Chapter 16

G-ZERO WORLD

T he commitment to austerity in 2010 drove critical economists to impatient fury. Why was the world embarked on a course that was so self-evidently counterproductive and so damaging to the prospects of tens of millions of unemployed around the world? Whose interests were being served by preserving this reserve army? Paul Krugman asked in the New York Times . 1 Whose interests were served by a lopsided deficit debate in which minor tax increases were traded for huge cuts in entitlements? What kind of shock would it take to break this impasse? Historical experience was not encouraging. FDR’s New Deal had not been enough. It had been hobbled by its own timidity and by relentless opposition from the Right. 2 To unleash the full capacities of the American state it had taken the national emergency of a war. “The fact is,” Krugman insisted, “the Great Depression ended largely thanks to a guy named Adolf Hitler. He created a human catastrophe, which also led to a lot of government spending.” 3 That didn’t mean that Krugman was hoping for World War III. But he couldn’t resist telling Playboy magazine that “[i]f it were announced that we faced a threat from space aliens and needed to build up to defend ourselves, we’d have full employment in a year and a half.” In light of events in 2011, one can’t help wondering whether Krugman assumed too much coherence in twenty-first-century politics.

The year, in fact, began with a geopolitical earthquake: the Arab Spring. And true to Krugman’s script, this triggered military intervention and calls for a Marshall Plan for the Middle East. 4 But after Afghanistan and Iraq there was no appetite anywhere in the West for nation building in foreign lands. Among conservative commentators, alarm at the overthrow of friendly Arab dictators mixed with the dismayed reaction to Bernanke QE’s to form a heady cocktail. A Wall Street Journal op-ed drew comparisons to the 1970s, when global inflation had helped to trigger the fall of the shah and Khomeini’s revolution in Iran. 5 Now, by “printing money” and driving up commodity prices, it was the Fed’s QE program that was destabilizing the world. As the Tunisian and Egyptian dictatorships toppled, conservative social media activists urged their followers to tweet “Bernanke has blood on his hands.” 6 Meanwhile, the liberal press fired back: It wasn’t monetary policy that was responsible for high commodity prices and food riots, it was global warming. That riposte allowed Paul Krugman to equate conservative opposition to quantitative easing to climate change denial. 7 It wasn’t so much a serious debate about the Arab Spring as indicative of the increasingly unhinged quality of American political discourse.

Europe was closer to the North African drama, but its reaction was hardly more coherent. France, Britain and Germany fell out over the NATO intervention in Libya, with Germany siding, as it had done at the Seoul G20, with China and Russia. Merkel’s government refused to give its vote in the UN Security Council for the aerial campaign against Gaddafi. Meanwhile, the EU squabbled disgracefully about who should accommodate the desperate refugees and migrants who poured through Libya into Italy. It was a dispiriting accompaniment to the rolling crisis in the eurozone. In the summer of 2011 it was not only the stability of Middle Eastern regimes but the creditworthiness of Italy and the United States that would be placed in doubt. Little wonder, perhaps, that two acute observers of the contemporary scene should refer to the world in 2011 as being governed not so much by the G20, G8 or G2 but by G-Zero. 8

I

By the spring of 2011 austerity was biting deep into the social fabric of Europe. Spending cuts and tax increases were slashing demand and squeezing economic activity. Across the eurozone, 10 percent of the workforce were unemployed. But unemployment for those between the ages of fifteen and twenty-four was 20 percent. And on the troubled periphery, the numbers were numbing in scale. In Ireland general unemployment reached 15 percent and youth unemployment 30 percent, in Greece 14 percent and 37 percent, respectively. In Spain 20 percent of all adults and 44 percent of young people were unemployed by the summer of 2011. Half a generation had their launch out of education and into working life aborted. Nevertheless, the demand for further austerity was unrelenting. After Ireland and Greece had subordinated themselves to troika programs, on March 23, 2011, Portugal’s prime minster, José Sócrates, resigned after failing to gain support for budget cuts. A week later, on April 2, Spain’s social democratic prime minister, José Luis Rodríguez Zapatero, announced that he would not run for reelection and would prioritize stabilizing Spain’s finances. On April 7 Portugal became the third country to place itself under a troika program. 9

The sense that Europe’s welfare state was being subjected to a relentless program of rollback driven by the demands of bankers and bond markets provoked outrage. Stéphane Hessel, former French resistance fighter and ecological activist, survivor of Buchenwald, Dora and Bergen-Belsen, became an unlikely bestselling author with his well-timed manifesto Indignez-Vous! (Time for Outrage! ). 10 To oppose the demands of global finance Hessel summoned the spirit of resistance martyr Jean Moulin, who died in 1943 at the hands of the Gestapo. Taking up Hessel’s slogan on May 15, 2011, ahead of local elections, a crowd of twenty thousand Spanish protesters occupied the most symbolic square in Madrid, the Puerta del Sol. The indignados would remain there for a month, defying efforts by the police and courts to evict them. 11 Building a tent city, they declared that “we are not goods in the hands of politicians and bankers.” 12 And the M15 movement continued long after their original camp was dispersed. June 19, 2011, witnessed the largest wave of demonstrations in Spain’s tumultuous modern history, bringing perhaps as many as 3 million people—7 percent of the Spanish population—onto the streets. 13 Scaled to the size of the United States, the equivalent demonstration would have involved 19 million protesters. Among the more humorous Spanish chants was one directed at Greece, their partners in austerity: “Hush! The Greeks are sleeping.” In 2010 Greece had been rocked by massive protests. But since the fall, resistance in Greece had ebbed. On May 28, 2011, Athens answered the Spanish challenge and the latest round of cuts demanded by the troika with the occupation of Syntagma Square. A week later, June 5 saw a gigantic rally, with between 200,000 and 300,000 participants in the capital city. Syntagma would be cleared only after violent clashes on June 28–29 pitting revolutionary militants against riot police, many of whom made no secret of their sympathy for Greece’s neofascist Golden Dawn movement.

A resurgent nationalism, defending sovereignty against the impositions of the crisis, would be one of the most powerful political responses to the crisis. This had both left- and right-wing variants. Both were at their most vocal in Greece, where the diktat of the troika awakened memories of occupation, civil war and dictatorship. On the Left it was commonplace in the demonstrations of 2010 and 2011 to associate Germany’s veto over eurozone economic policy with Nazi imperialism. Meanwhile, Greece’s own fascists paraded openly in the streets. 14 The membership of the Golden Dawn party reveled in torch-lit processions, adorned with runic flags and shielded by heavily muscled storm troopers. Golden Dawners harassed and attacked leftists and non-European immigrants, while laying on soup kitchens, reserved, of course, only for hungry Greeks. In a textbook rerun of the 1930s, a comprehensive social and economic crisis provided the setting for a program of national racial community.

The modes of resistance produced by the crisis were significant in their own right. Marches, demonstrations and strikes were combined with encampments, claiming territory. Public spaces manicured and modernized beyond recognition during the boom years were reclaimed for an alternative mode of life. 15 In Greece, defiance of the troika took the form of the nonpayment of taxes and fines. In Spain, with 500,000 families facing eviction and a life crushed under unpayable debts—there is no bankruptcy protection for mortgage debtors under Spanish law—protesters specialized in new forms of nonviolent, direct confrontation. 16 So-called escraches brought flash mobs together, organized via social media, to “get in the faces of politicians,” forcing the unresponsive elite to acknowledge the scale and intensity of the emergency. 17 If markets were entitled to panic, why should citizens be expected to preserve a proper demeanor? Why was it only the “confidence” of investors that mattered? 18

The new Left that began to take shape in response to the eurozone crisis would in due course shake up European politics. 19 In Greece, the coalition of the radical Left, known as Syriza, a combination of antiglobalization movements and breakaway elements of the Communist Party that had first formed ten years earlier, positioned itself under its charismatic young leader, Alexis Tsipras, as the radical alternative to PASOK, as the party willing to lead the Greek people in their struggle against oligarchs at home and the troika in Brussels. 20 In Spain the ranks of the protesters of 2011 included the articulate professor of political sociology and left-wing talk show host Pablo Iglesias, who would go on to be the main mover behind the Podemos party that was founded in 2014. 21 Like Syriza, Podemos activists freely invoked the language of “the people” to bind together a broad-based coalition against the government’s austerity line. 22 Podemos championed the cause of “la gente ” against “la casta ”—the corrupt clique bent on stealing “democracy from the people.” 23

Greek and Spanish politics would never be the same again. The crisis had leaped from the financial to the political sphere. But in the spring of 2011 the protests were held at arm’s length by the incumbent governments. What forced a change in policy was not protest, however passionate and imaginative, but the inescapable realization that extend-and-pretend, the “fix” cobbled together in 2010, simply did not work.

