Chapter 12

STIMULUS

D own a “road to hell” was where the United States was headed. 1 Those were the words of Mirek Topolánek, the lame duck prime minister of the Czech Republic, addressing the European Parliament on March 25, 2009. The embarrassment was that he was not just another Central European conservative. He was speaking in his capacity as president of the European Council just days ahead of the London G20. The economic policies of the Obama administration would destroy confidence, the Czech pressed on. Surging deficits and giant bond sales would “undermine the liquidity of the global financial market.” 2 They were fighting words. Everyone knew that conservatives on both sides of the Atlantic were suspicious of Obama’s administration, but a “road to hell”? Some wondered whether the translators could possibly have got it right. The New York Times reached for history. Perhaps as a survivor of decades of Communist tyranny, Topolánek had a particular allergy to state intervention. President Sarkozy didn’t care. He was furious. How could a jumped-up East European minnow be talking about America that way, and on behalf of Europe, to boot? In London Sarkozy upbraided the Czech about his inappropriate tone. On the back foot Topolánek offered a rather less trite and more disarming explanation. Far from being inspired by the horrors of Stalinism, the phrase had popped into his head after an evening spent listening to the heavy metal classic Meat Loaf’s “Bat Out of Hell.” 3

Whatever the idiom they expressed it with, what stirred conservatives on both sides of the Atlantic in early 2009 was outrage at the first major legislative initiative of the Obama administration: what would become known as the “Obama stimulus,” the American Recovery and Reinvestment Act. Pushed with urgency by the Democrats, it passed the House already on January 28, 2009. At the new president’s insistence it was debated in the Senate in a special weekend session and voted through on February 10. A week later, on February 17, Obama signed the spending package into law. It was the largest measure of fiscal stimulus undertaken in the West in the wake of the crisis and the largest in American history. By the same token, it instantly polarized the economic policy arena on both sides of the Atlantic.

I

Obama’s team never doubted the need to act. Over the winter of 2008–2009 America’s economic situation was deteriorating fast. Jobs were hemorrhaging. Detroit was on its knees. There was a pervasive sense of crisis and a need for renewal. The political stakes were obvious. It was the drama of the financial crisis in September and October 2008 that had broken McCain’s campaign and handed a huge electoral victory to Obama. The atmosphere of hope and expectation that surrounded his inauguration was electrifying. Many projected onto the new president expectations of almost revolutionary change. Not only had Obama brought the advancement of African Americans to a new stage, evoking memories of Martin Luther King Jr. Coming into office in the midst of the financial crisis, he could not escape comparisons to FDR and his famous first “hundred days.” And as if King and FDR were not enough, the newly elected president invoked another era of Democratic Party optimism. He wanted to offer the new generation a Kennedy-style moon-shot mission.

Whatever the Obama administration did, it would have to be huge for the simple reason that the twenty-first-century American economy is huge. GDP in 2008 was c. $14.7 trillion. To have a meaningful impact the stimulus would, therefore, need to be enormous. The problem was that Congress had a hard time dealing with this elementary fact. As the controversy over TARP indicated, a proposal that the federal government should spend a trillion dollars on work creation was likely to cause indignation, panic or both. So the approach the transition team devised was cautious. They would propose $775 billion to the Democratic Party leadership and hope that the notorious log-rolling tendencies of Congress would take the final total close to $1 trillion. 4 If Republican support could be bought with further tax cuts or more spending, the more the better.

Despite the radical expectations projected onto him, Obama was by inclination a bipartisan centrist. What he had not reckoned with was the sheer violence of the conservative hostility toward him. There was no possibility of bipartisanship. Whereas at least a minority of Republicans had voted with the majority of the Democrats to pass the Fannie Mae and Freddie Mac bailouts and TARP, in January 2009 in the House of Representatives not a single Republican voted for the American Recovery and Reinvestment Act, despite the tax cuts with which it was festooned. 5 In the Senate only three did. It was a warning of the depth of partisan hostility the Obama administration would face. From the outset of his presidency, a large section of Republican opinion effectively denied the legitimacy of Obama’s leadership. At the grassroots this expressed itself in the “birther” conspiracy, doubting Obama’s status as a natural-born citizen. In Congress it manifested itself in a stance of absolute opposition. America’s right-wing think tanks mobilized in force to denounce the bailouts and to discredit the stimulus and the financial regulations to come. By the spring the wave of antigovernment indignation that dubbed itself the “Tea Party movement” would roil the base of the Republican Party and hog the television news cycle. In the background, billionaire “dark money” donors, led by the Koch brothers, stirred the pot.

In 2009 the Republicans were in a minority in both the House and the Senate. But their relentless guerrilla war and the drumbeat of their media outlets had real and immediate effects. 6 Above all they shifted the balance within the broad-church coalition of the Democratic Party. The fact that the administration needed the Democrats to vote en bloc in favor of the stimulus gave leverage to so-called moderates—the Blue Dog Coalition and the New Democrat Coalition—free-market, antispending Democrats who were anxious to preserve their hard-won probusiness credentials. 7 As a result, rather than bidding the stimulus up from $775 billion, the congressional “moderates” tended to whittle it down. The result was less substantial than the Obama team had hoped for and less than the US economy needed. The headline for the American Recovery and Reinvestment Act was $820 billion. In actuality it was more like $725 billion in new money, $50 billion less than where the Obama team had started.

