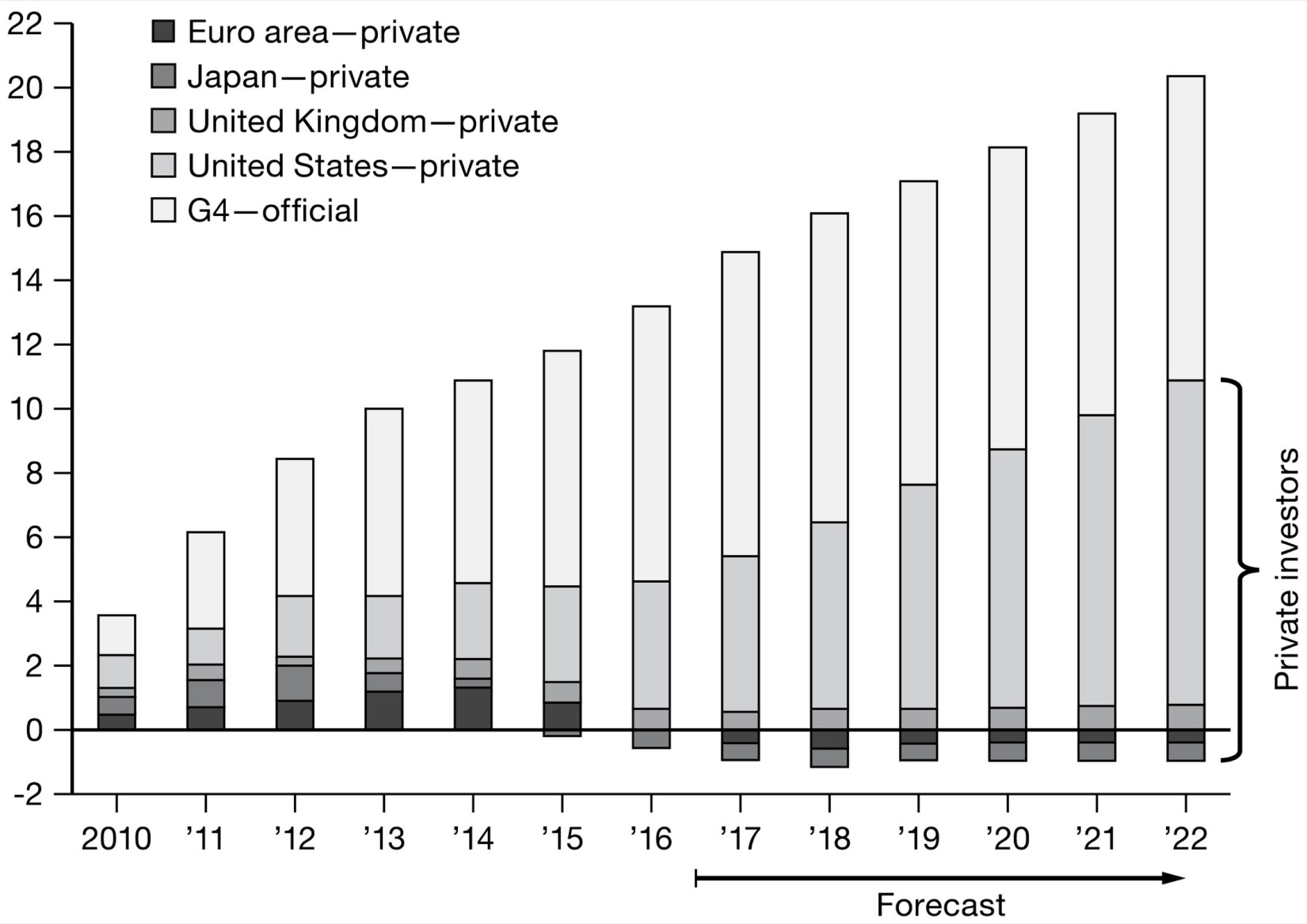

The congressional infighting over Obamacare and the Republican tax cuts was bare-knuckle American politics. But a clue to the relative calm in the Treasury market could be found in the same set of influences that had also preserved calm in the face of the Bush-era deficits of the early 2000s—the global demand and supply of safe assets. In the fall of 2017 the IMF published a remarkable table that showed the issuance of debt since 2010. 81 As this data revealed, austerity and QE had led to a major reshuffling of security portfolios. Given the budget-control measures adopted in Europe, the active bond buying by the ECB and the even greater activism of the Bank of Japan, they were, for the foreseeable future, not significant suppliers of safe assets to global investors. Not only was the ECB hoovering up eurozone bonds, but Germany, the chief supplier of European safe assets, was running a budget surplus. On a global scale over the next five years, the United States would be the only source of safe, Treasury-grade assets for investors worldwide. Whatever you might think of the Trump administration, if you needed to park a large volume of funds in safe government debt, there was no alternative to US Treasurys.

The Global Supply of Safe Assets Change in Stock of Advanced Economy Sovereign Debt by Region of Issuance and Holder (in $ trillions cumulative change since 2010)

Source: IMF, Global Financial Stability Report, Ocober 2017, 19, figure 1.13, panel 4.

IV

The Republican campaigns to roll back Obamacare and cut taxes were of long standing. Trump’s targeting of Wall Street in his election campaign was more novel. But it made electoral sense. Almost a decade on from the financial crisis, the banks were still deeply unpopular. A poll in the summer of 2017 revealed that 60 percent of Americans still regarded Wall Street as a “danger to our economy,” and only 27 percent thought regulation had gone far enough or posed “a threat to innovation or economic growth.” Fully 47 percent of Trump’s voters wanted to “keep or expand” Dodd-Frank, as opposed to only 27 percent favoring repeal or scaling back. When it came to financial products and services, 87 percent of Republicans and 90 percent of Independents favored regulation. 82 Wall Street lobbyists might wail against Dodd-Frank, but as the Obama administration insiders knew, it was they who had held back the popular tide running against the banks. And Trump, it turned out, was no different.