II

Greece’s situation was deteriorating. It was implementing austerity but the debt to GDP burden was rising, not falling. Cutting government expenditure did not have the energizing effect on private business activity that the advocates of expansionary austerity imagined, but rather the reverse. 24 Consumer spending and investment plummeted. As demand collapsed, this led to further job losses and declining tax revenues. By the early summer of 2011 it was clear that Greece would not be able to access capital markets in 2012, as had been assumed. This meant that the Europeans would have to come up with further loans or find some way of reducing Greece’s obligations ahead of the 2013 deadline. The IMF would not continue to disburse money into a program that was not fully funded. One year on from the crisis of the spring of 2010, patience was running out in Berlin too. At a G7 meeting on April 14, after Strauss-Kahn had set out the IMF’s terms, Schäuble weighed in. “We cannot just buy out the private investors with public money,” he admonished. 25 Merkel’s coalition was fragile. The FDP was, frankly, Eurosceptic. The SPD, if it was to vote with Merkel on Europe, demanded that the bondholders must be burned. But the EU Commission and the French government demurred, and Trichet would stop at nothing to keep restructuring off the agenda. When on April 6 the Greeks formally requested a discussion of reprofiling—restructuring the debt not by reducing the amounts owed but by extending the period of payment and the interest owed—Trichet forced them back into line by threatening to cut off the Greek banks. 26

The ECB’s position was not purely negative. What Trichet wanted was for the national governments to take over the task of bond market stabilization that the ECB had undertaken since May 2010. The European Financial Stability Facility agreed among the European governments on May 10, 2010, had begun operating. It was the vehicle for the bailout loans to Ireland and Portugal. But its legal status was fragile. Its funding was on a voluntary and bilateral basis. And it was to be used only in emergencies to buy up new debt issued by states shut out of the capital markets. It was not authorized to do the job that had been offloaded on the ECB, buying bonds in the secondary market to stabilize prices and yields. For Merkel to designate a common European fund for bond market stabilization was political poison because it smacked of debt mutualization, with all the political and legal ramifications that entailed. The Bundesbank might not like the ECB’s bond buying, but it could be justified as routine central bank intervention. To let Trichet carry the can was the lesser of two evils as far as Merkel was concerned.

This was the basic inconsistency in the German position. Berlin was not just the relentless advocate of austerity. It was also the most consistent and clearheaded on restructuring and PSI. But when it came to its necessary concomitants, starting with backstopping the rest of the bond market, Berlin was inconsistent and incoherent. Nor did Berlin show any particular energy in recapitalizing its banks, allowing Hypo Real Estate and the weaker Landesbanken to become millstones around its neck. Bailing in creditors without backstopping the bond market and strengthening the banks was not so much responsible policy as a high-wire act that the ECB, the French and the Americans all regarded with horror. And this is the most charitable interpretation of Berlin’s motivations. The less charitable reading was that Germany was engaged in a strategy of tension, deliberately fostering market uncertainty to bully the rest of the eurozone into submission. 27 Meanwhile, Germany enjoyed the privileges of a safe haven. While the PIIGS groaned under rising yields, Germany’s interest rates were sliding inexorably toward the zero lower bound. The uncertainty in the eurozone was not good for export business. But Germany’s exports to the rest of the world were booming. Labor markets were tightening. It was a long way from the affluence and complacency of Munich or Frankfurt to the turbulent streets of Madrid and Athens. Berlin could afford to wait it out.

It was Trichet and his colleagues at the ECB who found the status quo unacceptable. As a result of months of bond buying, by the spring of 2011 they found themselves as proud owners of 15 percent of Greece’s junk-rated public debt. When further negotiations about the European Stability Mechanism, the permanent replacement for the EFSF, did not provide for the purchasing of bonds in the secondary market, the ECB’s patience ran out. It was time for Frankfurt to draw the line. The public side of the ECB’s new harder stance was interest rate policy. As the eurozone crisis heated up again in April and July 2011, the ECB, in one of the most misguided decisions in the history of monetary policy, raised rates. 28 In the ECB’s defense, it was true that inflation in Germany and other hotspots of the eurozone economy was picking up. The asymmetry between the relative prosperity of Northern Europe and the rest of Europe was all too real. But the ECB’s move was clearly intended as a political signal. The ECB was asserting its independence. It was putting Europe’s governments on notice. It would be up to them to take responsibility for the debt markets. 29 Nor were interest rates the only way to send the message. Without fanfare, indeed, without public announcement of any kind, in mid-March the European Central Bank stopped purchases of eurozone sovereign bonds and introduced differentiated haircuts on repos for lower-rated bonds. 30

It took a few weeks for the markets to register the serious tightening of credit conditions. Then they sold off. The yield spread between the safest and riskiest eurozone bonds surged. The Greek spread reached 1,200 points and this time the fear was different. In 2010 the markets had moved against individual countries, first Greece, then Ireland. Now a wall of money was moving against the eurozone as a whole. One key indicator was American money market funds, key contributors to the cash pools from which European banks sourced their funding, huge sources of liquidity managed by giant asset managers like BlackRock. Whereas in early 2011 they were still providing as much as $600 billion in funding to European banks, from the spring they drastically curtailed their exposure. 31 Over the course of the year they would reduce their commitment to European banks by 45 percent. French banks were particularly hard-hit. Even giants like BNP were not exempt. On Wall Street large bets were now being placed not just on the default of the weakest borrowers—by the spring S&P was reckoning with a 50–70 percent haircut on Greek debt and a 1-in-3 chance of outright disorderly default—increasingly, investors were betting on the collapse of the euro itself. The most aggressive hedge fund managers swung their money first one way then the other, betting against the dollar on the back of the ECB’s interest rate increase and then the other way, taking huge positions against European sovereigns, banks and other vulnerable stock. 32 Big Wall Street names like bond king Bill Gross at PIMCO and John Paulson, the hedge fund hero of 2008, let it be known that they were bearish on Europe. They had always been skeptical about the eurozone, admittedly, but with the ECB and the national governments at odds, the Europeans seemed bent on self-destruction, and there was money to be made on that too.

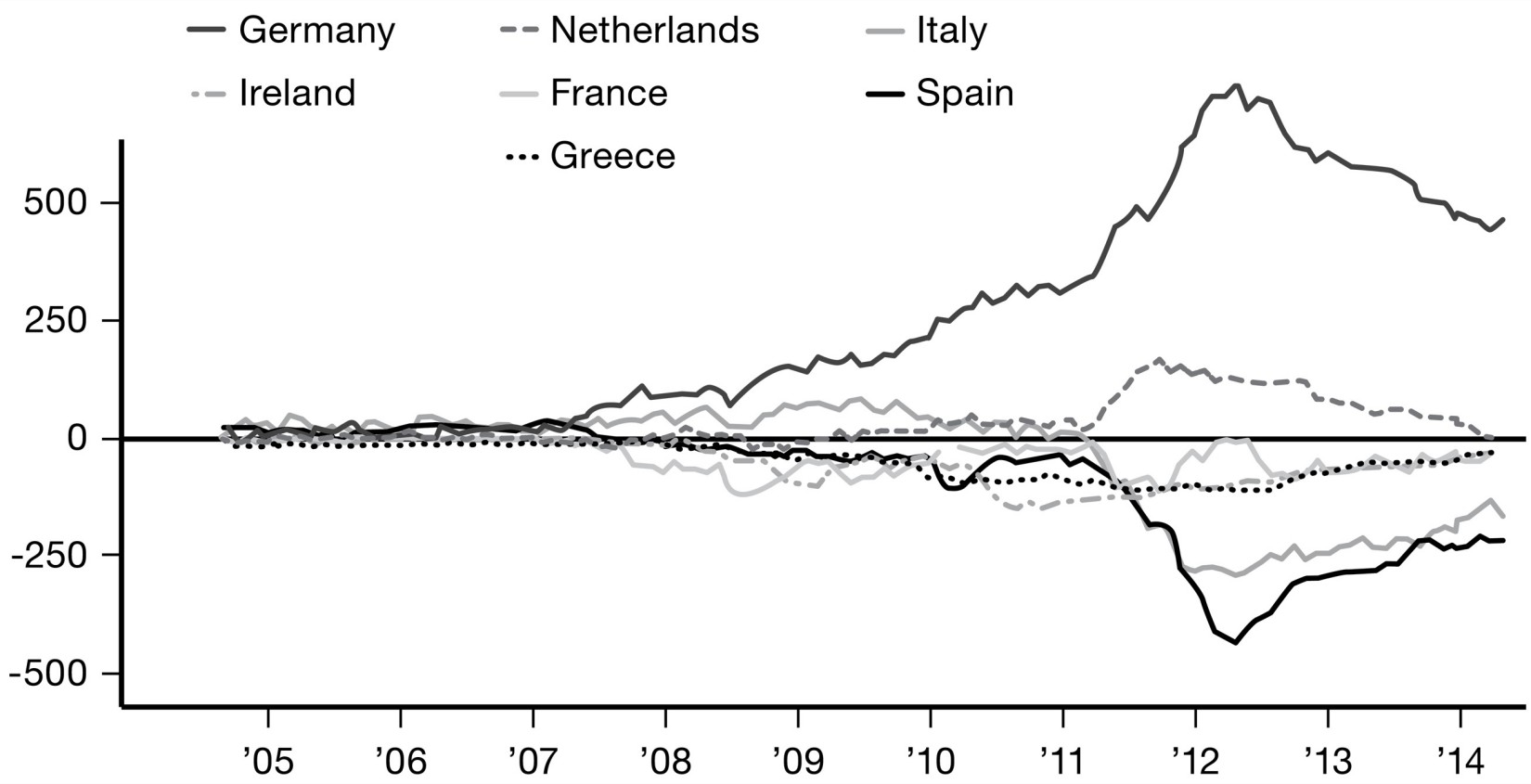

Nor was it only American money that was signaling its lack of confidence. A huge internal movement of funds within the eurozone was afoot. This was registered in a previously obscure but soon to be notorious appendage of the Eurosystem known as the TARGET2 balances. 33 As money flowed out of bank accounts in Greece, Ireland, Spain and Portugal in search of safety, it moved to Germany and elsewhere in the core eurozone. If funding markets had been functioning normally, the stressed peripheral banks would have found replacement funding in interbank markets without troubling their central banks. The recipient banks in the north were, after all, flush with flight money, and their Greek counterparts were willing to offer good rates. But interbank lending in Europe had never recovered from the shocks of 2007 and 2008 and had been dealt a further blow in the panic of April 2010. So instead, peripheral banks drew their funding from their national central banks, which, because they were no longer sovereign issuers of domestic currency, drew their euros from the ECB headquarters in Frankfurt, while at the same time the Bundesbank and other recipients of flight money piled up credits. Suddenly, in the spring of 2011, thanks largely to the journalistic entrepreneurship of the economist professor Hans-Werner Sinn, the German public was alerted to the shocking and quite misleading news that they were secretly providing a huge “credit” to the periphery. 34 Hundreds of billions of euros would be “forfeited” if the currency system collapsed.