Politics dictated not just its size but its shape. The president wanted big-ticket items of innovation. But Obama’s chief of staff, Rahm Emanuel, and his political team were always skeptical that the president’s infatuation with the environmental agenda and green growth would sell. What Capitol Hill wanted were tax cuts and spending programs targeted to please key constituencies. Ultimately, $212 billion of the stimulus went into tax cuts and $296 billion toward improving mandatory programs such as Medicaid (health coverage for lower-income groups) and unemployment relief. This left $279 billion for discretionary spending, of which the president’s priorities of green energy and improvements to broadband received $27 billion and $7 billion, respectively. 8 Altogether, the stimulus would patch up or replace 42,000 miles of road and 2,700 bridges. But unlike in the era of the New Deal, there would be no eye-catching logos, no charismatic monuments like those left by the Works Progress Administration. 9

Nevertheless, it was substantial. In absolute terms it was on a par with the spending of the New Deal. Though it was smaller in relation to a much larger national economy, the Obama stimulus was concentrated over a shorter space of time. 10 In 2009 it placed America alongside the Asian states in the league of activists, outstripping any discretionary fiscal measures taken in Europe. And it worked. Despite the protestations of “freshwater” free-market economists and the complex economic arguments directed against “naïve” Keynesian “pump priming,” every reputable econometric study found that the Obama stimulus had a substantial positive impact on the US economy. 11 Estimates by Obama’s Council of Economic Advisers put the number of jobs created at 1.6 million per year for four years, for a total of 6 million job-years. 12 The multiplier was positive and above 1. This implies that the effect of government spending on the economy was not just positive. More private economic activity was stimulated than the government originally contributed. So the impact of the government’s spending was to shrink the government’s share in overall economic activity.

But if this was the case, if the stimulus worked, why didn’t the Obama administration ask for more? 13 There were political risks in asking for a figure bigger than $1 trillion. But there were risks to undershooting as well. By 2010, America’s unemployment was still stuck above 10 percent. Foreclosures and forced sales were destroying entire communities. Millions of young people left schools and colleges without jobs. Men and women in the prime of life were shut out of the workforce. Many would not return. In the elections of 2010 and 2012 the Democrats fought on the back foot against the backdrop of a limping economy and resurgent Republican activism. They retained the presidency but lost control of Congress. Obama’s administration never built the constituency of Democrats-for-life that was shaped by Roosevelt’s New Deal. Given that they commanded majorities in both the House and the Senate in 2009, why did the Obama team not set the bar higher and pitch for an even larger number? If maximum force was the best approach to financial stabilization, why, when it came to fiscal policy, was the approach so penny-pinching?

Part of the answer is that the transition team did not fully grasp the scale of the tsunami that was descending on the US economy. From preparatory documents circulated within the transition team in early January 2009, we know that the worst-case scenario envisioned by Obama’s staff was for unemployment to reach 9 percent with no stimulus. 14 In fact, even with the largest government-spending program in American history, unemployment topped 10.5 percent. But despite this underestimate, it is clear that the top macroeconomists in the Obama transition team did, in fact, realize that the stimulus ought to be bigger. On December 16, 2008, Christina Romer submitted a report intended for the president-elect arguing that to close the “output gap” by the first quarter of 2011 would require a discretionary stimulus of $1.7–1.8 trillion. Romer’s modeling was conventional. Her figures were sound. Her proposal was a trillion dollars larger than the figure the Obama team ultimately pushed through Congress. What decided the issue was politics, or rather the self-censorship of the economics team in the name of politics. Second-guessing the attitude of Chief of Staff Rahm Emanuel and his political operatives, Larry Summers, as head of the National Economic Council, was convinced that he and Romer would lose all credibility if they suggested anything even close to the figure she thought necessary. The results of Romer’s calculation were, Summers quipped, “nonplanetary.” He did not want to jeopardize the influence of the economics team by appearing naïve and “unsavvy.” The effect was to skew the argument from the start. No figure in excess of $900 billion, half of Romer’s baseline, was ever proposed. A similar deflationary calculus ruled out any dramatic and direct action on home-owner debt.

The great political might-have-been of the early Obama administration is why, alongside TARP and the fiscal stimulus, the White House did not start by pushing a comprehensive relief program for home owners. 15 While the banks and lenders were bailed out, 9.3 million American families lost their homes to foreclosure, surrendered their home to a lender or were forced to resort to a distress sale. 16 The measures that the administration did develop to offer mortgage rescheduling were derisory in their impact. In response to criticism, Larry Summers has subsequently insisted that the question of home-owner relief was a constant subject of debate within the administration. 17 He convened regular monthly meetings with the Treasury and the other key agencies to challenge them to come up with better options. No mechanism that was effective, efficient and politically feasible emerged. There were basic obstacles. A program to help millions of distressed borrowers would have had to have been gigantic in scale. Forgiving loans on a substantial scale would have implied losses for the banking system at a time of financial uncertainty. And it would have caused a huge uproar in Congress, where the administration needed to husband its political capital, not so much with Republicans, from whom nothing was to be expected, but with the moderate congressional Democrats. It was a price that Summers, Emanuel and Treasury Secretary Geithner were not willing to pay.

