Chapter 19

AMERICAN GOTHIC

A mid the banking crisis of 2008, the American motor industry had been collateral damage. With sales collapsing, GM and Chrysler were knocked to their knees. In December 2008 a truculent Congress voted down an emergency aid package, but neither Bush nor Obama thought they could let GM and Chrysler fail. These once great powerhouses of American industrialism were rescued by diverting funds originally allocated to the bank bailout. By 2013 both GM and Chrysler were back in profit. Like the rest of American big business, they weathered the storm and Chrysler celebrated its recovery in the way that corporate America does, by booking a slot to run a headline-grabbing commercial during the Super Bowl in February 2014. They wanted something that would make a splash and they commissioned the man to do it. The spot was written, directed and acted in person by Bob Dylan, the wizened bard of offbeat Americana. Against a backdrop of Hopperesque noir, Dylan delivered a striking piece of high-caliber nationalist kitsch:

Is there anything more American than America? ’Cause you can’t import original. You can’t fake true cool.

You can’t duplicate legacy. Because what Detroit created was a first and became an inspiration to the . . . rest of the world.

Yeah . . . Detroit made cars. And cars made America. Making the best, making the finest, takes conviction.

And you can’t import the heart and soul, of every man and woman working on the line.

You can search the world over for the finer things, but you won’t find a match for the American road and the creatures that live on it.

Because we believe in the zoom, and the roar, and the thrust. And when it’s made here, it’s made with the one thing you can’t import from anywhere else. American pride. So let Germany brew your beer, let Switzerland make your watch, let Asia assemble your phone.

We . . . will build . . . your car. 1

His lines were all the more resonant because of what the audience could be expected to know about the place where the spot was filmed, Detroit. If the American motor industry was back from the dead, the same could not be said for Motor City.

Since its heyday in the postwar era, Detroit had long been a city in decline. At its peak it had a population of 1.8 million, of whom 500,000 were African American. Hit by deindustrialization and white flight following the 1967 riots, by 2013 the population of the urban core of Detroit had shrunk to 688,000, of whom 550,000 were African American. They were left behind in a city that was literally falling into ruin, burdened with debts running into the tens of billions of dollars. With most of the major factories that had made it one of the industrial heartlands of the world closed down, Detroit was caught in a death spiral of unemployment, racial disadvantage and unsafe and predatory financing. 2 By 2013, 36 percent of Detroit’s population were classed as living below Michigan’s far from generous poverty line. The unemployment rate was 18 percent. The city was an extreme example of the doom loop in which public and private financial distress compounded each other. In 2005, of all the mortgages in Detroit, 68 percent were subprime. 3 As the crisis cut a swath across America, 65,000 homes in Detroit were foreclosed. Of those, 36,400 were considered of so little value that they were simply abandoned, joining a total stock of 140,000 blighted properties. Trying to contain the contamination effect, the city demolished entire tracts. Though it received state and federal subsidies for the house-razing program, it cost Detroit $195 million. That came on top of lost tax revenues of $300 million. 4 None of this could the city afford. Detroit appointed an emergency manager who in June 2013 filed for bankruptcy, with debts owing between $18 billion and $20 billion. It was the biggest city bankruptcy in American history. 5

As viewers of Dylan’s Chrysler spot knew, Detroit was an extreme case, but it was not alone. Former industrial cities and towns across America were struggling. A few went bankrupt. In 2011 Jefferson County, Alabama, which included the steel city of Birmingham, had filed. In 2012 it was the turn of Stockton and San Bernardino, California. These were poorly governed places, burdened with the side effects of America’s ramshackle welfare state, with economies struggling against long-term decline or the immediate impact of the real estate bust. They were far from being carbon copies of northern postindustrial Detroit. But taken together they symbolized the bewildering turn from American Dream to American nightmare.

It wasn’t new news. Already in the late 1970s, Bruce Springsteen had offered a mournful soundtrack for postindustrial America. 6 In 2006 Obama had reminded the bigwigs of the Hamilton Project of the harsh realities of “people in places like Decatur, Illinois, or Galesburg, Illinois. . . . This is not a bloodless process,” he had said. But for most of Obama’s first term it wasn’t the worries of such places that preoccupied economic policy. It was the fight to save Wall Street and global finance. The protests of 2011 and their politicization of inequality had begun to change the conversation, but it was in the eighteen months following Obama’s reelection in November 2012 that the sense of American malaise reached a new pitch. 7 With the crisis no longer dominating the horizon, the concerns about America’s long-term trajectory that had worried liberal centrists already in the early 2000s, the sense that things weren’t “normal,” came roaring back.

I

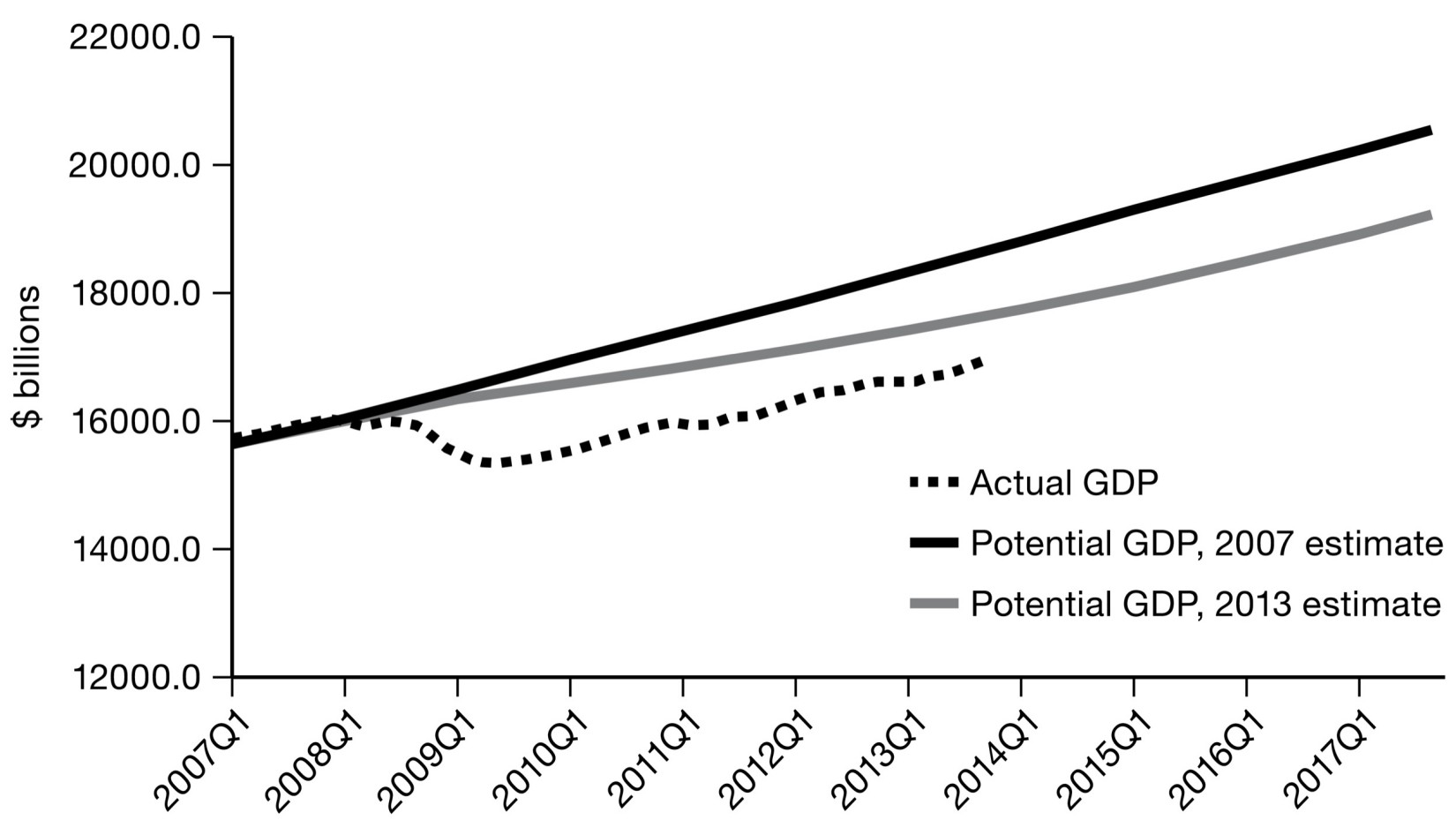

One unexpected but symptomatic manifestation was Larry Summers’s minatory speech at the IMF in November 2013. 8 His subject was the recovery and its deeply disappointing pace. American policy makers might congratulate themselves that they were leading the Europeans out of the recession and they were right to do so. Since 2010 Europe’s economic record had been even worse. But America’s own recovery was the slowest on record. On the “plucking model” of business cycles, after a downward shock as severe as that in 2008, one might have expected the rebound to be vigorous. In 2009–2010 the recovery had started strongly, but since then economic growth had relapsed to a depressing extent. Where was the “bounce”? What was wrong?

Growth Disappointing: Potential GDP Estimates of 2007 and 2013 Compared to Actual GDP (2013 Dollars)

Source: Taken from L. H. Summers, “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound,” Business Economics 49, no. 2 (2014): 65–74. Data: CBO.

The conventional view was that the United States was suffering from the aftereffects of an exceptionally severe financial crisis. This was no ordinary business cycle. It would take time for markets and balance sheets to recover. 9 It was precisely to avoid such hangovers that economists like Reinhart and Rogoff argued for financial restraint. If you avoided the credit bubble and the excessive upswing, you might avoid the bust. Keynesians like Krugman insisted that this was all very well, but the recovery had been needlessly slowed by the premature shift to austerity. As Krugman put it punchily, “[I]t all went wrong in 2010.” 10 The global shift to austerity for which Reinhart and Rogoff had been the cheerleaders reduced the recovery to an agonizing crawl. Bernanke’s QE could compensate to some degree, but it could not make up for the shortfall in aggregate demand.