This alarmist interpretation of the accounting data should be seen less as a piece of economic analysis than as a symptom of the increasing loss of legitimacy on the part of the euro system. What the TARGET2 balances registered was not a “loan” by Germany to the rest of the system. The TARGET2 balances were the offsetting official counterpart to an enormous movement of private funds into German bank accounts from the eurozone periphery. Some of those moving funds were rich Greek or Spanish businesses. But in large part it was Germany’s own investors bringing their euros home. They were able to do so without risk of currency losses or a massive Deutschmark appreciation, which would have hurt Germany’s exporters, thanks to the monetary union and the ECB’s clearing system. Sinn liked to inflame his readers with dark scenarios in which a breakup of the euro resulted in a loss of Germany’s bookkeeping claims on the ECB. It was a grim and uncertain prospect. But one thing was certain: The funds that anxious investors had already moved to safety in Germany were very unlikely to leave. What Germany was benefiting from was something akin to the exorbitant privilege enjoyed by the United States in the global economy. At times of stress, global money moved into dollars. In the eurozone, money moved to Germany. 35 It was a privilege measured by the yield spread. As the yields on crisis-country bonds soared, those on Bunds eased. It was one of the factors that helped to feed Germany’s prosperity bubble. That a flow of funds into Germany should come to be seen as a burden was symptomatic of the feverish discourse of the crisis.

TARGET2 Balances for Select Eurozone Nations (in billions of euros)

Source: Bruegel, National Central Banks.

III

By May 2011, confidence was so shaky that a secret Eurogroup meeting was hurriedly convened in Luxembourg. Scheduled for Friday, May 6, it was meant to restore unity and coherence. Instead it turned into a PR disaster. When Schäuble insisted that they must start by discussing restructuring and PSI, Trichet stormed out. He wouldn’t countenance such talk. On the other hand, to proceed without him was impractical, as the only thing keeping the Greek banks alive was ECB support. 36 No one fancied the idea of having to restructure them too. When Der Spiegel got wind of the meeting and markets in the United States began to react, the spokesman for Jean-Claude Juncker, the veteran prime minister of Luxembourg and Eurogroup chair, flatly denied that any meeting was taking place. 37 Hours later the same spokesman was forced to admit that the leaders had indeed met. “There was a very good reason to deny that the meeting was taking place,” he told the assembled journalists. “We had Wall Street open at that point in time.” The euro was plunging. Lying was a matter of “self-preservation.” When the Wall Street Journal asked whether such deception might undermine the “market’s confidence in future euro-zone pronouncements,” Juncker’s spokesman retorted that the market already appeared to discount any comments by ECB president Trichet and France’s finance minister, Lagarde. Whatever they said on the subject of Greece’s debt, “nobody seems to believe it.” So what further harm could be done by a convenient lie? Juncker himself had come to similarly stark conclusions: “Monetary policy is a serious issue,” the Eurogroup chair told an audience in April. “We should discuss this in secret, in the Eurogroup. . . . If we indicate possible decisions, we are fueling speculations on the financial markets and we are throwing in misery mainly the people we are trying to safeguard from this. . . . I am for secret, dark debates. . . . I’m ready to be insulted as being insufficiently democratic, but I want to be serious. . . . When it becomes serious, you have to lie.” 38 By May 2011 the effort to defend the indefensible, to uphold extend-and-pretend, had resulted in a complete breakdown of credible and coherent communication about the eurozone’s economic policy. Juncker was unusual only for feeling that he didn’t need to dress it up, which, as far as a tiny bourgeois tax haven like Luxembourg was concerned, might have been true. Projected onto a larger stage of the EU, the implications of Juncker’s “realism” were rather more disconcerting.

With Europe’s credibility draining away, what was needed was a “reset,” a clarifying intervention that would restore credibility and stop the crisis of confidence from widening. That is what Dominique Strauss-Kahn, as head of the IMF, seems to have had in mind when he scheduled meetings, first with Angela Merkel and then with the Eurogroup, for mid-May 2011. Strauss-Kahn “was going to push for a big firewall,” recalled one senior US official. “We were putting a considerable amount of expectation on the outcome of those meetings.” 39 Inside the IMF, a new head of steam of opposition to extend-and-pretend was building. The Fund’s Ireland team had never been satisfied with the inequitable deal forced on Dublin by the ECB and the G7 in November 2010. Ireland’s problems, Ajai Chopra insisted, were not merely Irish in scope, “they are a shared European problem” that required joint European action. 40 What was needed was to beef up the EFSF, giving it more resources and wider authority to intervene. Furthermore, as Ireland showed, Europe’s banks were too big to bail by any but the largest states. So Chopra insisted that if banks could not raise enough capital from private sources, there should be coordinated recapitalization across the EU. 41 Already a year earlier, in March 2010, Strauss-Kahn had challenged the Europeans to establish a jointly funded bank resolution authority. 42 Without that, any steps toward major debt restructuring were dangerous to contemplate.

By May 2011 the IMF had clearly formulated the basic logic of a eurozone fix that went beyond extend-and-pretend, and Strauss-Kahn seems to have been bent on delivering it. But minutes before his departure from JFK on May 14, the managing director of the IMF was hauled off his flight by officers of the NYPD to face charges of sexual assault and unlawful imprisonment. It was a bewildering turn of events. Much of European opinion was in uproar at the spectacle of such a prominent figure being reduced to the indignity of a New York perp walk. Did the presumption of innocence not hold in America? 43 In France those who did not blame the Americans blamed Sarkozy, who was widely suspected of plotting to eliminate Strauss-Kahn as a rival for the presidency. 44

Meanwhile, the hope that the IMF might shake the eurozone out of its paralysis evaporated and the Fund was left without a managing director. The question of succession opened a sore wound. In 2007 the emerging markets had been promised that the next head of the IMF would be one of theirs. Now, faced with the eurozone crisis, it was argued that because the IMF was so deeply engaged in Europe, it was crucial to have a European at the helm. Had Latin Americans, Asians or Africans ever had the temerity to make the analogous case, one can only imagine the reaction. The Europeans didn’t even blink. Their candidate for the job was Christine Lagarde, who had proven both her loyalty and her competence as Sarkozy’s finance minister. She had the backing of Europe, the United States and China. Meanwhile, as the eurozone spiraled toward crisis, the IMF’s push for decisive action was aborted. While Lagarde readied herself for her new role, the helm was taken by John Lipsky, the IMF’s American number two. Lipsky was all for large-scale support actions in the interest of systemic stability. If there were to be private sector involvement, on the other hand, it would have to be voluntary, and modest in scale. The priority of systemic stability and preventing contagion reasserted itself. This was no time for dangerous talk about debt restructuring or bank recapitalization. What mattered was containing the crisis and preventing uncertainty spreading from Europe.

IV

Strauss-Kahn never made it to his discussion with Merkel. But on June 5 the German chancellor headed to Washington. 45 By inclination, Merkel was an Atlanticist. But not since 2003 had relations been so strained. On economic policy Germany and America had been out of step since the crisis began. The storm over QE2 had been embarrassing. And where had Germany been in Libya? What was Berlin’s plan for Europe? The discussions with Obama were intense. Merkel returned home on June 8 with a Presidential Medal of Freedom and a new tune. There would be no more talk of Greek default or Grexit. In exchange for further austerity from Greece, there would be another aid package. Private sector involvement, i.e., debt restructuring, would be part of the bargain, as Germany had wanted from the start. But it would be voluntary. It would be a creditor-led restructuring, with the banks exercising a veto over the manner and scale of the debt write-down. What was still missing from Berlin’s pronouncements was any bold plan for a European bond fund or recapitalization. The net effect, therefore, was to heighten the tension. What the markets heard was that there would be PSI but without an adequate safety net.

On June 29 the battered Greek government pushed the fourth round of austerity through parliament, including privatization, tax increases and pension cuts. It did so in the wake of the violent clearance of Syntagma Square occupation and a two-day general strike. It did so in the face of IMF calculations that suggested that to achieve debt sustainability Greece needed to sell off public assets to the tune of 50 billion euros. Indeed, according to a further IMF assessment released on July 4, even that would not be enough. 46 It would take not only austerity and privatization but a truly heavy bondholder haircut to get Greece to sustainability. The tone of the talks with the International Institute of Finance (IIF), which had begun on June 27, suggested that there was little prospect of that. The banks and other bondholders were making only modest concessions. That suited the ECB, which was desperate that there should be no “default event,” but it stood in jarring contrast to the tens of billions of euros in cuts that Athens was imposing on its citizens. For Greece, the new Merkel-Obama dispensation was revealing itself to be extend-and-pretend in a new guise.