What became evident in the spring of 2009 was that the historical memory that was most alive in the Obama administration was not that of FDR or JFK but that of the last Democratic administration, under Bill Clinton in the 1990s. It was the Hamilton Project’s vision that prevailed in the Obama camp. In the face of the crisis the Democrats would prove themselves not as bold or imaginative but as sound managers of the economy whose task it was to put right another era of Republican misrule. Though in 2009 no one dissented from the need for an immediate stimulus, the Obama team was profoundly committed to the legacy of their mentor, Robert Rubin. 18 Summers, Geithner and Peter Orszag, Obama’s director of the Office of Management and Budget, were all veterans of the 1990s Treasury. Orszag and Rubin had argued in 2004 that government deficits would not only squeeze private investment but could set up a negative spiral of confidence and expectations and might trigger a sudden panic in financial markets. 19 Faced with the huge deficits produced by the financial crisis of 2008, there was, thus, no contradiction between the maximum-force approach to bank stabilization and the cautious approach to fiscal policy. Concern for confidence in the financial markets was their common denominator.

II

Despite its notable scale, its effectiveness and the political controversy it stirred up, the Obama stimulus was hedged around by political compromise. Furthermore, despite the urgency with which Congress acted, the stimulus was bound to come too late. Spending programs take months, if not years, to be put to work. The discretionary spending component of the Obama stimulus did not begin in earnest until June 2009, at which point the labor market was close to bottoming out. 20 The less commonly noted corollary is that the open-handed fiscal stance of the first year of the Obama administration was in large part an inheritance of decisions and nondecisions made in 2008, while the future president was still in the Senate.

In January 2009, as a result of the standoff between the Bush administration and congressional Democrats, the federal government was operating without a regular budget and was headed toward an unprecedented deficit in excess of $1.3 trillion. It was a political mess and a daunting fiscal hole, but, as far as the economy was concerned, it was precisely what was needed. 21 Part of the reason why Congress had refused to approve the budget presented to it by the Bush administration a year earlier was because it thought it was based on hopelessly unrealistic economic forecasts. Even as the real estate crisis began to make itself felt, the White House projected a deficit of only $407 billion for 2009. The administration called for $3.1 trillion in spending, and at prevailing tax rates assumed that revenue would come to $2.7 trillion. Congress doubted both figures and was proven correct. Thanks to the recession, revenue between September 2008 and September 2009 slumped to $2.1 trillion. Meanwhile, spending soared to $3.5 trillion, including a $151 billion installment for TARP and a first tranche of $225 billion on the Obama stimulus. Fighting over TARP and the Obama stimulus made good political theater for all sides. The programs were significant in their economic impact. But the largest part of the fiscal stimulus of 2009 came as a result of the budget standoff of the preceding year and the collapse in tax revenue due to the recession.

Automatic stabilizers are the unsung heroes of modern fiscal policy. In the United States, no more than one third of federal government spending is discretionary. The rest is made up of mandatory expenditures required by existing “entitlements,” social programs such as unemployment and disability benefits, or retirement pensions. These tend to increase during a recession. Likewise, tax revenue flows into Treasury coffers at preexisting rates of taxation and contribution levels, driven not by political decisions but by the fluctuating fortunes of the economy. Dominated by these nondiscretionary flows, modern state budgets have a powerful stabilizing effect on the economy. As economic activity declines and the economy calls for stimulus, tax revenue falls, entitlement spending increases and the government deficit automatically expands.

Viewed in these terms, the effect of the crisis of 2007–2009 on the budgets of rich countries was spectacular. Whatever the politics of stimulus spending in Congress, the Bundestag or the House of Commons, the automatic stabilizers delivered a huge and timely stimulus. According to calculations by the IMF, if the US economy had been at full employment in 2009, the crisis-fighting policies adopted by the Bush and Obama administrations would have been enough to produce a deficit of 6.2 percent of GDP—this was the discretionary deficit. The actual general government deficit was 12.5 percent of GDP. 22 More than half the support provided to aggregate demand was automatic or quasi-automatic. And this was typical of all advanced economies. According to the IMF’s calculations, of the vast increase in public debt in the developed world over the course of the crisis, just under half was due simply to the reduction in revenue produced by the contraction of the tax base. As profits, wages and spending all declined, this automatically generated a deficit and thus an offsetting public stimulus. This puts a rather different perspective on the fiscal policy battles at the G20. Though Germany, France and Italy steered clear of the kind of stimulus package launched by the Obama administration, let alone that trumpeted by Beijing, their deficits were widening too. As the private sector deleveraged and cut its spending, they too saw huge nondiscretionary deficits. Indeed, it would have taken a heroic and truly perverse act of austerity to prevent these automatic stabilizers from coming into effect. The net result was dramatic. Between 2007 and 2011, demand in the world economy was stabilized by the largest surge in public debt since World War II.