His campaign attacks were politics pure and simple. The leaders of Wall Street had never liked Trump. They clearly preferred the Clinton brand. He had paid them back in kind and he had won. The question of who was boss had been answered. Trump’s about-face once in office was utterly unabashed. He would do as befitted a boss-president. There would be a bonfire of regulations and in particular those of his predecessor. The thought of doing a “big number” on Dodd-Frank pleased POTUS. And it pleased him also to bestow favors on and receive applause from powerful interests, even those he had previously made a show of attacking. As he told a meeting of CEOs in April 2017: “For the bankers in the room, they’ll be very happy.” 83 To have favors lavished on them by the man who had pilloried them on the stump might seem topsy-turvy. But the bankers were not complaining. As the Financial Times commented: “Imagine going to the races, betting 98 per cent of your stake on the favourite [Clinton], which loses in the final stretch, and going home with huge winnings.” 84 As far as Wall Street was concerned it turned out that the game of politics was heads I win, tails you lose. Neither the politicians nor Wall Street gave a second thought to the angry voters who had actually put Trump in the White House.

To help with the gutting of Dodd-Frank it was only too easy to find bank lobbyists and business-friendly economists. And enthusiasm also came from the Republicans in the House. Led by Jeb Hensarling, who back in 2008 had spearheaded opposition to the bailouts and was now chairman of the Financial Services Committee, the House rapidly passed the so-called Financial CHOICE Act—where CHOICE stands for Creating Hope and Opportunity for Investors, Consumers and Entrepreneurs. It not only defanged Dodd-Frank. It was libertarian purism. It would scrap the Volcker rule and make stress tests a biannual rather than an annual affair. It eliminated the Orderly Liquidation Authority, insisting that failing banks should simply be referred to the bankruptcy courts. 85 Astonishingly, in the name of the freedom to choose, the CHOICE act even promised to gut Elizabeth Warren’s Consumer Financial Protection Bureau. 86