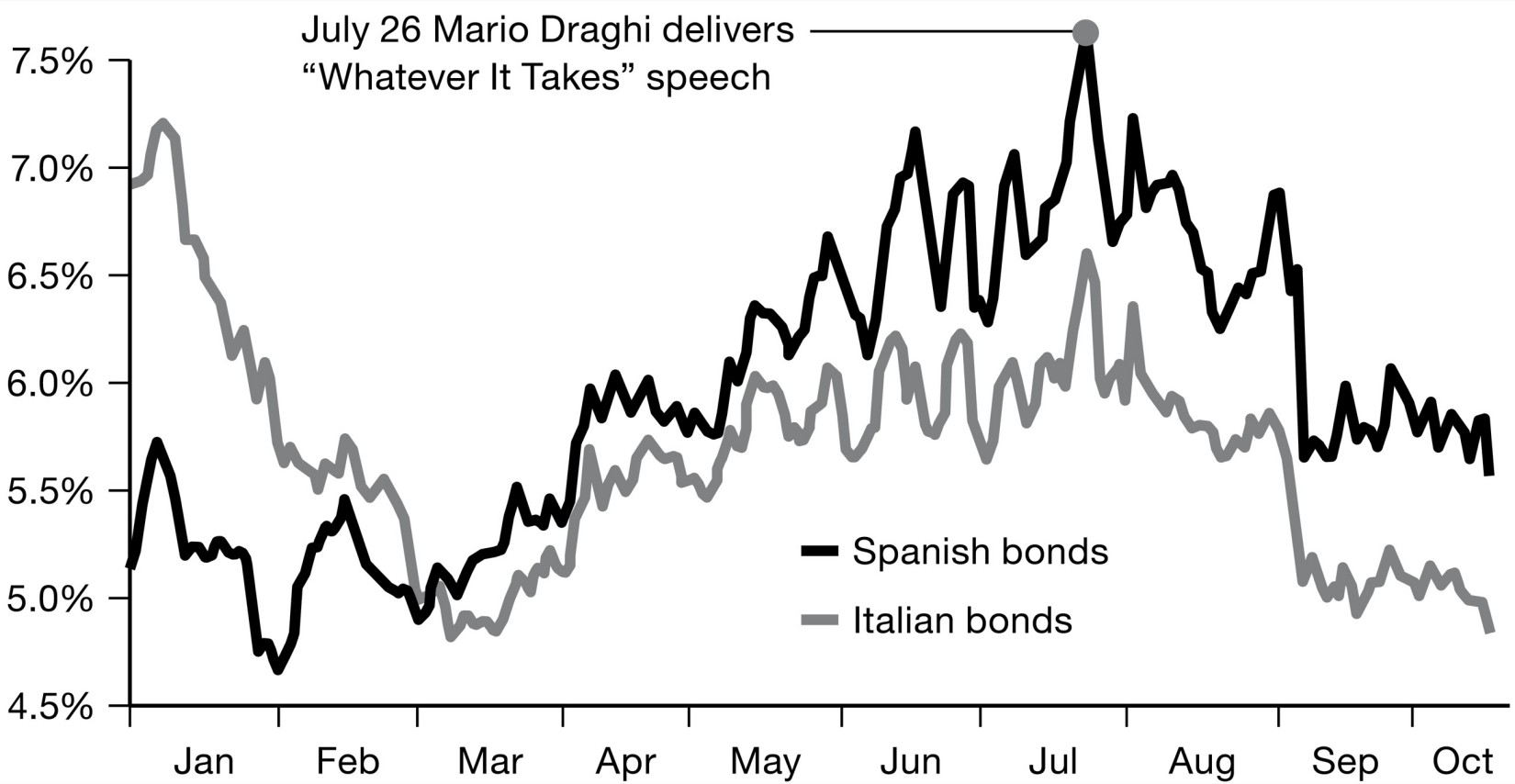

By June, as the S&P ratings agency downgraded Greece to CCC—the lowest score awarded to any sovereign borrower—and spreads surged to 1,300 points, the markets were asking a new question. If the eurozone couldn’t handle Greece, what if it faced more serious trouble? What if it had to deal with a crisis in Spain, or in Italy? Twenty years earlier, in the early 1990s, Italy had been on the rocks. Since then Italy’s debt had stabilized. Rome managed primary surpluses. But its debt was still dangerously high in relation to GDP. And given the size of the Italian economy—the eighth largest in the world by nominal GDP—its debts were enormous: 1.8 trillion euros. Alarmingly, in the last days of June 2011, following the decision to implement PSI in Greece, 100 billion euros of Italian debt had been sold off. European banks were pulling back, with French banks leading the way. The share of foreign holding of Italian debt fell from 50 to 45 percent in a matter of weeks. 47 That was enough to send Italy’s borrowing costs up from 4.25 to 5.54 percent between June and August of 2011. That might not seem like a large number. But given Italy’s huge refinancing needs, it spelled disaster. Between the second half of 2011 and the end of 2014 Rome calculated that it would need to borrow 813 billion euros in refinancing and new loans. A 25 percent increase in the cost of servicing such a huge volume of debt was a serious matter indeed. If a run began on Italy, it might well be game over for the eurozone.

Contrary to North European prejudice, the Italian political class was by no means oblivious to the seriousness of the situation. Italian economists, notably the “Bocconi boys,” named after the preeminent business school in Milan, had contributed as much as anyone to the new consensus of spending cuts and “expansionary austerity.” 48 Faced with the emergency of 2008–2010, Italy had permitted itself virtually no stimulus. The question was whether Rome had the will and capacity to respond to the new panic in the bond market. And, in particular, how Prime Minister Berlusconi would react.

Berlusconi was a figure wreathed in scandal. 49 He had faced allegations for crimes including racketeering, large-scale tax evasion and corruption. But on February 15, 2011, in the most embarrassing charge of all, he had been indicted for paying for sex with a minor and abuse of office in his efforts to cover up his liaison with an exotic dancer and call girl known as “Ruby the Heartstealer.” Rather than resigning, Berlusconi clung to his office. On April 6, 2011, as financial markets watched anxiously, Italy’s prime minister went on trial. The proceedings were immediately adjourned, but hearings would resume at the end of May. Meanwhile, a dark cloud of uncertainty and disrepute hung over the Italian government. Further doubts were raised at the end of May, when Berlusconi’s political alliance between Forza Italia and the Lega Nord lost control of Milan, his personal fiefdom. 50 Even at the best of times, Berlusconi’s instincts were those of a crowd pleaser. Now that he was fighting for his political life, could he be counted on to push through the kind of austerity that his finance minister, Giulio Tremonti, was demanding?

Over the weekend of July 9–10 Merkel intervened personally with Berlusconi to urge on him the seriousness of the situation. Europe’s future hung on Italy. But was it Italy, or was it, in fact, Germany that was the weak link? To many in Europe it was unclear whether Merkel herself was truly committed to holding the euro together. Ugly whispers began to circulate that Germany’s veteran chancellor, Helmut Kohl, father of the euro and German reunification, was questioning whether his European legacy was safe in Merkel’s hands. “This girl [Merkel] is destroying my Europe,” Kohl was reported to have told one journalist. 51 Only reluctantly were Merkel and Schäuble persuaded to defer summer travel plans and call an emergency meeting of the European Council on July 21 to discuss eurozone stabilization. The issues were predictable: fiscal adjustment and austerity, PSI, restructuring and debt sustainability, ECB bond buying. Only Europe-wide bank recapitalization, the final element in a coherent crisis-containment strategy, was not yet on the table. But what was Berlin’s game? Were Merkel and Schäuble engaged in truly hair-raising brinksmanship? Or, cocooned in their relative prosperity, did the German political class simply not understand the pressures the rest of the eurozone was under?

On July 14, 2011, in response to market pressure, the Italian parliament adopted a severe 70 billion euro austerity program, on a par with Germany’s 2010 effort. 52 But doubts remained as long as Berlusconi was at the helm. And the issue of PSI in Greece remained unresolved. Trichet was sticking to his guns. If there was anything approaching full-blown restructuring of Greek debt, the ECB would disallow Greek bonds as eligible collateral. Panic was again spreading through eurozone debt markets. What had originally been a problem of small fry, like Greece and Ireland, was rapidly becoming a comprehensive crisis of Southern Europe, including large economies like Spain and Italy. Whereas in 2007 eurozone bond investors had regarded Greek debt as equivalent to that offered by Germany, by September 2011 the CDS spreads on Italy and Spain were higher than those of Egypt in the throes of revolution. 53 The three countries in the world judged most likely to default were all in the eurozone—Greece, Ireland and Portugal—well ahead of Belarus, Venezuela and Pakistan. 54 The revolutionary mood seemed to have jumped the Mediterranean. The violent scenes in Athens fed fantasies of social disorder spreading across Europe. Supposedly serious financial analysts were talking of “hyperinflation, military coups and possible civil war.” 55 But it wasn’t any longer a matter of individual predatory hedge funds, or one or two overexcited analysts talking the euro down; commercial banks and pension funds from across Europe and the United States were pulling tens of billions of euros out of Italy and the program countries. 56 Once eurozone sovereigns lost their standing as issuers of safe assets, institutional investors had no option but to reallocate their portfolios. And that affected the European banks too. In the summer of 2011 wholesale funding was drying up. 57

With only days to go until the July 21 summit, the possibility dawned on Paris that Merkel might be willing to let the upcoming talks fail. 58 The debt reduction so far agreed with the bank lobbyists was too low to satisfy Berlin. The resources and mandate for the EFSF were insufficient to reassure the French, calm the markets or persuade Trichet to resume bond buying. If the talks failed, no one would be safe, including France. To break the deadlock Sarkozy realized that he would have to deal with Merkel one-on-one. The French president arrived in Berlin on July 20 at 5:30 p.m. and immediately hit a roadblock over the EFSF. It soon became clear that Berlin and Paris could not settle the matter without involving Trichet. He was summoned from Frankfurt, arriving on the last plane into Berlin at 10:00 p.m. The deal had to be done not between Germany and France but between Germany, France and the ECB. In the early hours of July 21 Sarkozy and Merkel took turns on a single cell phone to read out to Van Rompuy, the president of the European Council, the terms of their agreement. That afternoon in Brussels the package was formally presented to and voted on by the other governments.