For macroeconomists this was a cause to celebrate the stabilizing properties of the modern tax and welfare state. For fiscal hawks it was a cause of deep concern. In the long run those debts would require higher taxes to service and repay them. This would pose major political challenges. And how would capital markets react? According to the script set out by conventional fiscal conservatism, one might have expected serious and immediate repercussions. Would the debt shock trigger the loss of confidence that Orszag and Rubin and so many others had warned about? How would savers be induced to hold trillions of dollars in government bonds? Would interest rates have to rise? Would this crowd out private investment? Would bondholders get jumpy? Would the bond vigilantes of the 1990s swing into the saddle, selling government bonds, driving Treasury prices down and yields up? In the spring of 2009, as the scale of the deficit became clear, business media reported that markets were up in arms. In light of “Washington’s astonishing bet on fiscal and monetary reflation,” the Wall Street Journal looked forward to a stern response from bond markets. 23

So serious were the rumblings and so painful were the memories of the Clinton era that in May 2009 Obama asked budget director Orszag to prepare a contingency plan. 24 The budget director’s response was drastic. In the case of a bond market panic, the administration should severely hike taxes. The report was intended to be for the eyes of the president only. When Rahm Emanuel leaked it to Summers it provoked a towering fury. Summers threatened to resign and demanded that in the future he must have complete control of all economic policy input to the president. For all his rumpled, academic persona, Summers had a keen eye for power and could sense a new agenda of fiscal consolidation forming within the administration. This was a threat to his personal position. But it also violated his instincts as a “new Keynesian” economist. Summers might have censored Romer’s stimulus proposal, but he did not believe in the power of the “confidence fairies.” 25 To be talking about budget cuts in the early summer of 2009, when the United States was about to hit the trough of the most severe recession since the early 1930s, was wildly premature. If confidence was the issue, the best way to restore it was to engineer a solid recovery.