These were the parameters of the economic policy debate familiar since 2009 and long before. What they did not capture was the sense that a deeper and more serious problem was afflicting America’s economy and the society built on it. The hypothesis that Summers suggested to his audience at the IMF in November 2013 was disconcerting and unfamiliar; so jarring, in fact, that Summers, who is not given to either modesty or self-doubt, acknowledged, “[T]his may all be madness, and I may not have this right at all.” But in light of the data, the question had to be put: What if the inadequate recovery was not simply down to policy failure? What if there was a deeper problem, a chronic shortfall in the demand for investment relative to the supply of savings, resulting in a sustained condition of “secular stagnation”?

To see the force of this argument, Summers invited his surprised audience to look back to the period before the crash. In retrospect, everyone agreed that monetary policy before 2008 had been “too easy. . . . [T]here was a vast amount of imprudent lending going on. Almost everybody believes that wealth, as it was experienced by households, was in excess of its reality. Too easy money, too much borrowing, too much wealth.” But if that were the case, one would have expected the American economy to have been on a dramatic bull run. It was not. Despite the excesses of the housing boom, growth up to 2008 had been average. Indeed, when compared with the 1950s and 1960s it had been slow, which is why places like Detroit were in such a precarious position. “Unemployment wasn’t under any remarkably low level. Inflation was entirely quiescent. So somehow, even a great bubble wasn’t enough to produce any excess in aggregate demand.” So imagine, Summers continued the train of thought, “how satisfactory” the performance of the US economy would have been in the early 2000s “in the absence of a housing bubble, and with the maintenance of strong credit standards.” It would have been just as disappointing as the current recovery was turning out to be. It might have been worse.

In an astonishing makeover of America’s recent economic history Summers proposed that for at least two decades American economic growth had been on weak foundations. To achieve no more than a “normal” rate of growth it had depended on “abnormal” financial bubbles. Looking back over recent decades, Summers asked in a subsequent speech, “[C]an we identify any sustained stretch during which the economy grew satisfactorily with conditions that were financially sustainable? Perhaps one can find some such period, but it is very much the minority, rather than the majority, of the historical experience.” 11 It was a remarkable indictment of the policy consensus of which Summers himself had been a defining figure. 12 It had dramatic implications for current policy. If America simply waited, the long-awaited rebound from the crisis of 2008 might never arrive.

To address the chronic shortfall in investment, what Summers advocated was a new era of government activism. The United States would not match China, of course. Nor was that appropriate. But the conditions were right for a big burst of public investment. This would rebuild America’s infrastructure, and in so doing it would address the more fundamental questions posed by Detroit. Physical reconstruction would be a means to restore a sense of national coherence and national pride. As Summers remarked on another occasion: “Look at Kennedy airport. It is an embarrassment as an entry point to the leading city in the leading country in the world. The wealthiest, by flying privately, largely escape its depredations. Fixing it would employ substantial numbers of people who work with their hands and provide a significant stimulus to employment and growth. . . . If a moment when the United States can borrow at lower than 3 percent in a currency we print ourselves, and when the unemployment rate for construction workers hovers above 10 percent, is not the right moment to do it, when will that moment come?” 13

Belatedly, what Summers was calling for was what Obama’s administration had failed to deliver, a concerted drive to unify American society around a sustained program of investment-driven growth and comprehensive modernization. The efforts at stimulus in 2009 and 2010 had not been negligible. But they had been hedged around by the anxieties of the moment, resistance from Congress, a spectacular and aggressive mobilization of right-wing opinion and Larry Summers’s own nervousness about losing standing with the savvy political operatives. The result was a recovery that was not just slow but deeply inequitable. If the shocking images of dilapidation in Detroit and other postindustrial cities around America were not enough, devastating statistical data completed the picture.

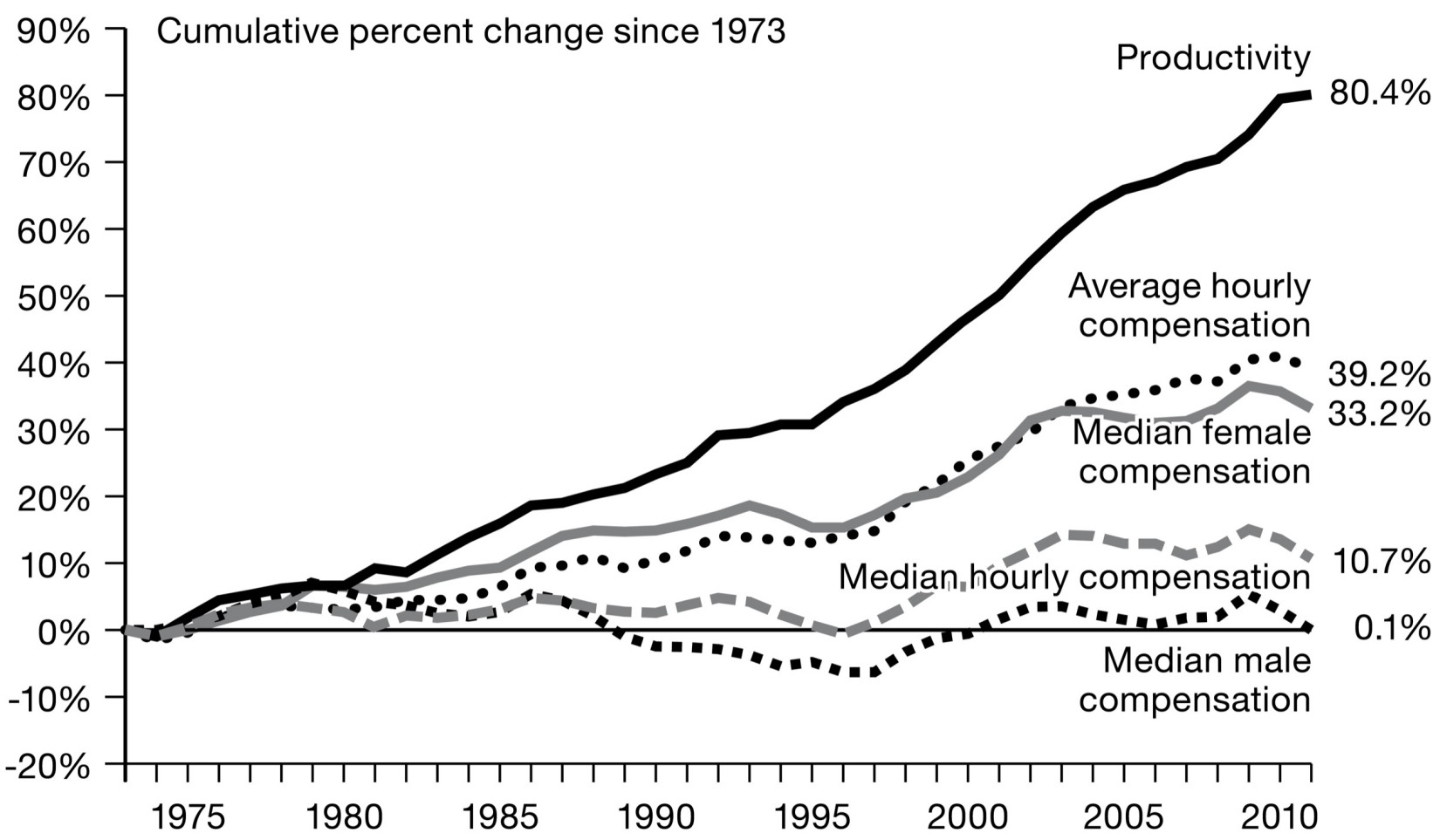

In October 2013 two French economists, one working in California, the other back in Paris, published the latest release of a long-running project on American inequality. 14 Emmanuel Saez and Thomas Piketty were at this point not unknown. An earlier paper in which they mapped top incomes in the United States over the long run had yielded the “We are the 99 percent” slogan that the Occupy movement had used to such good effect. 15 Nevertheless, the data they released in October 2013 were astonishing. From the latest round of tax releases they calculated that of the growth generated by the economic recovery since 2009, 95 percent had been monopolized by the top 1 percent. That tiny fraction of the population saw their incomes rebound from the trough of the recession by 31.4 percent. 16 Meanwhile, 99 percent of Americans had experienced virtually no gain in income since the crisis. The data were subsequently revised to show a less extreme disproportion. 17 But in 2013 the numbers were a sensation. The slow growth in GDP that worried Summers, in fact, hid two radically divergent realities. Whereas a tiny elite were doing extremely well, for average Americans the secular stagnation thesis that Summers advanced as a tentative academic hypothesis was simply the lived reality of the last forty years. Since America’s bicentennial in 1976, productivity growth, which drove overall economic growth, and the returns to labor in the form of household incomes had starkly diverged. The average American shared only to a small degree in national economic growth as measured by GDP statistics. Almost all the benefits of growth were being monopolized by the highest paid and those wealthy enough to own significant portfolios of financial assets. The financial crisis of 2008 had revealed how in extremis national economic policy was subordinated to the needs of a cluster of giant transnational banks. Now, in the face of a dismal recovery, the correspondence between economic growth and the progress of a national society was being challenged from the bottom up. Could the national economy any longer be plausibly presented as a project common to all Americans?

The Great Divergence: Labor Productivity and Compensation

Source: Lawrence Mishel, “The Wedges Between Productivity and Median Compensation Growth,” EPI Issue Brief 330 (2012): 1–7, http://www.epi.org/publication/ib330-productivity-vs-compensation/ .