Greece would receive an additional 109 billion euros, meeting its financing needs through 2014 and enabling the IMF to continue as part of the troika. The interest it paid on its loans would be lowered to 3.5 percent. Maturities would be extended and, through a menu of PSI options, Greece’s creditors would make a contribution, though the precise amount remained to be determined. The ECB would be indemnified for any losses it suffered. If the Greek banks suffered irreparable damage they would be recapitalized out of troika funds. 59 Most important, the governments stated emphatically that PSI applied only to Greece. It was the only insolvent eurozone sovereign. All others would honor their obligations without fail. To contain contagion the EFSF would be beefed up and at the behest of the ECB it would be empowered to enter the secondary market and to establish credit lines for nonprogram countries, such as Spain and Italy. The EFSF would no longer act only as an ultima ratio, as Merkel had insisted since March 2010, but as a preemptive agency, helping to stabilize markets to forestall any threat arising. These, finally, were the elements of a workable solution—buy-in by the Greeks, debt restructuring, further loans, cooperation with the ECB and backstopping by a newly empowered EFSF. There was even partial recognition of the need for bank recapitalization. The general structure was fine. But did the sums add up? And who was to pay?

One neuralgic point was the scale of PSI. The initial figure that had emerged from the polite negotiations with the IIF was only 20 percent. The bankers were not permitted in the intergovernmental meetings on July 21. But they gathered in the corridors outside. When the governments let it be known that 20 percent was insufficient, the IIF offered 21 percent. With this symbolic concession there was general satisfaction that a deal had been done. No one did the math. It was a matter of gestures, not arithmetic. When the IMF’s representative queried Greece’s sustainability under the assumption of such a modest restructuring, the meeting was treated to a “furious denunciation” by Charles Dallara of the IIF. 60 The indignation too was for show. In private Dallara was only too happy to boast of the astonishingly generous deal that his lobbying had secured for his clients, the big banks. 61

The result of this compromise was that Greece would pay the reputational price for having restructured its debts, but it would gain precious little financial relief. It would be left carrying a debt burden of 143 percent of GDP, which was clearly unsustainable. As one Goldman Sachs analyst commented: “This tendency to ‘under-size’ otherwise good policy initiatives has been a recurrent feature of European policies.” A member of the UBS economics team was less polite: “This is fiddling around at the margins. . . . The debt needs to halve.” As to the new support facilities provided by the EFSF, Willem Buiter, chief economist at Citigroup, told Bloomberg Television, “The European Financial Stability Facility has gone from being a single-barreled gun to a Gatling gun, but with the same amount of ammo. . . . It needs to be increased in size urgently.” 62 If Italy went critical, the EFSF would need not 200–400 billion but 1–2 trillion euros. Otherwise, only the ECB, with its bottomless supply of euros, could backstop the system.

In the meantime, investors were on edge. At the end of July it emerged that Deutsche Bank had cut its holdings of Italian debt by 88 percent since the beginning of the year. 63 For Italians in Berlusconi’s camp it was a clear case of blackmail. In the circles around Finance Minister Tremonti there was talk of a stab in the back. 64 Earlier in the year Rome had had the temerity to suggest that any joint European bailout fund ought to be funded in proportion not to GDP but to the size of bank claims that were being rescued. Not surprisingly, this was not a popular idea in Berlin. Tremonti was convinced that the precipitate sales by Deutsche were a message from Merkel and Schäuble. Whatever the truth of the matter, the suspicion was symptomatic. Trust was breaking down.

V

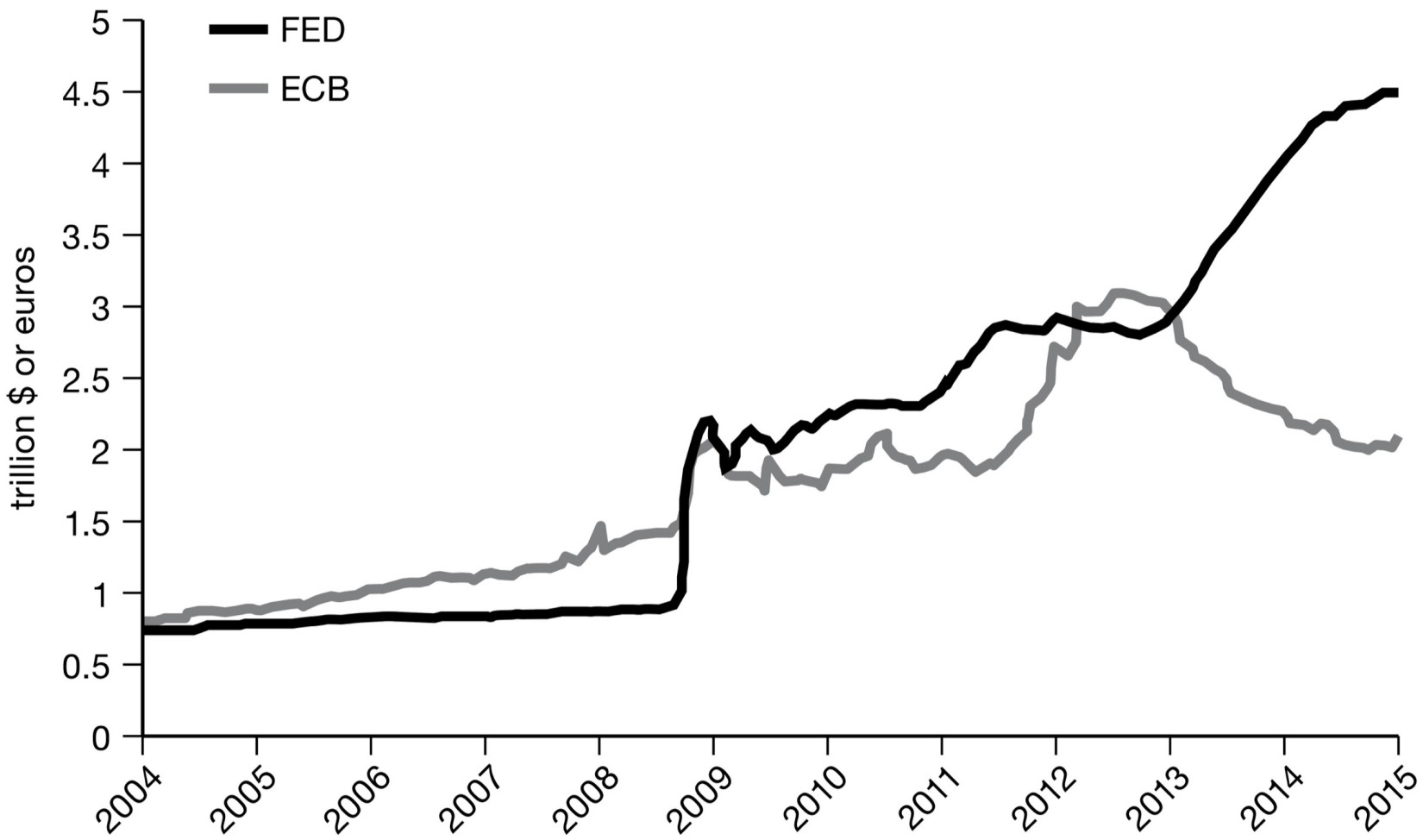

If money was fleeing out of Europe, where was it to go? The answer since the onset of the financial crisis had been, paradoxically, the United States. As US subprime went bad, there had not been the panicked dollar sell-off that many had feared. Instead, investors shifted into US Treasurys, the very top of the global monetary pyramid. In 2008 the dollar surged and US interest rates fell. Successive waves of QE reversed that trend. The dollar slid against its major trading partners. This imposed losses on investors and made US bonds marginally less attractive. By the summer of 2011, however, something far more ominous was on the horizon.

At the start of the year, as the new Republican majority in Congress flexed its muscles, the effort to craft a bipartisan, long-term approach to fiscal consolidation broke down. 65 For want of a budget, in April 2011 the US federal government already came close to a shutdown. On May 16 the permissible ceiling of federal debt was reached, at $14.3 trillion. With tax revenue covering only 60 percent of current spending, Washington had hit the limit of its legal right to borrow. The Treasury was forced to adopt “extraordinary measures,” including borrowing from government cash reserves and selling assets from the civil service retirement fund. 66 This would see the Treasury through until August 2. After that, the US federal government would face a choice between paying salaries or paying its creditors. America was sliding toward something even worse than concerted austerity, a chaotic shutdown risking default on its obligations to both domestic and foreign creditors.