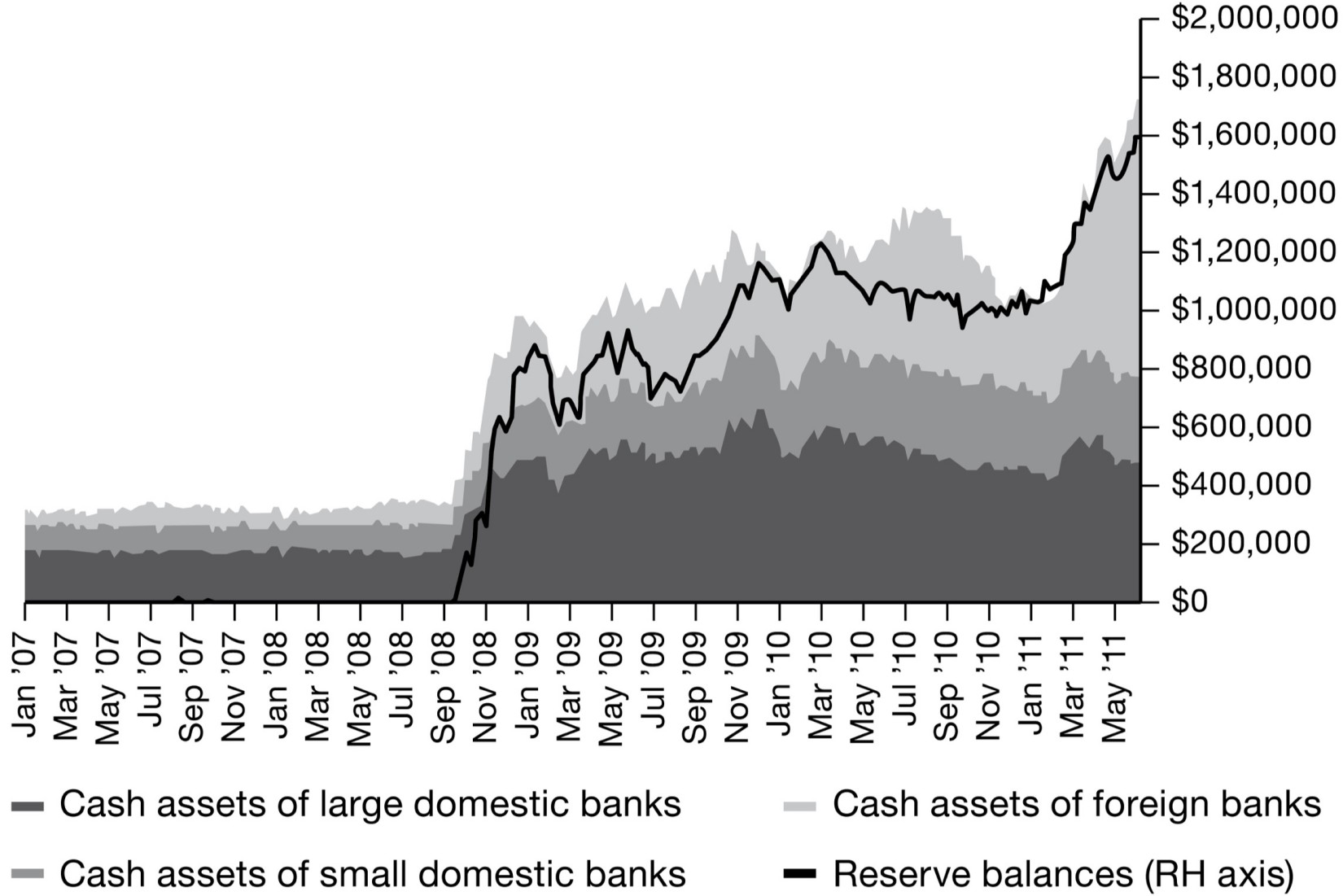

In the event, Summers and the other skeptics were proven right. There was no run against Treasurys. The bond vigilantes were a spook. America’s households were rebuilding their savings. Mutual funds were shifting out of risky mortgage bonds. Everyone wanted Treasurys. These were the kinds of systemic macroeconomic and financial mechanics that all too often escape fiscal hawks, who view the public budget like that of a private household. When the private sector is undergoing a shock episode of deleveraging, when the savings rate is surging as it was in 2009, what is needed to preserve the overall financial balance of the national economy is not for the state to cut its deficit too. Everyone cannot save at once without provoking a recession. As the proponents of “functional finance” have argued since the 1940s, the state must act as a borrower of last resort. 26 In so doing it preserves aggregate demand and provides a flow of safe long-term bonds to financial markets. After the shock of 2008 the entire world was keener than ever to hold safe assets. A huge class of AAA-rated private label securities had shown itself to be far from safe, so the demand for Treasurys was huge. It wasn’t only Americans who wanted US government debt. As Treasury debt held by the public increased by $2.9 trillion between the summer of 2007 and the end of 2009, foreign buyers took more than half. Chinese holdings of Treasurys increased by $418 billion.

Among those who were selling were some of the hardest-pressed banks. They needed to shrink their balance sheets. But that adjustment was cushioned by the central banks. In the first phase of what became known as QE1, on March 18, 2009, the Fed announced that it would purchase $750 billion in agency MBS and agency debt, as well as $300 billion in Treasury securities. The Bank of England made a similar announcement on March 9, committing to purchasing first £150 billion and then £200 billion of British government bonds, or gilts. So, far from swamping the markets with their debt, in 2009 yields on top-rated government bonds actually fell.

In the eurozone things were more complicated. There too the automatic stabilizers kicked in and deficits ballooned. Debt issuance surged. But unlike in the UK or the United States, the ECB is barred from buying newly issued government securities. After Lehman, however, Trichet was in no mood to take risks. Though the ECB did not purchase newly issued government debt, what it did do was to repo sovereign euro bonds. 27 As the eurozone deficits ballooned, the ECB operated what was known informally as the “grand bargain.” 28 It supplied hundreds of billions of euros in cheap liquidity to Europe’s banks in the form of the so-called Long-Term Refinancing Operation initiated in May 2009. 29 The banks then bought sovereign bonds. On average, the rate Europe’s banks paid to the ECB on the CTRO funding was only a third of the yield they earned on their bond holdings. All told, in the eurozone in 2009 the banks loaded up on 400 billion euros’ worth of sovereign debt. 30 It was easy and apparently safe profit, and it was Europe’s most stressed banks, including Germany’s bankrupt Hypo Real Estate and Franco-Belgian Dexia, that were keenest to take advantage. Seeking to maximize their return, they put the ECB’s funds into the riskier peripheral bonds from Portugal and Greece that were offering a marginally higher yield. As in the UK and the United States, this helped to stabilize the government debt market, but there was a crucial difference. In the United States and the UK the central banks were pushing liquidity into the banking system. By contrast, in the eurozone, it was the balance sheets of the banks that absorbed the sovereign debt.

III

Fiscal stimulus was clearly necessary over the winter of 2008–2009. The automatic stabilizers were a welcome complement. Together they helped to revive the advanced economies in the worst crisis they had experienced since the 1930s. Thanks to general macroeconomic conditions and the intervention of the central banks, there was no run in the bond markets in either Europe or the United States. Nevertheless, already in the spring of 2009, anxieties about excessive deficits and the need for consolidation were to be heard on both sides of the Atlantic, and nowhere more so than in Germany.

At the G20 in London, Merkel and Sarkozy had taken a public stance on the need for financial consolidation. In large measure this was political theater. Given the shock to Germany’s export sector, Merkel’s government could not ignore calls for a stimulus package. Unemployment was surging, and in the coming autumn the CDU and SPD had an election to fight. Early in 2009 Angela Merkel’s grand coalition brokered a deal. Finance Minister Steinbrück reluctantly agreed to a modest emergency package of extra spending and tax cuts. 31 Automatic stabilizers would take care of the rest. But the question of fiscal consolidation that had preoccupied Merkel’s grand coalition since 2005 could no longer be dodged. The SPD and CDU agreed that even as they administered the stimulus, budget balance at both the national and regional levels of government would be enshrined in a constitutional amendment.

This was not a resolution forced on Germany by panic in the bond markets or immediate financial necessity. German government bonds (Bunds) were for the eurozone what US Treasurys were for the dollar world, the safe asset of choice. 32 Despite its gaping deficit in 2009, Germany had no difficulty selling debt. It was not markets but the cross-party consensus on fiscal consolidation that had emerged before the crisis that dictated a decisive and irrevocable turn toward austerity. It was a decision driven by a long-term vision of competitiveness and retrenchment, the lobbying of taxpayer and business advocates and the regional interests of the rich states of western Germany. 33 It was a choice that would change the politics not just of Germany but of the eurozone as a whole.