II

The decay of the American Dream had been a staple of Barack Obama’s political discourse since his days as a junior senator. It was a common thread in the Hamilton Project agenda. In December 2013, a year into his second term as president, Obama visited a community center in Ward 8, an African American section of Washington, DC, to make a major speech about America’s ongoing social crisis. 18 He described the “daily battles” of ordinary Americans struggling against the “relentless decades-long trend” toward “dangerous and growing inequality.” The “basic bargain at the heart of our economy has frayed,” he declared. Of course, the trend toward growing inequality was not confined to America. But, Obama insisted, there must be no more evasion, “this increasing inequality is most pronounced in our country. . . . [S]tatistics show . . . that our levels of income inequality rank near countries like Jamaica and Argentina.” Comparable “wealthy allies, countries like Canada or Germany or France . . . have greater mobility than we do, not less.” Half of all Americans would experience poverty during at least one period of their lives. “The combined trends of increased inequality and decreasing mobility pose a fundamental threat to the American Dream, our way of life and what we stand for around the globe.” Inequality was, the president declared, the “defining challenge of our time.”

The racialized distress of cities like Detroit was clearly shocking. But, as Obama emphasized, America’s crisis was not confined to predominantly African American communities. Across the country, class, not race, was the most important determinant of an American’s life chances, and the big story of his second term as president was rural white working-class despair. It was Appalachia—West Virginia and Kentucky—held back by structural change, educational failure and immobility, that lurched into the headlines. At its most extreme, this lethal cocktail came to be symbolized by an epidemic of drug addiction, fed by cheap heroin from Mexico and rampant opioid abuse. 19 Already in 2007 deaths from drug overdose had overtaken road accidents as a major cause of death in the United States. 20 Among white Americans, deaths from overdose increased by 297 percent between 2010 and 2014 alone. Unlike in any other developed society, life expectancy among working-class white Americans had been decreasing since the early 2000s. In modern history the only obvious parallel was with Russia in the desperate aftermath of the fall of the Soviet Union. One journalistic essay and academic research paper after another confirmed the disaster, until the narrative was capped in 2015 by Anne Case and Angus Deaton’s famous account of “deaths of despair.” 21

The crisis was undeniable. The question was what to do about it. When the left wing of the Democratic Party had taken up the issue of inequality in the 1990s at the time of the Clinton administration, the standard diagnosis had been technical and economic. 22 Globalization had pushed top incomes up and lower incomes down. Since the 1990s, the impact of these factors had only increased. Imports of cheap manufacturers opened up by NAFTA and Chinese accession to the WTO benefited consumers, but depressed wages and robbed blue-collar Americans of secure manufacturing jobs and the health and retirement benefits that went with them. By 2013, experts close to the American labor movement estimated that the trade deficit with China had cost 3.2 million jobs and the competition of low-wage foreign labor had depressed the wages of the 100 million American workers without college education by $180 billion. 23 These were substantial effects, but in an economy with a workforce of more than 150 million and a wage bill of more than $7 trillion, they were nowhere near large enough to explain the huge surge in inequality. So globalization was supplemented by the thesis of skills-biased technological change. 24 This postulated that, independent of globalization and foreign trade, the trend in technological development had offered disproportionate benefits to those with higher skills in every walk of life and across the entire American economy, whether exposed to trade or not.

The standard reformist response was to advocate for a role for federal and state government in improving education, providing affordable access to community colleges and offering trade adjustment assistance. Hence, the focus of the Hamilton Project in 2006 on making sure that underprivileged kids made good use of their summer vacations. But after twenty years, given the mounting inequality and declining mobility, these measures could hardly be deemed a success. Disillusionment with conventional reformist solutions was a hallmark of the “new” inequality debate that sprang to life after 2011. Though there had been many well-intentioned efforts by government agencies to modify and improve the condition of average Americans, on balance their net effect had been modest, to say the least. Between 1977 and 2014 the share of national income going to the top 1 percent before taxes and benefits had risen by 88.8 percent. After fiscal redistribution their share increased by 81.4 percent. Nor did the tax and welfare state prevent the share of the bottom 50 percent from declining from 25.6 to 19.4 percent. 25 Nor was this by accident. Every conceivable source of leverage and influence had been exploited by those with money to maximize their advantage. As billionaire investor Warren Buffett famously put it: “Actually, there’s been class warfare going on for the last 20 years, and my class has won.” 26 Buffett was so appalled at the consequences that in 2011 he made himself into a spokesman for proposals to impose a minimum 35 percent tax on America’s highest earners, a proposal that Obama had backed but that had been blocked by the Republicans in Congress. 27 It was a sign of both Buffett’s personal decency and the utter lopsidedness of the balance of power in twenty-first-century America that a program of social improvement should consist of well-meaning billionaires volunteering to pay a bit more for the greater good of American society.

For those at the bottom of the pile, none of this was news. Opinion polls, especially those commissioned by the right wing, had for a long time been recording the profound resentment among the American population at the way that both the economy and the political system seemed to be engineered to their disadvantage. 28 These views were often dismissed as conspiracy theory, and often deservedly so. Online news sources like Breitbart, which rode to prominence on the back of the Tea Party movement, provided a platform for toxic racial and anti-Semitic rhetoric. 29 But if one stepped back from the poisonous language and crude logic, the assumptions that inequality was “systemic” and that “the system” was rigged against ordinary working-class Americans were not paranoid but simply realistic. From a radically different perspective and with completely different intent, the American Left had always made the case. Indeed, it was this radical skepticism that set them apart from the liberal centrists who dominated the Democratic Party. The Left did not trust the institutions. They did not believe that electing well-intentioned products of elite colleges to steer a machine designed to favor the wealthy offered any hope of fundamental change. As the Occupy slogan of 2011 put it, “The system isn’t broken, it’s rigged.” 30 In many ways the liberal centrists were the last to know. They, of all the segments of political opinion, had the most invested in the idea that America’s social ills were amenable to technocratic remedy and that the state was a suitable instrument for making such change. It was precisely the conversion of commentators of this ilk to a more radical view that marked how serious the sense of crisis had become. 31

In a remarkable series of articles following the 2012 election, Paul Krugman at the New York Times adopted a profoundly dark view of American society, economy and politics. “What do the pre- and postcrisis consensuses have in common?” Krugman asked in December 2013. 32 “Both were economically destructive: Deregulation helped make the crisis possible, and the premature turn to fiscal austerity has done more than anything else to hobble recovery. Both consensuses, however, corresponded to the interests and prejudices of an economic elite whose political influence had surged along with its wealth. . . . Some pundits [might wish to] depoliticize our economic discourse, to make it technocratic and nonpartisan. But that’s a pipe dream. Even on what may look like purely technocratic issues, class and inequality end up shaping—and distorting—the debate.” This from a Nobel Prize–winning economist who in the 1980s and 1990s had counted squarely in the mainstream.

Robert Reich, a former Clinton-era Labor secretary, underwent a similar disillusionment at exactly the same historical moment. “For a quarter century,” he now admitted, “I’ve offered in books and lectures an explanation for why average working people in advanced nations like the United States have failed to gain ground and are under increasing economic stress.” He had pitted an interventionist state against the forces of globalization and technological change. What Reich now recognized was that much of this was “insufficient,” if not “beside the point,” because it overlooked a “critically important phenomenon: the increasing concentration of political power in a corporate and financial elite that has been able to influence the rules by which the economy runs. . . . The problem is not the size of government but whom the government is for.” 33

After the events of 2008–2009 and the spectacularly lopsided bailouts, could anyone seriously doubt whom government was for? At the level of personnel, the revolving door that connected the Treasury, the Fed and the top banks continued to spin at a steady pace. By 2014 both Bernanke and Geithner were on their way from public service to well-upholstered positions in finance. Geithner went to the well-connected investment bank Warburg Pincus. Bernanke advises the Citadel hedge fund and chaired an advisory board for the giant PIMCO bond fund, owned by Allianz of Germany, which also included as its members Jean-Claude Trichet and Gordon Brown as well as Anne-Marie Slaughter of the Obama foreign policy team. 34 It was like a mini reunion of 2008 crisis fighters. And they had plenty to celebrate. Share values were recovering to their precrisis levels and beyond. The banks were rebuilding their balance sheets. As they piled up capital and reserves, rates of return in the financial sector were down. But, as the stress tests had always intended, pre-provision net revenue was bouncing back and the extra capital made the banks safer. America’s financial giants were expanding their businesses, pushing into markets vacated by their ailing European competitors. 35

Clearly, Wall Street enjoyed a privileged connection to government. After 2008 no one could doubt that. But what was striking in the aftermath of the crisis was how critical commentary on America’s political economy widened its scope beyond the banks. In so doing it followed the evolving contours of the economy itself. With the advent of the smartphone and social media boom in 2007, tech had regained the luster it had lost in the dot-com crash. Silicon Valley was the new cutting edge of American capitalism. Big Pharma continued to rake in profits. As oil prices resurged from their lows in 2009, big oil and the new technology of fracking were back. As the recession of 2008–2009 receded, what came ever more to the fore was a tendency toward concentration and oligopoly that went far beyond Wall Street. One of the side effects of Bernanke’s QE policy of low interest rates was that it made it hugely attractive for companies to borrow to buy out their competitors. In three giant merger waves, cresting in 2000, 2006 and 2015, with the antitrust authorities looking on, American capitalism remade itself in a more concentrated and monopolistic mode. 36 By 2013 profits were booming to an almost embarrassing extent. 37 Even chronic loss makers, like the airlines, were now making money. But the really big returns were elsewhere. As Peter Orszag, Obama’s former director of management and budget, now at Citigroup, and Jason Furman, serving as chair of the Council of Economic Advisers, reported in a research paper, two thirds of the nonfinancial firms that had managed to achieve a return on invested capital of 45 percent or more between 2010 and 2014 “were in either the health care or information technology sectors.” 38 What allowed such gigantic profits and enormous salaries to be concentrated in these sectors were market power, IP protection and government-licensed pricing. 39