For an administration habitually decried as populist, the remarkable thing was how spectacularly unpopular such legislation would have been. Like ACA repeal, the CHOICE Act had little or no chance of passing the blocking position the Democrats held in the Senate. As in the battle against Obamacare, the struggle was best waged outside the spotlight. Even if Dodd-Frank remained in place, the regulatory regime was fair game. This was a legacy of the discretionary conception of financial governance that framed Dodd-Frank. Pursuing maximum freedom from congressional interference, Geithner’s Treasury had pushed for the agencies to have the widest possible latitude in their regulatory efforts. Now that discretion could be used to fundamentally change the regime of bank supervision without the need for legislation. Mnuchin’s Treasury began preparing a series of reports on its approach to financial regulation, opening the door to the bank lobby. 87 By one count fully 75 percent of the bankers’ recommendations were incorporated into the Treasury’s new regulatory blueprint. 88 , 89 Unpicking the Volcker rule, which had taken almost four years to assemble, began by asking the banks how they would like it changed. 90 In November 2017 rather than scrapping the Orderly Liquidation Authority and restoring the role of the bankruptcy courts as the CHOICE Act had proposed, the Treasury decided that it preferred to retain control over the liquidation of a megabank in crisis. 91 Even if there were to be no more bailouts, the prospect of another Lehman was not attractive. The Trump administration exposed the basic weakness of Geithner’s regulatory design. It depended on those operating the law to have a programmatic commitment to systemic stability. Without that, the legislation per se was largely empty.