On Thursday, February 5, 2009, at a spartan Bundeswehr barracks in the precincts of Tegel Airport in the northern suburbs of Berlin, Chancellor Merkel personally brokered the deal. 34 Under pressure from ultraconservative Bavaria, the fiefdom of the CSU, the Länder collectively committed themselves to a constitutional amendment that would end all borrowing by 2020. Until 2019, the stragglers—Bremen, Saarland, Berlin, Sachsen-Anhalt and Schleswig-Holstein—would receive annual subsidies of 800 million euros. In exchange they would submit to the external review of their fiscal policy by a so-called Stability Council (Stabilitätsrat). Länder that refused to respond to the council’s advice would lose federal support. Germany’s federal government, for its part, agreed to bind itself by constitutional amendment to borrow no more than 0.35 percent of GDP under normal circumstances. 35 There would be exceptions in case of cyclical shocks, but the cap was severe. It applied to investment as well as to current expenditure.

No heed was given to the consequences that this draconian new rule would have for one of the largest bond markets in the world. Government bonds were seen only as a liability, not as a safe asset for savers. Austerity rhetoric ruled. Prime Minister Seehofer of Bavaria was jubilant. Chancellor Merkel declared a Weichenstellung (a change in the setting of the points). The debt brake was a demonstration that German federalism worked. 36 On March 27, 2009, in the Bundestag, Steinbrück made a typically vigorous defense of the constitutional amendment. It was a matter not of macroeconomics but of democratic autonomy, of “fiscal room for maneuver.” Since the 1970s, despite notional debt limits, annual deficits had resulted in a budget in which 85 percent of federal spending was consumed by debt service and nondiscretionary spending. Fiscal politics were “petrified and devoid of life” (“versteinert und verkarstet ”). 37 Restraint on debt would give back to voters and parliament the freedom to choose their fiscal priorities. The antidebt consensus did not go entirely unopposed. Peter Bofinger, the maverick Keynesian member of the Wirtschaftsweisen, the official expert advisory committee on the German economy, was scathing in his criticism. If the German federal government was issuing no new bunds, where were German savers to invest the 120 billion euros that they sought to put aside every year? Because the German corporate sector was also generating a financial surplus, they could not on balance invest their funds in German businesses. Rather than funding investment at home, Germany’s savings would out of necessity flow into investments abroad. 38 This was the financial counterpart to Germany’s chronic current account surplus, a symptom as much of repressed domestic consumption and investment as it was of export success. When it came to the Bundestag vote on May 29, 2009, the majority was wafer thin—68.6 percent as compared with the two-thirds required—but the amendment passed. It would take another two-thirds majority to undo it.

It was a domestic matter first and foremost. But even before it had been carried in the Bundestag, the debt brake was being touted in Berlin as a major element in Germany’s foreign economic policy. The strong Deutschmark and the independent Bundesbank had made West Germany a model of conservative economic policy. The tough Hartz IV measures set a standard for “labor market reform” in Europe. Now the Schuldenbremse would become Germany’s latest instrument of conservative economic governance for export. 39 For a politician of Merkel’s ilk, the problem of public debt, like the problem of inflation, was a problem affecting all advanced societies. It went back to the 1960s. It had built up over decades. Now was the time to make a stand. As Merkel headed to the G20 meeting in London she hailed Germany’s debt brake as a great achievement. As she told an audience at the German Chamber of Commerce: “We are going to have to try to transfer this to the whole world.” 40

IV

At the London G20, the clash between Merkel, Brown and Obama had enacted familiar transatlantic stereotypes. The Germans were frugal and skeptical about Anglo-Saxon free-market finance. The Americans and the British were freewheeling advocates of whatever it took to keep the capitalist engine spinning. But this was a distortion on both sides. The Germans had plenty of fiscal problems of their own and bankrupt banks to match. Meanwhile, the Obamians were never the full-blooded high spenders that others painted them as. If Treasury Secretary Geithner urged the rest of the G20 to do more, it was in large part in the hope that America might do less. There were Democrats in Congress who wanted to make a major second effort and to push for another round of stimulus. But they got no help from the White House. 41 Inside the administration, Christina Romer cut an increasingly lonely figure in her demand for a bigger fiscal effort. On occasion she would get the backing of Larry Summers. But when she became outspoken in favor of a second round of stimulus, as she did over the winter of 2009–2010, Romer was brutally silenced by Obama himself. 42

What began to prevail in Washington, DC, as in Europe from the late summer of 2009, were the fiscal politics of the precrisis period. The aim of fiscal “sustainability” returned to the fore. Geithner at the Treasury targeted a deficit of 3 percent by 2012, a huge tightening relative to the deficit of 10 percent of GDP in 2009. Even more aggressive was Orszag at the OMB, who ran in-house competitions for the best cost-saving ideas. 43 All the Obama administration’s medium-term priorities tended to point toward streamlining government and trimming spending. The top political priority was health-care reform. Though this was tarred by Republicans as European-style socialism, given the bloated inefficiency of America’s publicly subsidized, profit-making health-industrial complex—which at 17 percent accounted for twice the share of GDP attributable to the financial services industry—the priority of the Affordable Care Act was to cut costs. Likewise, the thrust of Obama’s foreign policy was retrenchment. In 2009 the White House was persuaded to put more troops into Afghanistan, but only because it was simultaneously running down its Iraq commitment. America’s soldiers didn’t like it, but the age of major spending increases was over. Though the Obama stimulus crested in the second year of his presidency, this was offset in 2010 by cuts to other areas of federal spending and a crushing contraction in state and local spending. Though it suited no one to acknowledge the fact, between 2009 and 2010 Germany’s deficit was actually increasing more rapidly than that of the United States. 44 Though the arguments were apparently more transparent, the politics of fiscal policy in the wake of the crisis were in their own way no less opaque than those that framed monetary policy.