In late July 2011, as Sarkozy, Merkel and Trichet diced with the future of the eurozone, the United States was perilously close to the edge. There was no longer any disagreement in Washington about the need for urgent fiscal consolidation. 67 But there was a huge divide between Democrats insisting on a balanced approach to deficit reduction, involving tax increases as well as entitlement cuts, and Republicans focused exclusively on spending reductions. The Speaker of the House, John Boehner, was looking to assert his control over the Tea Party faction by striking a deal with the White House to achieve deficit cuts of $4 trillion over ten years. But on July 22 the talks between Boehner and the Obama administration broke down over Republican demands for slashing reductions in medical spending and the White House insistence on a $1.2 trillion increase in taxes. 68 Journalists began compiling calendars as to which bills due in August the American government should pay first. Constitutional specialists were debating the pros and cons of executive prerogative, or coining trillion-dollar platinum coins with which to repay the national debt. 69 If Greece was a problem, and Italy was too big to fail, there was simply no reckoning what a US default might do. In August alone, the Treasury had to roll over almost $500 billion in debt. 70 With the eurozone wobbling, the American money market funds that were pulling out of European bank bonds continued to shift into US Treasurys. But appearances were deceptive. Investor demand for US government debt held up, but above all in lower-risk, short maturities. The average maturity of US Treasurys held by the MMFs declined from ninety-five days in January 2010 to only seventy days at the end of July 2011. 71 Meanwhile, financial engineers began to contemplate the need for something no one had contemplated before—credit default swaps against US Treasurys. 72

Prior to 2008 the market for US Treasury CDS had not existed. What would have been the point of insuring the risk-free asset class on which the entire global financial system rested? In the wildly improbable event of a US default, the general destabilization would be such that it was unclear whether any private financial entity would still be in a position to act as a reliable counterparty. Who would be left standing to pay out on insurance against the end of the world? Nevertheless, having first come into existence during the turmoil of 2008, when it seemed that Fannie Mae and Freddie Mac might fail, in the course of 2011 the niche market for CDS on US Treasurys sprang back into life. In the last days of July just over a thousand contracts were outstanding, with spreads running to 82 basis points. It was a fraction of what investors in Greek debt paid, but it was astonishing that the market existed at all.

On July 31, 2011, Washington pulled back from the abyss. A budget compromise was reached that would impose automatic austerity if the two warring parties could not agree on cuts by the end of the year. Reluctantly, sufficient Tea Party radicals were won over to the Republican leadership’s position for the deal to go through. It took heavy lobbying and hours of alarmist lectures by credit-rating experts and former officials from the Bush administration to convince the Republican insurgents of the dramatic consequences of a default. But the damage was done. As Mitch McConnell, the Republicans’ leader in the Senate, blithely informed the media: “I think some of our members may have thought the default issue was a hostage you might take a chance at shooting. Most of us didn’t think that. What we did learn is this—it’s a hostage worth ransoming.” 73 As Jason Chaffetz, one of the hard-line Tea Party newcomers, remarked, the threat had been real. “We weren’t kidding around. . . . We would have taken it down.” 74

On August 3 China’s Dagong ratings agency was the first to draw the obvious conclusion. It downgraded the United States from A+ to A. As Dagong remarked: “[A]t this crucial juncture, neither the Democratic Party nor Republican Party has shown any consideration for the general interest in order to argue for their own partisan interest; they had a hard time making the correct choice in a timely manner leaving the world in terror, which highlights the negative role of the US political system on an economic basis.” 75 The US political system, the Chinese analysts concluded, “cannot resolve the fundamental influence of low economic growth, high deficit and increasingly higher debt to the debt service capability through increasing real wealth creation, with the declining national solvency irreversible. It is natural that QE3 monetary policy will be enabled for the next step, which will throw the world economy into an overall crisis; the status of [the] US dollar will be essentially shaken in this process.” This was the judgment of the G20 at Seoul turned into the language of credit rating. The year ended with a big sell-off of US government debt by Beijing. But there was no rout. The long buildup of Chinese claims on the US taxpayer had ended. But the portfolio stabilized at between $1.2 trillion and $1.3 trillion.

Criticism from China was only to be expected. More surprising was the fallout at home. On August 5 the unthinkable happened. One of America’s own ratings agencies, Standard & Poor’s, downgraded the United States from AAA to AA+. S&P cited the “political brinkmanship of recent months” and the mounting evidence that “America’s governance and policymaking” was “becoming less stable, less effective, and less predictable.” 76 It also pointed to the supposedly unsustainable level of US debt and the speed of its accumulation, which would take it well over 90 percent of GDP by 2021—the notorious Reinhart and Rogoff threshold. But when the US Treasury was handed the explanation for S&P’s decision, it became clear that the ratings agency had committed an elementary mistake. By applying the figures for debt growth to the wrong benchmark scenario, it had wildly overstated the deficit to be expected over the next ten years. Even more surprisingly, when this error was pointed out, S&P did not retreat. It left the downgrade in place as well as the explanatory text—minus the modeling error. This led the Treasury to fire off an official denunciation. “S&P still chose to proceed with their flawed judgment by simply changing their principal rationale for their credit rating decision from an economic one to a political one. . . . The magnitude of this mistake—and the haste with which S&P changed its principal rationale for action . . . raise fundamental questions about the credibility and integrity of S&P’s ratings action.” 77 No one doubted the weakness of the US political system. But S&P had delivered just one more demonstration of how broken the ratings agencies were. It was their AAA certifications, handed out to hundreds of billions of subprime MBS, that had helped to precipitate the crisis in 2008. It was their serial downgrades that were setting the pace of the crisis in the eurozone. But it turned out that they could not even get their sums right on the US budget.

VI

Trillions of dollars of debt were losing their status as safe assets. The US Treasury was accused by the German finance minister of interventionist tendencies akin to communism. NATO was squabbling over Libya. The loose monetary policy of the Federal Reserve was blamed for fomenting revolt in the Middle East. The EU was locked into a self-deceptive nonsolution to the Greek debt crisis, and when it was not engaged in extend-and-pretend it was openly and unabashedly lying. Both Italy’s prime minister and the managing director of the IMF were up on sex charges. Washington was willfully toying with bankruptcy. The ratings agencies could not do their arithmetic. Millions of people were in the streets, protesting, demanding a “rupture,” unable or unwilling to pay debts they had contracted or that had been contracted in their name.

Over the weekend of August 6–7, as the world digested the downgrade of America’s sovereign debt, heads of government, central bankers and Treasury officials interrupted their summer vacations for a frantic round of telephone conferences. But all that emerged were lame communiqués, which did nothing to inspire confidence. On Monday, August 8, rocked by bad news from both sides of the Atlantic, stock markets sold off sharply. President Obama was left to remark: “We now live in a global economy where everything is interconnected, and that means that when you have problems in Europe and in Spain and in Italy and in Greece, those problems wash over into our shores.” 78

In the general crisis of legitimacy in 2010–2011 there was no Archimedean point. There was no place to stand above the fray. Bringing this home was the point of the protesters “getting in the face” of government officials in Spain and Italy. They wanted to break through the invincible authority and distance that separated decision makers from those their decisions impinged upon, to force them to come face-to-face with a different reality. And over the summer of 2011 a small band of US activists determined to do the same at the hub of the world financial economy in New York.

On August 19, 2011, representatives of the New York Stock Exchange met with agents of the FBI for an unusual conference. 79 Trawling the Internet for suspicious activity, the FBI had got wind of an “anarchist” network dubbed “Occupy Wall Street.” Its aim was to spread the protest movement that had gained such scale in Europe to the United States. The occupation of Zuccotti Park right next to Wall Street was scheduled for September 17. The US media at first ignored the story. The first to cover it were Agence France-Presse and the Guardian . 80 But within weeks the tiny encampment that lodged itself within hailing distance of Wall Street would become headline news around the world. 81

Given the scale of the social media storm it unleashed, it is important to put Occupy Wall Street in perspective. It was tiny compared with the gigantic antiausterity mobilizations in Europe. The global Occupy demonstrations that took place on October 15, 2011, attracted perhaps as many as a million demonstrators in Spain, 200,000 to 400,000 in Rome, tens of thousands in Portugal. In New York between 35,000 and 50,000 protesters marched. But the New York occupation had a symbolic significance far in excess of its modest scale. It articulated radical opposition at the very heart of US capitalism. Imitation camps sprang up across the United States, in Philadelphia, Oakland, Boston, Seattle, Atlanta, L.A., Denver, Tucson, New Orleans, Salt Lake City and many other cities. Further afield there were notable solidarity camps in London, Seoul, Rome, Manila, Berlin, Mumbai, Amsterdam, Paris and Hong Kong. Estimates vary, but protesters in at least nine hundred cities around the world staged sympathy demonstrations. 82 Across the United States, wherever they sprouted, the Occupy camps could expect the watchful presence of the FBI and even US counterterrorism authorities. But despite their tiny size and ramshackle appearance, the obvious and unsettling fact was that the anger of the radical minority was shared by a wide swath of US public opinion.

In October 2011 a poll conducted for the New York Times and CBS News found that almost half those questioned felt that the FBI’s “anarchist camp” reflected the views of most Americans. 83 Two-thirds thought wealth should be distributed more evenly—nine out of ten Democrats, two thirds of Independents and even one third of Republicans agreeing with that sentiment. But only 11 percent of Americans trusted their government to do the right thing, 84 percent disapproved of the Congress that had threatened to bring the US federal government to its knees and 74 percent thought their country was on the wrong track. Since January 2009 the Obama administration had been straining every muscle to put the lid on popular discontent. Rather than seeking to mobilize the indignation simmering in American society, it had found one technocratic fix after another. Two years later the result was a spectacular delegitimization from both the Left and the Right.