Silicon Valley saw no need to apologize. Theirs was the great technological and entrepreneurial success story of the late twentieth and early twenty-first centuries. Antitrust, data protection and intrusive tax investigations were, as far as Tim Cook of Apple was concerned, nothing more than “political crap,” antiquated road bumps on the highway to the future. 40 As tech oligarch Peter Thiel told audiences and readers: “Creating value isn’t enough—you also need to capture some of the value you create.” That depended on market power. “Americans mythologize competition and credit it with saving us from socialist bread lines,” but Thiel knew better. As far as he was concerned, “[C]apitalism and competition are opposites. Capitalism is premised on the accumulation of capital, but under perfect competition, all profits get competed away. The lesson for entrepreneurs is clear . . . [c]ompetition is for losers.” 41

One could hardly ask for a more crass statement of robber baron hubris. The implications were bleak. America’s massively skewed distribution of income and wealth was the product of inherited assets, amplified by pervasive technological and economic change and Warren Buffett’s “class war,” which extended to every facet of the political regulation and deregulation of the economy. If this was so, what would it take to counteract the imbalance and to redress the astonishingly one-sided outcomes? A polite European social democrat like Thomas Piketty inferred from his inequality data that what the world needed was a global wealth tax. This was the message of his remarkable global bestseller, Capital in the Twenty-First Century , which redefined the public debate about inequality in 2014. 42 That would certainly help to offset the tendency toward massive inequality. But in a system as starkly polarized and lopsided as that of the United States, what relevance did such well-meaning suggestions have? The tax proposal wasn’t wrong. It just sidestepped the reason it was needed in the first place, the brutal struggle for privilege and power, which for decades had enabled those at the top to accumulate huge wealth, untroubled by any serious effort at redistribution. The answer, if there was one, was clearly not technical. It was political in the most comprehensive sense. Power had to be met with power.

In January 2014 Reich went to Congress to testify. “I’ve served in Washington, and know how difficult it is to get anything done unless the broad public understands what’s at stake and actively pushes for reform. That’s why we need a movement against economic inequality and in favor of shared growth—a movement on a scale similar to the Progressive movement at the turn of the last century that fueled the first progressive income tax and antitrust laws, the women’s suffrage movement that got women the vote, the labor movement that helped animate the New Deal of the 1930s and fueled the great prosperity of the first three decades after World War II, the Civil Rights movement that achieved the landmark Civil Rights and Voting Rights Acts, and the environmental movement that spawned the Environmental Protection Act and other critical legislation.” 43

Reich’s call to arms was powerful and compelling. To fix a rigged system, what was needed was a comprehensive mobilization. But as Reich was only too well aware, the progressive Left were not the only ones who could draw this conclusion. In fact, the American right wing got there first. Unlike liberal progressives, the libertarian right wing in the United States had never doubted that government was a problem. Indeed, they had always vociferously argued that it was the entire problem. America’s downward slide, the long-running trends toward inequality and oligarchy, the disaster of 2008, the lopsided recovery from it, were all symptoms of the profound corruption brought about by big government meddling and its capture by interest groups. Obama’s crisis politics were simply the latest phase. In response to Obama’s December 2013 inequality speech, Fox News speakers did not hesitate to mobilize the extraordinary Piketty and Saez data on the lopsidedness of the recovery, but only to turn them against the president: “He’s saying he wants to take out inequality and his policies from the beginning have been to equalize.” But what had happened to inequality under the Obama administration, the Fox anchors demanded to know. “[T]he top 1 percent—their income rose by 31.4 percent between 2009 and 2012. Income for everyone else, you know how much that grew? 0.4 percent. These are just facts here. 95 percent of income gains have gone to the top 1 percent. So this system that he’s talking about, he is the system. It’s his system!” 44

Of course the low top tax rates that had helped to create that outcome of extreme disparity were set by a Republican Congress and kept there by them. But the polemic was telling. A large part of the American Right agreed with Obama that the American Dream was in trouble, but for them, he was the personification of everything that was wrong. His defeat of Mitt Romney in 2012 only vindicated them in their belief that existing Republican politics were hopelessly inadequate. The Republicans would never achieve the transformation they craved with a candidate like Romney, an upper-class banker. In 2013, while the Democrats were still lulled by the sweet scent of Obama’s second victory, the Right counterattacked. Their target was the great social policy initiative of Obama’s first term, the Affordable Care Act. The hostage they would take was the budget.

III

In 2011 the Tea Party caucus had come close to forcing the United States into fiscal crisis. That had been avoided at the last minute by a compromise under which a bipartisan “super committee” would make recommendations on deficit reduction. When that failed to reach agreement in January 2012, it meant that automatic sequester cuts would be triggered in January 2013, affecting the entire government machine, including defense. 45 This nondiscretionary mechanism was popular with the Rubinite fiscal reform crowd. 46 Among the loudest and most influential voices for budget cuts was the coalition of business interests and Washington insiders gathered by Peter G. Peterson in the Fix the Debt campaign. 47 They had a strong preference for entitlement cuts and, given their suspicion of the kind of “political crap” that frustrated businessmen and policy experts alike, automatic sequester was far from being the worst of all possible worlds. As Obama’s ex–budget director Peter Orszag put the argument in October 2011 in the wake of the first budget showdown with the Tea Party: “To solve the serious problems facing our country, we need to minimize the harm from legislative inertia by relying more on automatic policies and depoliticized commissions for certain policy decisions. In other words, radical as it sounds, we need to counter the gridlock of our political institutions by making them a bit less democratic. . . . We need to jettison the Civics 101 fairy tale about pure representative democracy and instead begin to build a new set of rules and institutions that would make legislative inertia less detrimental to our nation’s long-term health.” 48

Unless something was done, the automatic cuts coming down the road in 2013 were huge—$563 billion in a single year, a contractionary antistimulus that might well trigger a new recession. To avoid this disaster, tense negotiations began in the hope of reaching a deal. The so-called grand bargain worked out between Obama and Boehner in 2011 was a lopsided demonstration of Washington’s rigged politics in action. It traded deep cuts in entitlements for some carefully chosen increases in taxes that would hit higher-income households but cushion “job-creating” and “growth-generating” businesses. To the Left it was outrageous. 49 The mainstream deficit-reduction campaign was riddled with conflicts of interest. Many of the most active exponents of entitlement cuts were lobbyists for targeted tax exemptions. As one cynical observer put it, “It’s easier to get face time in Washington as a deficit hawk than as a corporate hack.” 50 Meanwhile, the effort by Peterson lobbyists to present the austerity movement as a grassroots and youth-driven movement was exposed as a risible joke. The campaign included a bus tour of college campuses called “The Can Kicks Back,” a bizarre YouTube clip in which the venerable Senator Alan Simpson was persuaded to dance Gangnam style, and a cack-handed effort to deluge Congress with scripted letters from indignant teens protesting the debt burden their grandparents were threatening to pass down to them. It wasn’t so much grassroots as “Astroturf.” 51

Countering the posttruth of the mainstream austerity campaign made for good journalistic exposés. It also made sense for the Left to focus its fire on the likes of Peterson, Orszag, Simpson and Bowles, who were assumed to be the real power brokers in Washington. What no one reckoned with was the astonishing aggression and energy of the Far Right, which was not interested in reducing government so much as stopping it altogether. The Tea Party caucus inside the Republican Party was a small, determined and well-funded group. As far as deficit reduction was concerned, they would accept only spending cuts. And the spending they wanted to stop, in particular, was Obamacare, which they regarded as a lethal “socialist” threat to America’s future. The Republican leadership might worry about losing centrist votes. They knew that the budget crisis of 2011 had not played well with the electorate. But the most hard-core Tea Party advocates did not listen. To the Taliban of the Right, it was clear that Romney had lost because he was a moderate, compromising on immigration and health care. The only way to win back the electorate, at least the electorate in their gerrymandered Republican congressional districts, was to take the hardest line possible.