Chapter 13

FIXING FINANCE

“C onfidence” is one of the most quicksilver concepts in economics. In 2007–2008 it had been the collapse in confidence in mortgage securitization, money markets and the banks that brought down the house and necessitated the bailouts. By 2009 confidence was still the problem. But now it was government deficits and the supposed threat of bond vigilantes that seized the headlines. Given actually prevailing conditions in bond markets at the time, the constraints this anxiety placed on fiscal policy were a triumph of precrisis centrist orthodoxy over the facts of the postcrisis situation. While the bond vigilantes never appeared, millons of jobless would pay the price for the failure to sustain fiscal stimulus. And the effects went beyond the labor market. The purpose of restraining fiscal policy was supposedly to maintain confidence and to create space for a private sector recovery. But where was that to come from? The real estate market was still collapsing. Households needed to pay down their debts and restore their overstretched finances. Uplift would have to come from business investment. For that there needed to be financial stability and easy credit, and from there the trail led back to the institutions that had actually been the source of the collapse of confidence in 2008, the banks and their dangerous balance sheets. Having excluded a full-scale fiscal response on grounds of protecting confidence, faute de mieux resurrecting the banks came to seem like the most promising path to recovery.

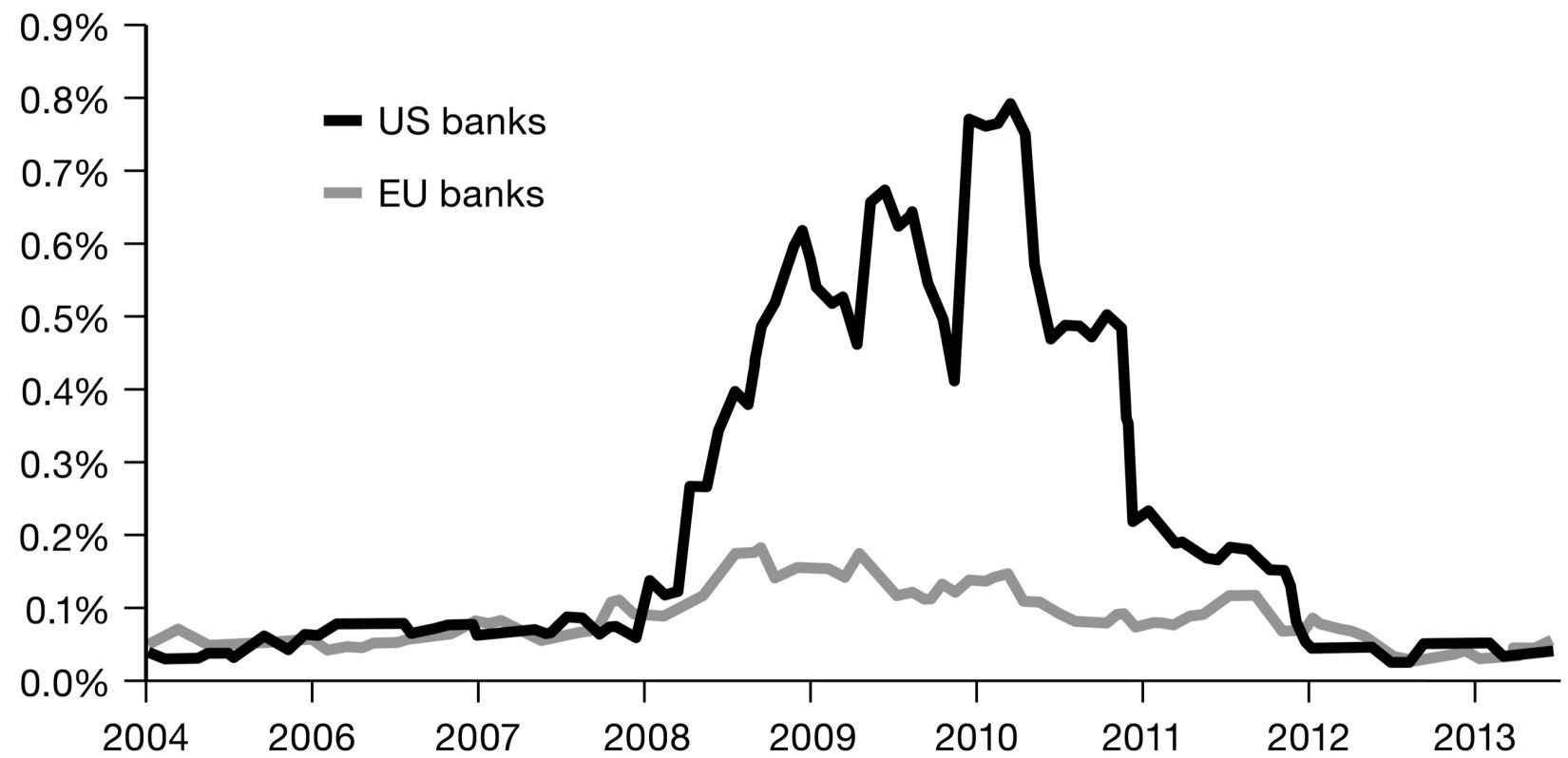

Though the acute general panic of September 2008 had passed, the banks were still very fragile. As the full scale of the losses began to sink in—by May 2009 the IMF was estimating $1.5 trillion in write-downs around the world—default insurance premiums on bank debt surged to 300 basis points in the eurozone and 400 basis points in the United States. 1 At those kinds of rates raising new bank funding was prohibitively expensive. And in the spring of 2009 Bank of America and Citigroup, two of America’s largest commercial banks, were still in danger. 2 Bank of America was digesting the horrors of the Merrill Lynch balance sheet. At Citigroup the situation was even worse. Despite the double capital injection by the Treasury and the ring-fence around $300 billion of its most toxic assets, by May 2009 Citi’s shares were trading at 97 cents. 3 The New York Fed was preparing plans for an all-out rescue effort that would involve guaranteeing all its debt and $500 billion in foreign deposits. Meanwhile, rather than recognizing the political trauma caused by the 2008 bailouts, the bankers in their self-satisfied insulation continued to help themselves to the lion’s share of whatever revenue they generated.

In Britain, the most egregious case was RBS, a now majority state-owned bank that announced in February 2009 that it intended to honor £1 billion in bonus contracts. 4 In the United States the figures were far larger. In the 2008 bonus season, after suffering tens of billions in losses, Wall Street paid out $18.4 billion to its top staff. That was two and a half times the amount that Congress approved for the president’s priority of modernizing America’s broadband infrastructure. Alternatively, if it had been retained by the banks, it would have made a substantial contribution toward their recapitalization. 5 But the investment banks weren’t conventional public companies. They were partnerships run primarily for the benefit of their managerial elite and they expected to be paid, whatever happened. In the 2008 bonus season Merrill Lynch alone was responsible for $4–5 billion in payments. And it made sure to pay out earlier than normal in December 2008, just after the firm revealed a fourth quarter loss of $21.5 billion and days before it collapsed into the reluctant embrace of Bank of America. 