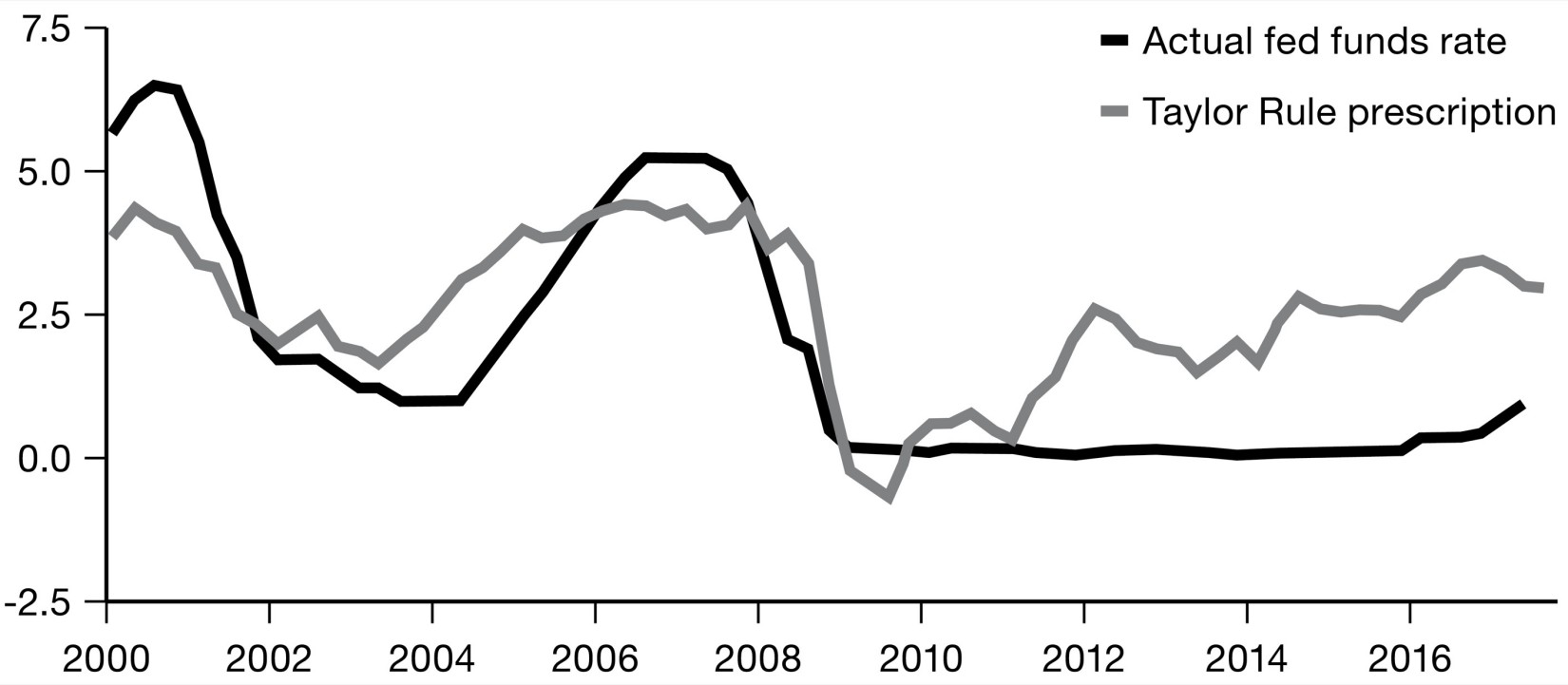

Arguably the most radical section of the CHOICE Act was the provisions pertaining to the Fed. They constituted an all-out assault on central bank activism as practiced by Ben Bernanke. In the future the CHOICE Act demanded near total transparency of all Fed meetings. The act called for the FOMC to declare a mathematical policy rule to justify its interest rate choices. As its default the act specified the so-called Taylor rule, named after John B. Taylor of Stanford University, a favorite of the Right and a longtime academic rival of Ben Bernanke. His rule called for interest rates to be set as the sum of:

The rate of inflation over the previous 4 quarters;

One-half of the difference between the real GDP and an estimate of potential GDP;

One-half of the difference between the rate of inflation over the previous 4 quarters and 2 percent;

and an assumed real interest rate of 2 percent.

It was a mechanical formula that required interest rates to be adjusted upward if inflation was high and unemployment low, or downward if the reverse was the case. If the Fed preferred a different rule, the CHOICE Act stipulated that it must spell out its own formula in similarly mechanical terms and demonstrate econometrically that its rule was preferable to the Taylor model.

As the authors of the bill were well aware, enshrining this formula in law implied an entire alternate history of American monetary policy back to the crisis and before. Taylor and his disciples blamed the crash on the fact that in the early 2000s, under Greenspan, rates had been too low. 92 During the crisis, on the other hand, if one applied the Taylor formula, interest rates should have been pushed into negative territory. A strict application of the Taylor rule in the autumn of 2008 would have called for rates of below zero, effectively a tax on savings deposits. It was because he judged that impracticable that Bernanke had adopted quantitative easing. The CHOICE Act would ban any such improvisation. Once the acute crisis had passed, instead of QE2 and QE3, Taylor’s formula would have called for rate increases. There would have been no worrying about taper tantrums, whether at home or abroad. Indeed, no regard would be paid to conditions anywhere in the world other than the United States, unless, of course, the Fed dared to include its wider global concerns as a variable in its own interest rate equation.

Actual Fed Funds Rate and Taylor Rule Prescription

Source: Atlanta Fed.

The CHOICE Act was first and foremost a political gesture. Promising to curb the discretion of the Fed played well on the Republican side. But on the substance of policy there was, in fact, no disagreement. Taylor rule or not, 2017 was clearly a time to tighten, to raise rates and to start, tentatively, unwinding the gigantic balance sheet built up during the era of QE. 93 After ending security purchases under QE3 in October 2014, the Fed had made the first move to raise rates in December 2015. It had then paused before inching them up again in December 2016, March 2017 and June 2017. The FOMC ended 2017 by laying a path of at least three further increases in 2018.

As always, a subtle game was played out between the FOMC and the markets. Janet Yellen proved herself a master of this game, managing to socialize the idea of rate increase without triggering panic. But there was never much chance of her tenure being extended into the Trump presidency. 94 There was talk that John B. Taylor himself might be in line to take Yellen’s place. Trump liked the look of Kevin Warsh, an underqualified New York princeling who had been parachuted onto the Fed board by the Bush White House in 2006. But in the end he settled on Jerome Powell. It was a strikingly conventional choice. Powell was a Republican investment banker in the Mitt Romney–Hank Paulson vein. He had earned the trust of the Obama administration by campaigning within the Republican Party against the shutdown of 2011. 95 That had led to his nomination to the Fed board in December 2011, where he had distinguished himself by his loyalty to both Bernanke and Yellen. He was also thought to be supportive of the Dodd-Frank framework. 96 But what recommended Powell to Trump were most likely his personal attributes. He was not an academic economist. He was a rich businessman. With a personal net worth estimated in excess of $100 million Powell was by far the wealthiest person to take the position of Fed chair since the 1930s. Unlike Professor Taylor, Powell was nondoctrinaire when it came to policy. Under his stewardship the White House would not have to fear unduly painful increases in interest rates.