Chapter 17

DOOM LOOP

O n September 1, 2011, Pedro Passos Coelho, Portugal’s new prime minister, made his first visit to Berlin. His host, Chancellor Merkel, began the joint press conference by announcing how pleased she was to hear that the troika had just submitted its first report on Portugal’s structural adjustment program and had declared itself satisfied with the progress being made. She was delighted also to hear that Coelho saw no obstacle to incorporating a German-style debt brake into Portugal’s constitution. Then, in the question-and-answer session that followed, it seemed that Chancellor Merkel let the cat out of the bag. Asked about the question of parliamentary control over the European Financial Stability Facility, recently mandated by the German constitutional court, Merkel deadpanned: “We do live in a democracy and we are pleased about that. It is a parliamentary democracy. That means that the budget is a key prerogative of parliament. Thus we will find ways to organize parliamentary codetermination in such a way that it is nevertheless market conforming, so that the appropriate signals appear in the markets. I hear from our budget specialists that they are conscious of this responsibility.” 1

Market-conforming codetermination—was this what European democracy had been reduced to by the autumn of 2011? Was this the hidden agenda of the troika programs, imposed not only on the parliaments of Greece, Ireland and Portugal but on the Bundestag as well—to make them market conforming? For many who joined the protests of 2011, Merkel’s words confirmed their jaundiced view of the EU as little more than a container for the rule of the markets, or that new buzzword of the crisis, “neoliberalism.” 2 Merkel did little to clarify the situation. On September 22, a few days ahead of the IMF meeting in Washington, she welcomed the first German pope, Benedict XVI, to the chancellery. Quizzed by curious journalists, Merkel volunteered that the European crisis had been at the heart of their conversation: “We spoke about the financial markets and the fact that politicians should have the power to make policy for the people, and not be driven by the markets. . . . This is a very, very big task in today’s time of globalization.” 3

In their flailing generality, these statements are symptomatic of the depth of the crisis by the autumn of 2011. In the space of barely three weeks, the German chancellor managed to tell the press that politicians should be responsible to markets and to tell the pope that politicians should make policy for “the people” regardless of those markets. Was it a contradiction? Or was she implying some kind of synthesis? If so, was it a matter of finding the market-conforming mode of expression that would allow politicians to slyly exert their power or, more ominously, a matter of hammering democracy into such conformity that no market ever need fear the policy parliament might make? Did anyone in Berlin know? No surprise that Gregor Gysi, the sharp-tongued spokesman of Die Linke, should lash Merkel’s handling of the eurozone crisis as an engine of chaos and confusion. 4

The very least one can deduce is that the optimistic dogma under which democracy and markets were seen as natural and necessary complements—the mantra of the aftermath of the cold war—was dead. 5 In its place the crisis had put a more realistic awareness of the potential tension between the two. But this generalization too has its risks, particularly when it is assumed that it is financial markets, not politics, that force the tension. Certainly in the course of the eurozone crisis that had not been the case. The pressure the more fragile members of the eurozone were under depended not on some inescapable clash of peoples and markets, or global capitalism and democracy. 6 It was dictated, first and foremost, by the willingness, or not, of the ECB to buy bonds. In the markets many banks and traders were not just crying out for the EU to undertake a stabilization effort but betting billions that it ultimately would. What delayed the stabilization and escalated the conflict between democracy and markets to an extraordinary pitch was the struggle among Germany, France and the ECB over the future governance of the eurozone, a question in which politics and economics were inseparably intertwined. Ironically, the result, as in 2010, was to escalate the crisis to the point that European affairs could no longer be safely left to the Europeans.

I

The compromise of July 21 on a new Greek aid package was supposed to be flanked by a new round of bond buying by the ECB. Ireland and Portugal, at least, were judged to be making sufficient progress under their IMF-supervised programs. So on August 4, 2011, the ECB let it be known that it was once again in the market for their bonds. Prices and yields promptly stabilized. This was the cheery backdrop to Coelho’s visit to Berlin. But as far as Italy and Spain were concerned, Trichet did not want to let them off the hook so easily. The ECB needed further proof of conformity. To make the point, on August 5 Trichet dispatched a confidential memo to prime ministers Zapatero and Berlusconi, spelling out what would be necessary for the protection of the ECB’s bond purchases to be extended to them. 7 In the case of Italy, weight was added to the missive by the signature of Mario Draghi, head of the Italian central bank and Trichet’s anointed successor at the ECB.

Neither Spain nor Italy had applied for a troika program, but that did not stop the ECB from demanding huge cuts to government spending and increased taxation. In the Italian case, Trichet and Draghi called for the privatization of local public services, a proposal that had recently been decisively rejected in a nationwide referendum. 8 The ECB also called for dramatic changes to labor market policy, infringing on rights of Italian and Spanish trade unions. Such changes were necessary, the ECB insisted, to cut unemployment and increase growth. It was a blatant attempt to shift the balance of social and political power by means of monetary policy, poorly disguised by the ECB’s proviso that care should be taken to ensure that the social safety net remained intact. In case these unpopular measures encountered opposition, Trichet and Draghi suggested that the Italian government should invoke the decree powers of Article 77 of the Italian constitution, which allowed executive action “in cases of extraordinary need and urgency.” Originally designed to counter the specter of Communist insurrection during the cold war, Article 77 was a legal fig leaf that had been repeatedly invoked since the 1970s to cover “emergency measures.” 9 Its overuse had been criticized by the Italian courts. If Berlusconi was worried about the legality of these proceedings, Trichet and Draghi advised that he should apply retrospectively for parliamentary sanction. Perhaps not surprisingly, legally minded members of Berlusconi’s cabinet wondered whether it was their malodorous prime minister or Draghi and Trichet who posed the greater risk to the rule of law.

The Spanish government chose to keep the ECB’s letter secret. If it was to be humiliated it preferred not to have the fact made public. As a sign of their compliance, Spain’s two largest political parties agreed to amend the Spanish constitution, unchanged in thirty-three years, to provide for a balanced budget amendment. 10 By contrast, Berlusconi accepted Trichet’s terms but under public protest. He would later say that the ECB’s instructions “made us look like an occupied government.” 11 But rather than embarrassing the ECB, the expostulation from Rome served only to enhance Trichet’s reputation as a hard-liner, which, in an ironic twist, freed him to act. On August 7 the ECB began buying Italian and Spanish bonds under the Securities Markets Programme (SMP). 12

This was enough to calm the markets and stave off the immediate risk of a disaster. But Berlusconi’s government was evasive about the full scale of the austerity measures it was willing to adopt. The Italian economy was perched on the edge of a severe recession. Markets remained jumpy. And as everyone realized, things were going to get worse before they got better. The compromise on Greece hammered out on the weekend of July 20–21 had been inadequate from the start. Rather than achieving sustainability, Greece’s consolidation program was falling consistently behind schedule. To escape insolvency Greece needed a haircut far larger than that squeezed out of the bankers over the summer: not 21 percent but something closer to 50 percent. If this was not to cause panic, it would need to be framed by a solid Franco-German agreement on the future governance of the eurozone. France was truly the last line of defense. If the crisis spread by way of Rome to Paris, the game would be up. Ominously, in the fall of 2011, as the ECB intervened to prop up Italian public debt, the spread of the ten-year French bonds relative to bunds nudged upward to 89 basis points. 13 In reaction, Merkel and Sarkozy tightened their alliance. What Sarkozy desperately needed was a wall of money. With the ECB pursuing a strategy of tension, the only way to really calm markets would be to expand the EFSF or to agree to a wholesale mutualization of eurozone public debt. It was Berlin’s agonizingly slow acceptance of these basic facts that set the pace of the crisis.

On September 29 the Bundestag finally voted on the puny expansion of the EFSF bond market stabilization fund agreed on July 21. It was widely seen as a decisive vote for the future of Merkel’s coalition. 14 Though the EFSF was supported by the majority of the Bundestag, on the German right wing the bond buying of the ECB had triggered a furious reaction. At the crucial ECB board meeting in August, Merkel’s hard-line new appointee as head of the German Bundesbank, Jens Weidmann, once a star pupil of Axel Weber and Merkel’s personal economic adviser, not only voted against bond buying but made his opposition public. 15 On September 9 Jürgen Stark, the German member of the ECB board and the bank’s chief economist—the man widely thought to be behind the ECB’s interest rate hikes earlier in the year—resigned in protest. To stop the momentum of the conservative rebellion Merkel needed to win the EFSF vote in the Bundestag, not with the votes of the pro-European SPD opposition but on the basis of her own Kanzlermehrheit —with the votes of her coalition partners. In the event, on September 29 Merkel got the votes, but by a painfully narrow margin. Out of the 330 members of the government coalition, only 315 voted for the motion, 4 more than the 311 needed. Merkel was on top, but she had little room for maneuver.

In any case, as soon as the Bundestag had voted it was clear that it had been overtaken by events. As everyone in the markets realized, the EFSF fund that had been agreed over the summer was too small. The Bundestag vote on September 29 was simply the occasion to start talking about how the fund might be leveraged, something that had been explicitly ruled out by Schäuble ahead of the vote. 16 Unless the markets suddenly calmed, Merkel’s government would soon be rolling the parliamentary dice again.