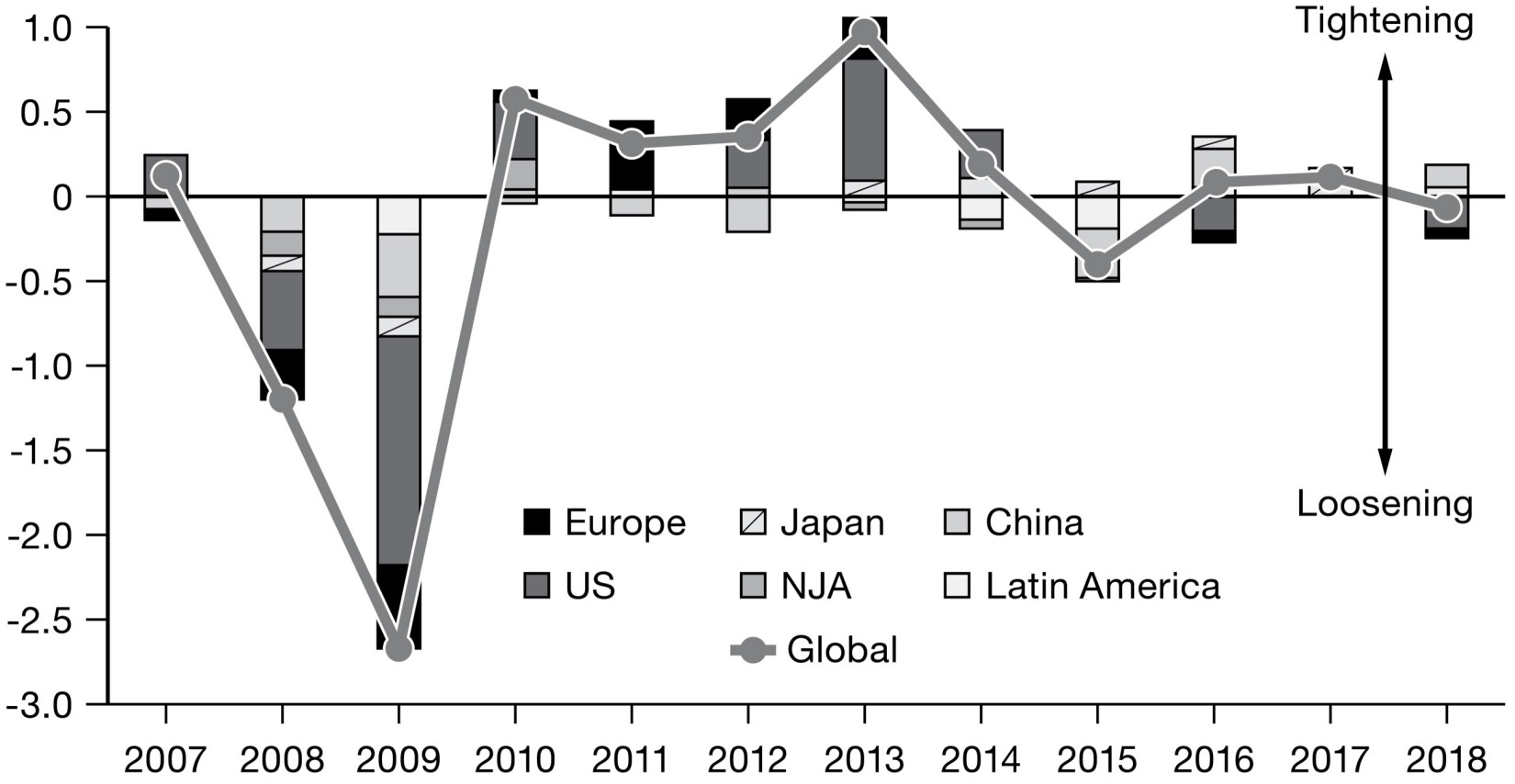

By January 2013 no cross-party agreement had been reached. The automatic sequester was put off for two months by stopgap legislation. Meanwhile, the debt limit was raised sufficiently to cover spending until May. With a substantial section of the Republicans agreeing to modest tax increases on the highest earners and on large inheritances, it seemed as though a crisis might be avoided. But the timeline was now pressing. On March 1 the sequester cuts came into full effect, hitting the budgets of the military, FEMA, the FBI, the FDA and the SEC. America’s apparatus of government began to go into hibernation. 52 In 2013 the sluggish economic recovery in the United States would be further slowed down by a fiscal tightening equivalent to almost 1 percent of global GDP. The United States moved from being significantly more expansive than the EU in 2008–2009 to being far more contractionary.

Global Fiscal Tightening or Loosening as % of Global GDP

Source: Credit Suisse.

Meanwhile, to keep basic government functions going, ad hoc spending authorizations were approved to cover the federal government through September. Crafting a proper budget for 2014 was more than Congress could manage. On March 21, March 23 and April 10, first the House, then the Senate, and finally the White House released separate budget proposals. The Senate and the White House were close together in terms of both the deficit reduction ($1.8–1.9 trillion over ten years) and the balance of spending cuts and tax increases they proposed. 53 The Republicans in the House were in a different world. They called for much bigger cuts ($4.6 trillion over ten years) to be achieved entirely by slashing spending. The House would not consider the Senate budget, and neither the Senate nor the House would vote on the White House proposal. The incoherence of US fiscal policy was reaching a new pitch. On May 19 the debt ceiling was reinstated at a level that covered borrowing since suspension in February but without provision for any new debt. The Treasury was, therefore, forced back on the expedients it had resorted to in 2011, raiding government cash tills and running down reserve funds. By mid-October the Treasury would run out of money and be forced to prioritize bill payments. It would be tantamount to a selective default. To prepare for this contingency, mainstream Republicans in May 2013 proposed a bill to ensure that at least the government’s bondholders were paid. 54 To John Boehner, the conventionally minded Republican leader in the House, this seemed like a sensible first step to order the federal government’s affairs in case of bankruptcy. But the Democrats had no interest in making the unthinkable more manageable, and the proposal that Chinese creditors should be paid ahead of serving military and social security recipients made easy political meat. The Full Faith and Credit Act was soon dubbed the “Pay China First Act” and voted down by the Democrats. Obama announced that he would veto the bill if it passed.

With the summer having gone by without any movement toward a deal, on September 25 the Treasury announced that it would run out of cash on October 17, 2013. Nancy Pelosi appealed to Boehner to remember the sacrifice that the Democrats had made to pass the TARP program for President Bush. 55 But that cut no ice with a Republican majority that did not remember the Bush years fondly and was terrified of being outflanked on their right wing by the Tea Party caucus, for whom TARP and the bailouts were anathema. With the Republicans demanding swinging cuts and privatization of Medicare, no deal could be reached, and on October 1, 2013, at 12:01 a.m. Eastern Time, the government went into partial shutdown, with up to 850,000 federal employees put on temporary unpaid leave. 56 The White House was forced to suspend the president’s foreign travel. At a meeting of APEC in Indonesia, the American president would not make his rendezvous with his Chinese counterpart. It was not until October 16, hours before the Treasury’s final deadline, that the Senate passed a continuing resolution to fund the government through February 2014, a temporary expedient with which the Republican leadership fell into line once they realized the political damage they were suffering from the standoff.

IV

Though a disaster was avoided, it is important not to normalize what had happened. The radical right wing of the Republican Party, xenophobic nationalists, many of them evangelical zealots, motivated by a worldview fashioned by the alt-right, or Pat Buchanan’s extreme America-first nationalism, a group whose hard core accounted for 10 percent of the House of Representatives, had threatened to paralyze the most important nation-state in the global system. As Steve Bannon, the editor of the Breitbart news site, a cheerleader of the Tea Party and a rising star of the alt-right, gushed to a Daily Beast journalist in November 2013: “I’m a Leninist. Lenin wanted to destroy the state, and that’s my goal too. I want to bring everything crashing down, and destroy all of today’s establishment.” 57 For the likes of Bannon, the crisis of 2008 and the bailout had marked a fundamental caesura in American history. The morning of September 18, 2008, when Bernanke and Paulson’s alarmism had scared President Bush into approving the TARP plan, was a fundamental turning point. It was a moment, according to Bannon, at which the threat of systemic collapse revealed the true power structure: “We are upside down; the industrial democracies today have a problem we have never had before; we are over-leveraged . . . and we have built a welfare state which is completely and totally unsupportable.” 58 Only a no-holds-barred struggle against the liberal elite and the state they had constructed in their image could save America. If this discomforted the failed Republican establishment as well, all the better.

To challenge the power structure, Robert Reich had called for a new progressive age, a new civil rights movement, a movement unafraid to question the status quo at all levels. That challenge had arrived, but it came from the Right, not the Left. The world was aghast. In Japan, Newsweek appeared on newsstands declaring “Ruined America—a Superpower Destroys Itself.” The Wall Street Journal reported on “Shutdownfreude” spreading across Europe, as for once it was America, not the eurozone, that was in the dock of global public opinion. 59 Der Spiegel commented bleakly: “The United States had embarrassed itself on the global stage. . . . Is this how a superpower behaves?” 60 One might respond that only a superpower could possibly afford to behave like this. But how long would the United States be able to uphold that position if it was internally so at odds that it was unable to decide whether to honor its debts or pay its soldiers? Predictably, Xinhua, China’s official news agency, took a dim view. Editorialist Liu Chang wrote: “As US politicians of both political parties are still shuffling back and forth between the White House and the Capitol Hill without striking a viable deal to bring normality to the body politic they brag about, it is perhaps a good time for the befuddled world to start considering building a de-Americanized world.” 61 On a lighter note, a Canadian comic living in China commented: “Chinese must be wondering: When will America embrace real reform? How long can this system survive? Where is America’s Gorbachev?” 62

Nor was it only foreigners who were worried. If the Tea Party would turn the Republican Party into a vehicle for an attack on the creditworthiness of US government, what was safe? So far the Tea Party had made Obamacare its main target. What would be next? By 2014 the Republican Right would block immigration reform and refuse to fund the Export-Import Bank, both priorities of American business. At the G20 the Americans were embarrassed to report that funding for the IMF was being held hostage by Republican opponents of abortion who wanted contraception excluded from Obamacare. 63 What if the Republican zealots targeted Fed independence or trade policy next?

Of course, there were business interests aligned with the Tea Party on tax and welfare issues. The coal lobby wanted environmental regulation stripped away. A clique of right-wing oligarchs saw the movement as the vehicle for a cultural and socioeconomic counterrevolution. 64 But with the 2013 budget fight, the mainstream of the American business leadership could no longer ignore the problem. Over the winter of 2013–2014, the Chamber of Commerce mobilized not to fight organized labor but to resist the Republican insurgency. “No fools on our ticket” was the Chamber’s slogan for the 2014 midterms, a euphemism for excluding the Tea Party. 65 A spokesman for the Chamber put it this way: “The crowd that wants to come to Washington and blow the place up and shut the place down, that’s a threshold issue for us. . . . We care about governing.” 66

By 2014 the signs of realignment were undeniable. While the Tea Party inveigled against “special interests” that had “come to dominate our political culture,” “self-serving politicians” and “the interfering strong hand of a powerful elite,” it was Democratic candidates who advertised themselves as “business friendly.” 67 As Senator Chuck Schumer of New York put it, “Democrats and business are on the same side on a range of issues. . . . The Tea Party has dragged the Republican Party so far to the right that business is now closer to mainstream Democrats than Republicans.” 68 The alignment that had first become clear during the bank bailout of 2008 was becoming something more entrenched. In the name of nationalism and the American Dream, the right wing claimed the cause of systemic change, while the Democratic Party establishment filled the middle ground the Republicans vacated. The question of the comprehensive progressive campaign to fight for greater equality was left begging.