V

Building a new administration and setting a domestic policy agenda was a protracted and complex business, for which Trump and his coterie were ill prepared. All the more forceful was their approach to foreign relations, where the White House and the executive branch had far more leeway. Within forty-eight hours of his inauguration on Friday, January 20, 2017, Trump announced his intention to renegotiate NAFTA. The next day, Monday, January 23, he withdrew the United States from the Trans-Pacific Partnership. TTIP, the object of years of laborious negotiation with the EU, was also left for dead.

It was a spectacular overturning of a centerpiece of Obama-era foreign economic policy. TPP was a showpiece of American grand strategy in a multipolar age. It was a shock to America’s allies. Committing to TPP had cost many Asian countries, most notably Japan, serious political capital. And it begged the question: If there was no grand regional alliance, where did that leave Obama and Clinton’s pivot to Asia and the de facto policy of containing China? Indeed, abandoning TPP and TTIP was not just a break with the Obama era, it was a reversal of America’s sponsorship of multilateral trade policy dating back to the 1940s. 97 At the first G20 meeting attended by Treasury Secretary Mnuchin in Baden-Baden in March 2008, it was impossible to reach agreement even on a simple pledge “to resist all forms of protectionism.” 98 As Wolfgang Schäuble noted in his usual uncompromising fashion, the meeting had reached an “impasse.” 99 All Mnuchin had to offer by way of clarification was that the new administration had a “different view on trade.” Philip Hammond, the UK chancellor, advised his colleagues that it was better to give the Trump administration more time: “If we demand a hard answer now, I’m pretty sure we won’t like the answer we get.” 100

Meanwhile, in Washington a battle was raging over NAFTA. As far as Trump was concerned it was “one of the worst deals ever.” 101 As he told journalists after three months in office, he “was really ready and psyched to terminate” it. 102 The relish was obvious. Bannon and economic adviser Peter Navarro, a nationalist trade economist, urged him to follow his instincts. For the announcement they had earmarked a rally in Harrisburg, Pennsylvania, on April 29, 2017, to celebrate his first hundred days in office. For Mexico and Canada it would have been a brutal blow. Realizing the seriousness of the situation, they rapidly coordinated their positions. Desperate to prevent a precipitate break, hundreds of American business leaders lobbied the White House. The secretary for agriculture, the commerce secretary and the secretary of state all pleaded for a stay of execution. In the end the decisive argument appears to have been a map showing quite how much of “Trump country” would be hurt by withdrawal. Did the president really want to put Texas in play? The map “shows that I do have a very big farmer base, which is good,” Trump later told journalists. “They like Trump, but I like them, and I’m going to help them.” 103 That meant not canceling NAFTA. Instead, Washington would renegotiate. But it would do so from a weakened position. The Obama administration had spent years haggling for improved access to Canadian agricultural markets, cross-border licensing of financial services and improved labor standards with Mexico. To do so it had used not raw threats but the lure of the even bigger trade deal, TPP, a project into which the United States had inveigled Mexico and Canada at the Los Cabos G20 summit in 2012. With TPP gone, all the concessions on NAFTA already agreed were consigned to the dustbin of history. 104 Trump’s renegotiation would start from scratch with little but threats to offer.

NAFTA, TPP, TTIP were regional treaties. The truly global forum for trade policy was the WTO. It was an original creation of the founding moment of American globalism in the 1940s. 105 The United States had long been its most powerful backer. President Trump did not attend the party to celebrate the seventieth anniversary of its founding in November 2017 at the Ronald Reagan building in Washington, DC, but he sent his ill wishes by way of Fox News. “The WTO was set up for the benefit [of] everybody but us. . . . They have taken advantage of this country like you wouldn’t believe,” he told the news channel. 106 As his trade representative, Trump appointed the veteran trade warrior Robert Lighthizer, who in the 1980s had been responsible for extracting the agreements by America’s major competitors to voluntarily restrain their steel exports to the United States. Lighthizer blasted the WTO with a broadside. He objected to the judicial activism of the WTO’s trade arbitration panel, its pandering to the special pleading of large developing countries like India, its failure to address areas of chronic industrial overcapacity such as steel and above all its inability to get to grips with the unprecedented challenge to economic liberalism posed by the rise of Chinese state capitalism. 107 In Washington’s view, the WTO should confine itself to providing a forum for bargaining between the major trading powers. The United States should throw off any restraint on its ability to retaliate against economies that it considered to be discriminating against it. But rather than translating this vision into positive proposals for the WTO, the Trump administration adopted the tactics the Republicans had used to such effect in Congress. The United States refused to permit the appointment of new arbitrators to WTO panels, threatening to hollow out the institution, making it increasingly dysfunctional and illegitimate. If there was no actual éclat at the WTO meeting in December 2017, the lack of progress on any area of trade liberalization was dismal. 108 Lighthizer did not even deign to stay until the end of the conference.