II

In the summer it had finally been acknowledged that any Greek debt restructuring would require a full-scale bailout of Greece’s own banks. They held so much Greek public debt that their balance sheets would not survive the debt write-down. What the European governments were still struggling to accept was that the problem was far wider than that. The politics of extend-and-pretend might have the benefit of deflecting attention from the creditor banks to the bankrupt government borrowers. It was the citizens of the troika-supervised countries who paid the price. But it also allowed European policy makers to avoid getting to grips with the underlying problems of financial stability. The assumption, presumably, was that given time the banks would take care of themselves. But despite the fairy-tale numbers produced by the European stress tests, it was clear that this was wishful thinking. In fact, Europe’s banks were sliding back toward the cliff edge in the fall of 2011. They were struggling to cope with pressure from six directions at once. The legacy losses from 2007–2008 were still on their books. Their holdings of European sovereign debt were increasingly impaired. The troubles of the eurozone economy were bad for new business. The new capital and liquidity requirements of Basel III required painful balance sheet adjustment. In their most profitable niche markets in the United States, Europe and Asia, the European banks faced fierce competition from the resurgent American and Asian banks. And in light of all this, wholesale money markets were increasingly leery about offering funding. A slow contraction of balance sheets was one thing. If funding markets shut down, Europe would face a repeat of 2008. Given that acute threat it was not without risk to openly address the long-term issues of the sector. But if the problem of recapitalization was not squarely faced, how would the banks ever be made safe?

In August 2011, as she established herself as managing director of the IMF, Christine Lagarde took up the baton that Strauss-Kahn had dropped when he was carted off to Rikers Island jail. Already in 2009 IMF analysts had highlighted the inadequacy of European bank recapitalization. 17 Now, two years later, in light of the escalation of the eurozone sovereign debt crisis, the IMF estimated that the minimum the European banks needed was $267 billion in new capital. 18 It was a daunting challenge, but without it, all other crisis-fighting measures on the side of fiscal and monetary policy would lack a solid foundation. European political obfuscations were obscuring the basic lesson of 2008: Questions of macroeconomic policy and systemic stability could not be hygienically separated from the workings of megabanks, now more politely known as systemically important financial institutions.

The banks, of course, defended what they took to be their own interests. Never one to shrink from alarmism where bank regulations were concerned, the Institute of International Finance estimated that Basel III plus national regulations would force banks worldwide to raise their capital by $1.3 trillion by 2015. 19 It was a huge ask and many banks might simply prefer to shrink their balance sheets, flattening the fragile recovery. At the meeting of the Financial Stability Board on September 23 in Washington, Jamie Dimon of J.P. Morgan counterattacked. He condemned the new capital rules and challenged Mark Carney, the chairman of the Bank of Canada and head of the SFB, so violently that Lloyd Blankfein of Goldman Sachs felt it necessary to personally intercede. 20 Bizarrely, Dimon denounced the Basel III rules as anti-American, whereas, in fact, the pressure they placed on the Europeans was far more severe. Rather than raising capital, like their American counterparts, Europe’s main lenders were deleveraging en masse, cutting the size of their loan business. On the basis of plans published by the banks themselves, analysts predicted a contraction of between 480 billion and 2 trillion euros. From the point of view of the regulators, this was exactly what was intended. The banks needed to “derisk.” But it wasn’t only a matter of corporate strategy. What was driving the contraction as much as anything else was the collapse in demand for loans. That spelled trouble ahead for the eurozone economy and it threatened a vicious circle in which a widening depression forced banks to make ever larger provisions for a new wave of nonperforming loans, further tightening pressure on their balance sheets.

Europe’s Banks Under Pressure: Fall 2011 (in billions of euros)

|

2008 legacy assets |

PIIGS debt |

Expected deleveraging |

|

|

RBS |

79.6 |

10.4 |

93–121 |

|

HSBC |

54.3 |

14.6 |

83 |

|

Deutsche Bank |

51.9 |

12.8 |

30–90 |

|

Crédit Agricole |

28.2 |

16.7 |

17–50 |

|

Sociéte Générale |

27.5 |

18.3 |

70–95 |

|

Commerzbank |

23.8 |

19.8 |

31–188 |

|

Barclays |

20.7 |

20.3 |

20 |

|

BNP Paribas |

12.5 |

41.1 |

50–81 |

Note: PIIGS debt refers to holdings of Portuguese, Italian, Irish, Greek and Spanish sovereign debt.

Sources: Bank of England, Financial Stability Report 30 (December 2011), and http://www.forecastsandtrends.com/article.php/770/ .

It was not the misery of youth unemployment in Spain and Greece that made the eurozone crisis into an object of global concern. The world would wake up late to what would be dubbed the “populist danger.” In 2011 it was the prospect of European banking crisis that seized the attention of policy makers around the world. If the trillion-dollar balance sheets of the French, German, Swiss, Italian and Spanish banks were shaking, then the City of London and Wall Street would not be safe. And, as in 2008, the influence ran both ways. If the withdrawal of funding from American sources put the European banks under excessive pressure, they would drastically curtail their business in the United States. As William Dudley of the New York Fed later explained to Congress: “Money market mutual funds which were providing dollar funding to the European banks during the summer and fall [of 2011] were pulling back. Other lenders, large asset managers, were also pulling back from the European banks. And this was causing those banks to start to get out of their dollar book of business. . . . [T]his was going on at a pretty feverish pitch through the late fall and in through the early winter.” 21 The panic was spreading to the American banks themselves. In the fall of 2011 the premium on American bank credit default swaps began to rise ominously. 22

III

On the morning of September 16, 2011, Treasury Secretary Geithner flew to Warsaw to attend, for the first time, the monthly meeting of European finance ministers and central bankers. In his widely leaked remarks he apparently began on a humble note. 23 “Our politics are terrible, maybe worse than they are in many parts of Europe,” he said. The debt ceiling battle had ended in Congress only six weeks earlier. “Given the damage we caused the world in the early stages of the financial crisis and given the challenges we have, we are not in a particularly strong position to provide advice to all of you, so I come with humility.” But he then went on to insist that the “ongoing conflict” between Europe’s governments and the ECB was “very damaging.” “You have to, governments and the central banks have to, take out the catastrophic risk from markets.” Austria’s outspoken finance minister, Maria Fekter, later commented that the American Treasury secretary’s tone had indeed been “very dramatic.” 24 What Geithner proposed was standard American maximum-force firefighting doctrine. “The firewall you build has to be perceived as larger than the scale of the problem. You can’t succeed by shrinking the problem to fit your current level of financial commitments. . . . It’s more dangerous to escalate gradually and incrementally than with massive preemptive force.” According to the Treasury’s own estimates, the eurozone needed a fund of at least 1 trillion euros and preferably 1.5 trillion. 25 Picking up an idea launched by Mark Carney of the Bank of Canada and Philipp Hildebrand of the Swiss Central Bank, Geithner argued that the European Financial Stability Fund should be leveraged to give it sufficient firepower to act as a firewall. 26 The EFSF could borrow against the capital invested in it by Europe’s governments. It was a neat solution, but controversial in Europe, particularly in Germany, because as it increased the fund’s firepower, it also increased the liability for losses.

It was the Europeans who invited Geithner to Warsaw. But in the wake of the Wall Street crash of 2008 and the congressional budget crisis of July 2011, there was probably no moment in living memory in which Europe was less willing to listen to financial advice from America. Jean-Claude Juncker refused point-blank to discuss Geithner’s bailout fund proposal with a nonmember of the eurozone. Geithner stalked out of the encounter refusing comments to the press. As one New York analyst commented: “I’m not sure it’s productive for Secretary Geithner to have gone to Poland given the European resentment towards the U.S. . . . I fear that it may cause Europeans to cut off their nose to spite their face.” 27 That trivializing diagnosis was telling in its own right. But the rebuff to the United States was undeniable. On Geithner’s return, the New York Times ran an unflattering piece contrasting the reception he had received with the triumphalism of the 1990s, when Time magazine had hailed his mentors—Greenspan, Summers and Rubin—as “The Committee to Save the World.” In September 2011 Sheila C. Bair, Geithner’s longtime nemesis as the chair of the FDIC, commented that the Treasury’s advice might have been more compelling if it had come jointly from the United States and China, a point that the Chinese would make at the next G20 meeting. 28

As the leaders of world finance convened in Washington for the annual IMF meeting at the end of September 2011, the mood was grim. The world’s financial institutions were staring into “the abyss,” they declared. 29 From the sidelines Larry Summers, recently retired from the White House, declared: “Now, when these problems have the potential to disrupt growth around the world, all nations have an obligation to insist that Europe find a viable way forward.” 30 The Europeans could not go on pretending that all that was at stake were matters of eurozone governance. The G20 premeeting issued a communiqué stressing that, in the face of the ongoing eurozone crisis, “[w]e commit to take all necessary actions to preserve the stability of banking systems and financial markets as required.” Geithner and his British counterpart George Osborne combined to demand an end to Europe’s “political crisis.” The emphasis on politics was telling. Canada’s finance minister expressed incredulity that the global gatherings had been talking about Greece since January 2010. 31 Geithner warned of a “cascading default, bank runs and catastrophic risk” if Europe failed to build a big enough firewall. Lagarde, from her new vantage point in Washington, insisted that there was still “a path to recovery,” but “much narrower than before, and getting narrower.” 32 And yet a week after the IMF meeting, the EFSF plan that Merkel would squeeze through the Bundestag was undersized, and Finance Minister Schäuble publicly denied any plan to increase it by means of leverage. The Europeans, and the Germans in particular, still did not “get it.”