Chapter 20

TAPER TANTRUM

T hat the astonishing events in Congress in 2013 did not lead to an immediate crisis in the bond market pointed to the resilience of the US Treasurys as the global safe asset of choice. Though the Chinese and Germans might complain and the market blipped, demand for US Treasurys quickly recovered. Ultimately, the market for IOUs drawn on the American taxpayer was underwritten by the Fed. Unlike the ECB, America’s central bank left no doubt that it backed its government’s debt. QE3 bond purchases provided immediate support, keeping prices up and rates down. This provided at least one point of stability for global investors. But after the events of 2013 questions could no longer be avoided. Was one of the unintended side effects of the stability generated by the Fed to free politics from market constraints and thus enable Republican extremism? Did America’s ability to ride out short-term budget crises like those of 2011 and 2013 lead contemporaries to underestimate the future dangers that the degeneration of American democracy might bring with it? And how long would the Fed’s technocratic interventions compensate for America’s lackluster economic recovery and the shambles in the legislative branch? How long could the Fed continue with QE3? When would the Fed begin tapering? Compared with the chaos in fiscal policy, these were, on the face of it, “normal” monetary policy questions, except that since 2008 there was no longer any such thing as normal monetary policy. The enormous expansion of the Fed balance sheet underpinned not just the US banking system but the entire global dollar system. Furthermore, the Fed had not just expanded its balance sheet, it had changed its composition. Buying up long-term securities in exchange for cash reserves, the Fed had absorbed onto its books the maturity mismatch that had undone the shadow banking system. After successive phases of QE, it was the Fed that held long-term securities that were matched against short-term liabilities such as cash and deposits by American and European banks.

Despite some nail biting by inflation hawks, this posed no immediate stability risk. The banks were happy to hold their cash reserves with the Fed. If interest rates went up, the Fed, as one of the largest holders of bonds, would suffer a capital loss. But this was more than made up for by the $350 billion in profits that the Fed paid to the Treasury between 2008 and 2013. 1 The real question was the likely fallout in the financial markets and money markets when the Fed changed its stance. Any move to moderate the Fed’s bond purchases, let alone to unwind its position, implied a comprehensive adjustment in the willingness of the markets to absorb not only a greater volume of bonds but also some of the maturity mismatch that the Fed was carrying. And that would have to happen at the same time as short-term interest rates were nudging up. If, on the other hand, the Fed continued QE3, its balance sheet would further inflate, bond prices would remain elevated, interest rates would remain stuck near zero and imbalances would further accumulate. In 2008 the Fed had embarked on a vertiginous tightrope walk from which there was no way back to the certainties of the great moderation.

I

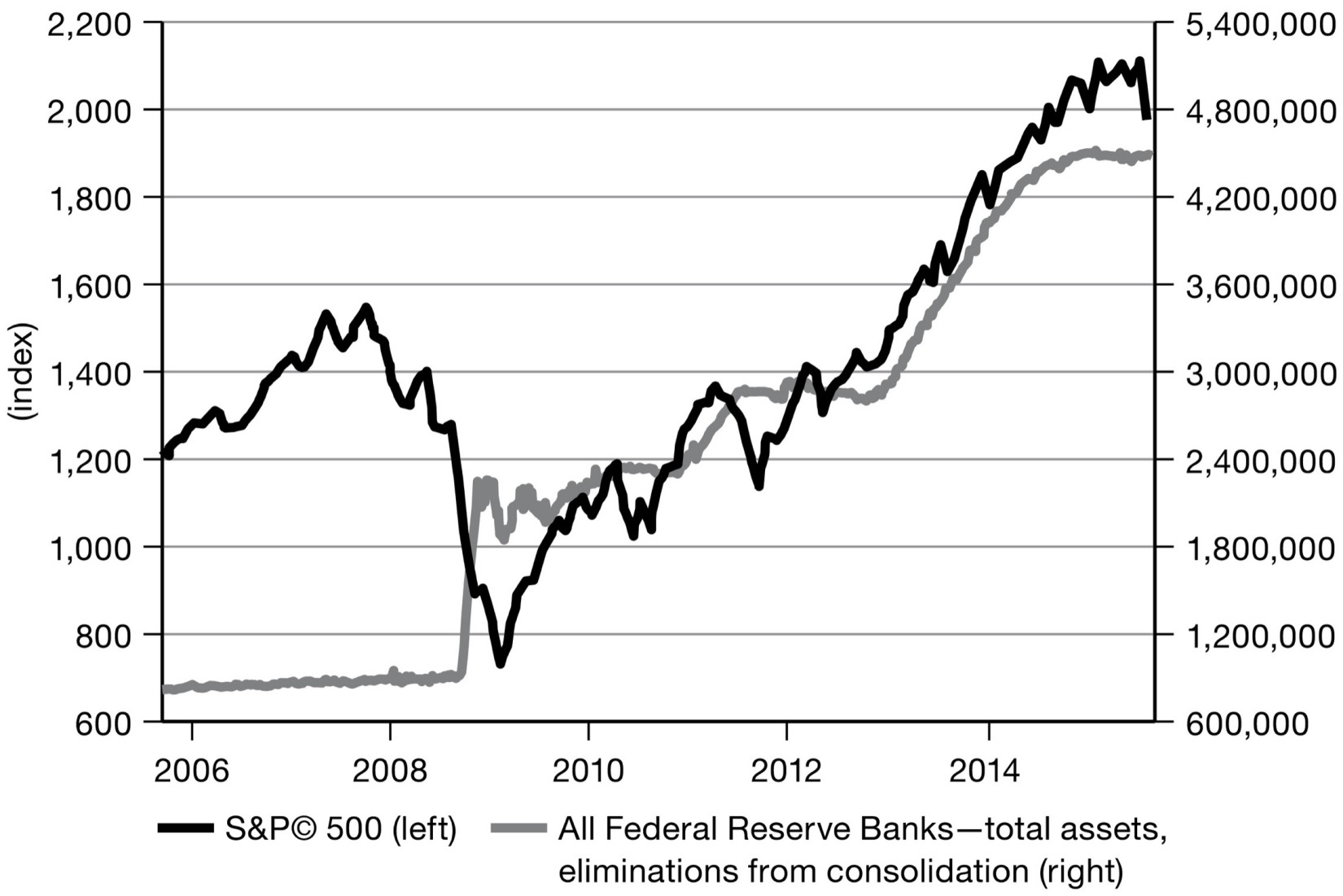

Both at home and abroad, the Fed’s low interest rate policy created a superheated investment climate. By its bond-purchasing program, which pushed up bond prices and depressed yields, the Fed incentivized investors to shift out of bonds and to place their funds in higher-risk, higher-return assets. How far this impulse actually went to explain the stock market boom is debatable. The econometric evidence is strongest for the impact of QE1 in launching the first phase of the stock market recovery in 2009. 2 But for the average Wall Street booster, the visual association between the Fed’s balance sheet and the surging value of the S&P 500 was plenty to be going along with. As a strategist for Citigroup told the Financial Times, “Everything revolves around monetary policy. It’s not the underlying economics that’s driving things, it’s central bank liquidity.” 3 In 2008 the Fed had intervened to stop the market from imploding. It had pumped trillions into the financial system. Now the markets hung on its every word.

Propping Up the Markets? The Association (Possible Spurious) of the S&P 500 and the Fed’s Balance Sheet

Source: Federal Reserve Economic Database (FRED).

Investors looked for higher yields not just in US equities but further afield. Dollars were cheap for everyone. Any investor who was willing to take a gamble on exchange rate movements could borrow cheaply in dollars and invest in high-yielding emerging markets. Assuming the dollar did not sharply appreciate before the debt was due, it would be a profitable carry trade. 4 By the middle of 2015, governments and businesses outside America would pile up $9.8 trillion of debts denominated in dollars. 5 Much of this went to rich, developed world economies. But $3.3 trillion was owed by emerging market borrowers, both government and private. From the point of view of the yield-chasing investor, the more exotic the securities the better. In September 2012 Zambia issued its first dollar-denominated bond. With a modest 5.6 percent coupon, a $750 million offering attracted more than $11 billion in bids. 6 A year later a state-backed tuna-fishing venture in Mozambique raised $850 million. Altogether, African sovereign borrowers garnered $17 billion in bond funding in 2012–2013. 7 In May 2013 the boom reached its peak, with the $11 billion ten-year bond issued by Petrobas, Brazil’s state-owned oil company. It was the largest bond issue ever by an emerging market corporation. Demand was so great that the yield on the Petrobas issue fell to as little as 4.35 percent, less than many sovereign borrowers. 8

This global interest in emerging market debt was exciting from the point of view of the borrowers. But it also exposed them to serious risks. Huge, aggressively managed funds crowded into tight markets. As the IMF pointed out, given that the largest five hundred asset management companies had more than $70 trillion in their portfolios, a 1 percent reallocation implied a flow in or out of an asset class of $700 billion. This was enough either to swamp or to starve the emerging markets. The withdrawal of funds that had caused such stress in 2008 around the periphery of the world economy had amounted to only $246 billion. The unprecedented inflow that transformed the outlook of those same economies in 2012 was $368 billion. 9 This disproportion created risk for the borrowers. But it was potentially bad news for the investors as well. If there was to be a sudden wave of withdrawals, the small size of emerging financial markets would amplify the stampede effect. 10 If the Fed reversed its policy and money flooded back to the United States, who would be the first to sell? Who would get out without fatal losses?