The shock delivered by the new administration to global economic institutions was severe. There had been nothing like this since the 1930s and nowhere was this felt more acutely than in Europe. In the early days it was unclear whether the Trump team actually acknowledged the EU as a counterparty or understood that the United States no longer maintained bilateral trade relations with individual European countries. In an interview given just days before he took office, Trump dismissed the EU as a “vehicle for Germany.” According to inside sources, members of his entourage were placing phone calls to European leaders to ascertain which countries might be “leaving next.” 109 Trump’s people believed the Brexit hype. There was a fear in Europe that Trumpery would spread. London was about to trigger Article 50 and formal exit proceedings. The Austrian, Dutch and French elections were all in play. There were forces in the White House that openly supported not only Brexit but Marine Le Pen and the Front. 110

Once the initial shock wore off, international forces began to concert themselves. Mexico and Canada worked together closely to do what was possible to save NAFTA. The other parties to TPP decided to go ahead without the United States. By late May, when Trump made his first visit to Europe, the “populist” spook had passed. Macron was in the saddle in Paris. When the American president refused publicly to underline America’s commitment to Article 5 of the NATO treaty and gave notice of his intention to withdraw from the Paris climate change agreement, Merkel had seen enough. Germany was in general election mode and the spectacular swing in European public opinion against Trump gave Merkel every reason to act. On May 28, 2017, the day after Trump’s departure, speaking to an enthusiastic crowd in Munich, the German chancellor announced that Europe had to adjust to a new reality. 111 After Trump and Brexit, it was clear that Europe could no longer rely completely on its long-standing American and British allies. “The times in which we can fully count on others are somewhat over, as I have experienced in the past few days. We Europeans must really take our destiny in our own hands. Of course we need to have friendly relations with the US and with the UK and with other neighbours, including Russia. But we have to fight for our own future ourselves.” 112

It was no doubt a remarkable moment. As Richard Haass, president of the Council on Foreign Relations, tweeted: “Merkel saying Europe cannot rely on others & needs to take matters into its own hands is a watershed—& what US has sought to avoid since WW2.” 113 But what did it actually amount to? Europe’s own process of consolidation in the wake of the crisis seemed stalled. President Macron of France offered a bold vision of Europe’s future in a major speech at the Sorbonne. 114 But who was it addressed to? After the inconclusive elections in Germany in September 2017, there was only a caretaker government in Berlin. Italy was creaking under the weight of years of recession. Spain was thrown into chaos by Catalonia’s bid for independence. Furthermore, any moves toward further integration and self-determination for the Continent were bound to arouse resistance. If Britain was leaving, the difficult Eastern Europeans remained. In July 2017, on his second trip to Europe for the G20 meeting in Hamburg, Trump made a point of stopping in Poland. In front of a crowd of supporters of the Law and Justice government, Trump found a European audience that loved him. The flags waved as he proclaimed America’s commitment to NATO as a bulwark of civilization and a bastion for the people of the West who “still cry out ‘We want God.’” 115 Trump had segued from “America first” to a “clash of civilizations,” but neither one nor the other would go down well with the multicultural crowd that was awaiting America at the G20 meeting. As Hammond, the British chancellor, had pointed out, sometimes it was better not to push the Trump administration too hard for a clarification of its position. There was reason to fear that one might not like the answer.