According to BIS data, professionally managed funds increased their stake in emerging market equity and bonds from $900 billion to $1.4 trillion between 2008 and 2014. 11 Set against global totals running into the tens of trillions, those were not huge numbers. But they were comparable to the stock of toxic subprime assets, which had caused such havoc in 2007–2008, and to the debts of Greece, Spain and Ireland, which had destabilized the eurozone in 2010–2012. After subprime and after eurozone sovereign debt, were emerging markets to be the next volume in the “trilogy” of debt crises? 12

Not for nothing the financial officials of booming emerging markets like Brazil complained about the influx of hot money from the United States. At the G20 in Seoul in November 2010 they had lambasted Bernanke for adopting QE2, dropping US interest rates and allowing the dollar to slide. By 2013 many emerging markets had gone beyond the war of words to adopt capital controls. Brazil, South Korea, Thailand, Indonesia all took steps to slow the inflow of funds and curb the appreciation of their currencies. Fifteen years earlier in the heyday of the “Washington consensus” this would have put them beyond the pale. Restraining international capital movement was a retreat from the most fundamental liberalizing policy of the 1970s and 1980s. But the advocates of the market revolution had foreseen neither the emerging market crises of the 1990s nor monetary policy on the scale of QE. Faced with the giant flux of the global credit cycle, amplified by spillover effects from the Fed’s crisis fighting, controls on capital inflows were grudgingly accepted as a pragmatic necessity, even by the IMF. 13 It was, the Economist magazine commented, “as if the Vatican had given its blessing to birth control.” 14

II

As far as the markets were concerned, everything depended on when and how the Fed changed course. Back in September 2013 Bernanke had made the giant bond-buying program of QE3 that was soaking the world in dollar liquidity conditional on America’s labor market. He had promised that interest rates would stay at rock bottom until unemployment fell below 6.5 percent. In the spring of 2013, with the US economy beginning to edge toward that threshold, the Fed began to drop hints. The moment was approaching at which it would consider slowing the pace of asset purchases. It was a delicate game. The Fed didn’t want to “taper” too abruptly. The labor market was not yet fully recovered. The sluggish recovery that was troubling Larry Summers might not withstand a sudden spike in interest rates. For the investors, on the other hand, it was crucial to be ahead of the game. If they knew that the Fed was going to raise rates in the foreseeable future and that bond prices would fall, they wanted to be the first to sell. Of course, no one could know for sure whether the Fed would indeed begin to taper or precisely when. So another reason to sell was to test the Fed’s resolve. As Richard Fisher, chair of the Dallas Fed and himself a former hedge fund manager, put it to the Financial Times in characteristically colorful terms: “Markets tend to test things. . . . We haven’t forgotten what happened to the Bank of England [when George Soros broke the pounds peg in the ESM in September 1992]. I don’t think anyone can break the Fed . . . but I do believe that big money does organize itself somewhat like feral hogs. If they detect a weakness or a bad scent, they’ll go after it.” 15 For Fisher, given this tendency to herding, it “made sense” for the Fed “to socialise the idea that quantitative easing is not a one-way street.” But given the likely impact on the fragile recovery of a large step up in interest rates, Fisher did not expect Bernanke to go from “Wild Turkey to ‘cold turkey’ overnight.” The feral hogs should beware of getting ahead of themselves.

On May 22, 2013, Bernanke took the plunge. He told Congress, “If we see continued improvement and we have confidence that that is going to be sustained, then in the next few meetings, we could take a step down in our pace of purchases.” 16 The markets skipped a beat. Then, at 2:15 p.m. on June 19, 2013, Bernanke made a more specific announcement. Conditional on continued positive economic data, the FOMC would vote on scaling back its monthly bond purchases from $85 billion to $65 billion at the upcoming September 2013 policy meeting. The bond-buying program might wrap up entirely by mid-2014. Despite weeks of preparation, Bernanke’s statement triggered a full-scale “taper tantrum.” In a matter of seconds yields surged from 2.17 to 2.3 percent. Two days later they had risen to 2.55 percent and would peak at 2.66 percent. These were small changes in absolute terms, but amounted to an increase in interest costs of almost 25 percent and inflicted a correspondingly serious capital loss on bondholders. US equity markets reacted in sympathy, losing 4.3 percent in a matter of days.

In the emerging markets Bernanke’s May announcement had already been enough to provoke a violent reaction. If the Fed reduced its purchases, bond prices began to ease and yields nudged upward, the emerging markets would come under a double pressure. Not only would their rates have to adjust by at least the same amount as the United States, but they would face an amplification effect through the exchange rate. As the Economist explained, a “stock of dollar debt is like a short position,” i.e., a speculative position assuming that the dollar exchange rate will either remain level or fall. 17 A Fed interest rate increase signaled not only higher borrowing costs but a likely upward movement in the dollar. Exposed emerging market borrowers would run to cover their dollar exposure, amplifying the currency adjustment and increasing the pressure on other dollar borrowers. Already in the spring of 2013, as markets began to worry about Bernanke’s next move, the emerging markets felt the pressure. For the emerging markets the funding boom was over. The exchange rates of what Morgan Stanley dubbed the “Fragile Five”—Turkey, Brazil, India, South Africa and Indonesia—declined precipitously. Western investors pulled their money. 18 Interest rates went up to counter the “vacuum cleaner” effect of Fed policy. 19 Capital controls put in place to curb excessive inflows did not prevent foreign money from leaving. But they limited the scale of the damage. As one Brazilian central banker remarked: “We knew this was going to come, and we prepared ourselves.” 20

Stern American observers noted that the global credit cycle was not fate. 21 Countries that had allowed their currencies to appreciate had been subject to a smaller inflow of funds. Nor, when the global credit cycle reversed, did everyone lose funding at the same pace. Among the emerging markets the hardest hit were those with less than fully sound financial positions. The Fed tightening was going to be tough for everyone, but if they did not put their budgets in order, they had only themselves to blame. 22 That made sense as a moral message and it conveniently deflected responsibility from the United States. It was up to the emerging markets to look after themselves. But it did not turn out to be well supported by the evidence. The biggest losers among the emerging markets, in fact, tended to be those that had attracted the largest foreign inflows, which also tended to be those with the most solid financial records. 23 In any case, home truths about fiscal discipline came late for those now facing a funding squeeze. Some buckled down. Raghuram Rajan, the onetime critic of financial market euphoria and former chief economist of the IMF, now earned his spurs as India’s central bank governor by raising rates and stabilizing the rupee. 24 But the taper tantrum was a test of political as well as financial resilience. Not all governments responded with equanimity to such abrupt external pressure.

When QE taper talk hit the Turkish currency in May 2013, President Erdoğan was struggling with a dramatic domestic challenge as protesters clashed with riot police in Istanbul’s Gezi Park. 25 Erdoğan had no doubt about how to interpret this coincidence. It was no coincidence at all. The internal political and external financial pressures on his government were part of a “conspiracy by unspecified foreign forces, bankers, and international and local media outlets” to push for regime change. 26 For Erdoğan, the pressure was being applied to all the countries that dared to claim a new place for themselves on the world stage—countries like Brazil and Turkey. “[T]he symbols are the same, the posters are the same, Twitter, Facebook are the same, the international media is the same. They are being led from the same center . . . the same game, the same trap, the same aim.” The masters of social media in Silicon Valley, the crusading liberals at the State Department and the Fed were all in on it. In an inflammatory speech he denounced the connections between Turkish private banks, international capital groups and, according to at least one report, Israel. “Who won from these three-week long [sic] demonstrations?” President Erdoğan asked. “The interest lobby won. The enemies of Turkey won.” 27 Foreign experts might insist that Turkey had simply to put its economic house in order, but Erdoğan had other ideas. Frustrated with the EU’s failure to proceed with Turkish accession negotiations and the Obama administration’s failure to act in Syria, he lurched toward Moscow. Turkey, Ankara let it be known, would welcome membership in the Economic Cooperation Organization founded by Russia and China in Shanghai. 28 Compared with the capricious West, the Russia-China axis seemed to promise stability.

At the G20 in Saint Petersburg on September 5–6, 2013, as the world waited to see how the Fed’s Open Market Committee would vote, the tone was more measured than that from Ankara, but the message was loud and clear. The Fed needed to acknowledge that everyone, including the United States, was living in an “interdependent world.” The finance ministers of both Brazil and Indonesia demanded more clarity from Bernanke. China, which was exposed to the United States not just through trade but also through its giant dollar bond holding, was no less vociferous. As one official spokesman put it: “Given that U.S. monetary policy has a huge influence on emerging markets and the global economy, we hope that U.S. monetary policy authorities, whether exiting or scaling down stimulus, will not only consider the U.S.’s own economic needs but also think about economic circumstances in emerging markets.” 29 Rajan was the emerging market spokesman with the highest personal profile in the United States. During the crisis of 2008, he reminded America, the emerging markets had undertaken “huge fiscal and monetary stimulus” in support of global growth. The industrialized countries could not now “wash their hands . . . and say we’ll do what we need to and you do the adjustment. . . . We need better cooperation and unfortunately that has not been forthcoming so far.” 30

“Interdependence” was one of the nostrums of the age of globalization. And it was all very well to call for greater cooperation. But why should the Fed listen to such demands? In 2008 it had provided liquidity to the entire world economy. Now it was doing its best to sustain the revival. But its mandate was national. It was responsible for the American economy, not the wider world. As far as the Fed was concerned, the really compelling argument was that of blowback. This was what had clinched the case for the massive swap line action in 2008. And this was the point made in the fall of 2013 by IMF managing director Christine Lagarde. The reverberations from the Fed’s huge monetary shocks, she warned Washington, “may well feed back to where they began,” i.e., back on the United States. 31 But it was one thing for the Fed to acknowledge that Europe’s megabanks might bring the house down. It was quite another to make the same claim for the emerging markets. Looking at the numbers, no one could seriously argue that the business cycles of Indonesia or India had much impact on US financial stability. 32 The interdependence of the global age was all pervasive, but it was emphatically not symmetrical. Some received shocks, others dealt them out.