Clearly, Merkel’s vision of a united Europe fighting for its own future would have to tackle deep internal divisions. Nor was the rise of right-wing nationalism Europe’s only point of difference. Trump’s protectionism was directed not just against Asian competitors. Germany too was in the crosshairs. As ever, Finance Minister Schäuble was quick to respond. He would no more take criticism from Trump and Mnuchin than he had from Obama, Geithner, the IMF or fellow Europeans. 116 In the German view a trade surplus was first and foremost a reward for export competitiveness. But the kind of gigantic deficit run by the United States also pointed to deeper macroeconomic imbalances. It was hardly surprising that given Germany’s budget surplus and America’s large and growing government deficit there should be a difference in their trade accounts. This was the familiar repertoire of arguments about transatlantic trade. But this time Schäuble added a twist. It was true, he admitted, that German exports enjoyed a competitive advantage. The euro was undervalued. But it was not Germany that set interest rates or the value of the euro. It was the ECB. To the horror of German savers, Mario Draghi’s expansive policy of QE was driving European bond yields into negative territory and depressing the value of the euro. Visiting Washington in April 2017 Schäuble told American audiences that he had warned Draghi about the tendency of the ECB’s expansive monetary policy to inflate Germany’s trade surplus. 117 That it was causing tension with the United States was predictable. The ECB stood firm, and the IMF backed the continuation of QE in Europe. But Schäuble had served notice of how Trump’s attacks might be instrumentalized in the long-running argument over eurozone economic policy. The furor around Trump should not cause one to forget how bitterly Europeans and Americans had squabbled over economic policy in the “good” Obama years.

The ECB’s belated monetary expansion at a time of Fed tightening was a real source of transatlantic imbalance and it was a reminder of the disharmony over monetary policy that had marked the world economy since the onset of the crisis, a disharmony to which conservative voices in Germany had contributed as much as anyone. 118 Nor were the chronic surpluses of Germany, the Netherlands and China figments of the Trumpian imagination. They pointed to real and persistent imbalances in the world economy. In global trade policy as in so many other areas, the outrage caused by the uncouth belligerence of the Trump administration too easily obscured the reality of the problems it was gesturing toward. At the G20, the atmosphere was self-congratulatory. The WTO earned applause for seeing the world economy through the financial crisis of 2008 far better than it had fared during the Great Depression of the 1930s. There had been no catastrophic lurch toward high tariffs and protectionism. 119 There had been no repeat of the Smoot-Hawley tariff of 1930. The twenty-first-century system of global governance might not be popular, but it had worked, or so the story went. Ten years on from the crisis, it was, therefore, the height of populist irresponsibility to indulge in backbiting economic nationalism. For the defenders of the status quo, Trump made a perfect caricature enemy against whom to reassert the nostrums of liberalism. But this deflected attention from a more complex and ambiguous reality. The idea that Trump constituted a sudden and shocking break with a prevailing liberal success story depends on an unduly sanguine view of the global backdrop. This was as true with regard to trade as it was with regard to monetary policy. In fact, the last major effort to negotiate a global trade deal, the Doha round, had come to a crashing halt in the summer of 2008. World trade had recovered from the disaster of 2008–2009. But since 2010 trade volumes had stagnated. In 2015 they had declined. 120 This was driven in part by the business cycle. The taper tantrum and the setback to commodity prices had rocked the emerging markets. But it also reflected a wave of protectionist measures adopted by countries across the world, concentrated not on tariffs but on a variety of nontariff barriers. 121 No one imagined that Trump’s personal views on trade reflected arcane knowledge of new types of protectionism. He was regurgitating opinions first formed in the 1970s and 1980s. But if the expert staff around Lighthizer was looking for ammunition to demonstrate the reality of discrimination against US exports, it was ready to hand. Through tax breaks, subsidies and export credit systems, not to mention China’s state capitalism, world trade was increasingly shaped not only by corporate value chains, but also by state intervention. A large part of America’s huge trade deficit was accounted for not only by Chinese trade discrimination, but also by lost export earnings siphoned through offshore tax havens, located not only in the Caribbean but also in the EU. 122 In this respect too the once-robust assumption that globalization was an inevitable, natural process was losing its power to convince. Trump’s trade hawks did not advocate a return to the 1930s, but neither were they willing to continue the pretense that the naïve triumphalism of 1989 with its easy assumptions about the inevitable victory of democratic capitalism any longer “jived with the facts.” As the national security strategy issued in December 2017 darkly declared: “There is no arc of history that ensures that America’s free political and economic system will automatically prevail.” 123

V