In any case, given that Republican insurgents were in the process of shutting down the federal government, and were eyeing the IMF’s budget as a potential hostage, it would have been politically disastrous for the Fed to acknowledge that it was conditioning its latest policy move on business conditions in Indonesia. Instead, the protests from the emerging markets provided a convenient occasion for the Fed to make a stout show of American patriotism. As Dennis Lockhart, president of the Atlanta Fed, reassured Bloomberg TV in August 2013: “You have to remember that we are a legal creature of Congress and that we only have a mandate to concern ourselves with the interest of the United States. . . . Other countries simply have to take that as a reality and adjust to us if that’s something important for their economies.” James Bullard of the Saint Louis Fed emphasized the same point: “We’re not going to make policy based on emerging-market volatility alone.” 33

III

Then, on September 18, came the Fed’s long-awaited decision. After the buildup since May, the FOMC announced that it would leave interest rates where they were and continue bond buying at the current rate, pending “more evidence that progress will be sustained.” 34 The taper, the prospect of which had been giving the markets jitters since May, was off.

The decision to change nothing unleashed a frenzy of interpretation not about the likelihood of tapering but about why it had not happened. Were the doves on the Fed board resisting an interest rate shock? Had Bernanke got cold feet? Was he kicking the can down the road for his successor to deal with? 35 Or was the Fed consistent in its policy, but bad at forecasting? Between the spring of 2013, when it began to think about tapering, and September, when it decided to postpone it, the Fed had adjusted its forecast for economic growth sharply downward. 36 If the economy was recovering less strongly than expected, this would rescue the Fed’s reputation as a consistent policy maker, but at the price of undermining confidence in its forecasts and highlighting the downturn in expectations. Or was the Fed neither cowardly nor a bad forecaster? Was it playing a subtle tactical game? If it was committed to ensuring that the US economy completed its slow recovery without interruption from a premature and violent increase in rates, it needed to know how severely bond markets would react to a reduction in monetary stimulus. The evidence of the taper tantrum in June 2013 was clear. The markets were impatient. Investors would rapidly tighten credit conditions on any hint of movement by the Fed. If the Fed believed that what was necessary was something more gradual, then after the initial tapering announcements in May and June, it needed to shock markets a third time in the opposite direction, letting them know that though tapering was coming, it was not a one-way bet. 37

Four different interpretations: Fed politics, Fed weakness, Fed forecasting error, Fed game playing. Which was it? How were markets to know, and without knowing, how were they to react? Given the Fed’s hesitancy, one might have expected the bond vigilantes to take up the fight. There was profound hostility to Bernanke among the more militant investor crowd. In October 2013 Larry Fink, the CEO of BlackRock, the largest asset manager, accused the Fed of feeding “bubble-like” market conditions. 38 His chief investment officer for fixed income complained that there were “tremendous distortions” building in interest rates. 39 But there was no unanimity in the market. Bill Gross at Allianz-PIMCO argued that investors should accept the inevitable. If the aim of the Fed was to engineer a gradual exit from the gigantic debt bubble of the boom years—what Ray Dalio at the Bridgewater hedge fund called “beautiful deleveraging”—bond investors would have to accept that this came at their expense. 40 They should abandon their expectation of an imminent increase in rates. “Right now the market (and the Fed forecasts) expects fed funds to be 1 percent higher by late 2015 and 1 percent higher still by December 2016. Bet against that. . . . In betting on a lower policy rate than now priced into markets, a bond investor should expect a certain pastoral quietude in future years, much like that grazing cow, I suppose. Not that exciting, but what the hay, it’s an existence! . . . Mother Nature nor Mother Market cares not a whit for your losses nor your hoped for double-digit return from an equity/bond portfolio that is priced for much less. Be a contented cow, not a voracious crow, and graze wisely with increasing certainty that the Fed and its forward guidance is your best bet for survival.” 41

With trillions of dollars at stake and markets feverishly trying to second-guess the Fed’s policy, was Bill Gross’s pastoral image not wishful thinking? Rather than a herd grazing contentedly, to the Financial Times it seemed that relations between the markets and the Fed were increasingly coming to resemble the contorted psychodrama of a rocky marriage. Investors might take Gross’s advice and “practice believing that central banks love me.” But the refrain hid deep tensions and uncertainties. For the past five years, under the influence of massive Fed stimulus, investor strategies had come to resemble one another, leaving them to second-guess themselves, one another and the central bank: “What are you thinking? What are you feeling? What have we done to each other? What will we do?—a refrain equally applicable to a concerned policy maker as a nervous husband. . . . The whole thing reeks of a marriage built on shaky foundations.” 42 At any given moment the balance might be upset by a shift in policy or a market mood swing. The consequences for the entire global economy would be “deeply unpredictable.” 43

IV

“I will practice believing that the Fed loves me” was also the prescription that foreign central bankers would have to follow. The decision not to halt QE3 eased pressure on emerging markets. India’s rupee, which had been hardest hit by the taper tantrum, rebounded from 68 to the dollar to 61.9 to the dollar in early October. 44 Indonesia’s currency stopped its precipitous slide. This was a relief. But Rajan and his colleagues would have to believe that the Fed bore them in mind despite the fact that Congress jealously watched over the Fed’s exclusively American mandate and despite the fact that the Fed had made its decision while ostentatiously flaunting its indifference to the rest of the world. All the more significant was what the Fed did behind the scenes. On October 31, 2013, in the weeks following the September taper pullback and the congressional budget standoff, the Fed, the ECB, the Bank of Japan, the Bank of England, the Bank of Canada and the Swiss National Bank made a low-key, joint announcement:

“[T]heir existing temporary bilateral liquidity swap arrangements are being converted to standing arrangements, that is, arrangements that will remain in place until further notice. The standing arrangements will constitute a network of bilateral swap lines among the six central banks. These arrangements allow for the provision of liquidity in each jurisdiction in any of the five currencies foreign to that jurisdiction, should the two central banks in a particular bilateral swap arrangement judge that market conditions warrant such action in one of their currencies. The existing temporary swap arrangements have helped to ease strains in financial markets and mitigate their effects on economic conditions. The standing arrangements will continue to serve as a prudent liquidity backstop.” 45

The swap lines that had been so crucial to stabilizing global financial markets and which had been uncapped in October 2008 were now being established on a permanent basis. 46 As in 2008, this network had limits. None of the most fragile emerging markets were included in the inner core of the Fed’s swap network. But they were not left out in the cold either. What began to take shape were regional subnetworks. These were uneven. There was nothing of note around the core European central banks. But in Asia the central banks were more active. In September 2013, as anxiety about the Fed’s tapering rose to a crescendo, India negotiated an increase in its existing swap line arrangement with Japan from $10 billion to $50 billion. In December Japan doubled the swap line facilities it offered to Indonesia and the Philippines and announced that it would be looking to negotiate similar bargains with Singapore, Thailand and Malaysia. 47 Japan’s enormous reserve holdings of dollar assets, second only to those of China’s, gave it the means to offer such facilities. And in the event of a crisis, the Bank of Japan could always draw on the Fed. Thus dollar liquidity would percolate out through the entire system.

As in 2008–2009, in 2013 the public bluster about the need for a new monetary order and a “de-Americanized world” distracted from the reality that a powerful new network of liquidity provision was being rolled out across the world economy. The swap-lines story stayed buried on the interior pages of the Financial Times and the Wall Street Journal . 48 There was no fanfare, no new Bretton Woods Conference. There was also no congressional or parliamentary approval. These were administrative measures. But they were also far more than that. Five years on from the crisis, while markets remained unsettled and the American political system was racked by dissension, the global dollar system was being given a new and unprecedentedly expansive foundation.

About the technical efficacy of the swap lines there was little doubt. Their political legitimacy was a different matter. And in the autumn of 2013 one couldn’t help thinking of another of America’s technical systems of power that had been revealed earlier that year: the NSA’s electronic surveillance network. 49 The network that Edward Snowden exposed in early June also centered on US power and technological capacity. It too was no American monolith. Like the Fed, the NSA worked through local agencies. It too promised to provide a blanket of security for the United States and its allies. Of course spying and exchanging currencies were not the same things. But they did have in common that their functional power and administrative efficacy were not matched by anything resembling public political authorization. They were testimony, at one and the same time, to the continuing significance of US global power and the difficulty in justifying that power in public either in the United States or in the countries whose governments and business interests were enrolled in America’s network.

Chapter 21

“F*** THE EU”: THE UKRAINE CRISIS

B efore 2008 the driver of crisis was expected to be the balance of financial terror between the United States and China. A huge unwinding of the global disequilibrium centered on China and America and driven by profound domestic imbalances in each of them would, it was feared, rock American power to its foundations. In 2008 the expansion of the EU and NATO in the face of Russian opposition had added another dimension of risk. Georgia and Russia had clashed and Moscow had approached Beijing to mount a joint attack on America’s fragile finances. Beijing had held back. There was no great dollar selloff. The geoeconomic course of the crisis took an unexpected and innovative direction. The Fed’s liquidity swap lines stabilized the dollar-based financial system. In November 2008 the upgrading of the G20 had added a global leadership forum and this had been important in legitimizing the dramatic expansion of IMF resources in 2009. This backstopped the IMF’s urgent engagement in Eastern Europe. A year later, remarkably, the IMF would find itself committing hundreds of billions of dollars to rescuing the eurozone. At the same time, the United States was aggressively pushing a new system of regulation for global banking through the normally slow-moving Basel Committee.