6 But of all the bonus scandals, the one that really caught the public’s attention was AIG. It closed its fourth quarter of 2008 with a loss of $61.7 billion, the largest in US corporate history. Nevertheless, on March 16, 2009, the company announced that its Financial Products division, which had been at the heart of the toxic spill, would be awarding $165 million in bonuses, a figure that might rise to as much as $450 million. Even President Obama expressed his “outrage” and demanded redress for America’s taxpayers. 7 What was to be done?

I

One option was nationalization. That is what the British had been forced to do to Lloyds-HBOS and RBS. Germany’s Commerz and Hypo banks were in state hands. Economists pointed out the positive example of Sweden, which when faced with a major banking crisis in the 1990s had taken radical action. After nationalizing and restructuring its banks the economy had bounced back fast. By contrast, Japan had put off restructuring and recapitalizing its banks and had languished ever since. Perhaps the solution was to follow the Swedish example, to break up America’s megabanks, restructure, recapitalize and then return them to the market. What would once have been dismissed as Luddite was now merely common sense. In February 2009, former Fed chair Alan Greenspan, who as a young man had sat at the feet of free-market goddess Ayn Rand, told the Financial Times : “It may be necessary to temporarily nationalise some banks in order to facilitate a swift and orderly restructuring. . . . I understand that once in a hundred years this is what you do.” 8 On network TV news, the Republican senator for South Carolina Lindsey Graham opined that “[t]his idea of nationalizing banks is not comfortable . . . [b]ut I think we’ve got so many toxic assets spread throughout the banking and financial community, throughout the world, that we’re going to have to do something that no one ever envisioned a year ago, no one likes.” 9

The intensity of feeling running against the banks in early 2009 was such that President Obama had to take a stance. At a press conference on February 10, 2009, he took up the international examples that everyone was talking about. He acknowledged the off-putting experience of Japan in the 1990s with its botched bailout and recognized that Sweden had done far better after nationalizing its banks. “So,” Obama continued, “you’d think looking at it, Sweden looks like a good model.” But the president was never comfortable with the comparison: “Here’s the problem,” Obama remarked. “Sweden had like five banks [laughs]. We’ve got thousands of banks. You know, the scale of the US economy and the capital markets are so vast. . . . Our assessment was that it wouldn’t make sense. And we also have different traditions in this country. . . . Obviously, Sweden has a different set of cultures in terms of how the government relates to markets and America’s different. And we want to retain a strong sense of that private capital fulfilling the core—core investment needs of this country. And so, what we’ve tried to do is to apply some of the tough love that’s going to be necessary, but do it in a way that’s also recognizing we’ve got big private capital markets and ultimately that’s going to be the key to getting credit flowing again.” 10

It was not Obama at his most articulate. But it was a clear statement of basic principles. The “core investment needs of the country” were a matter for “private capital.” Government stimulus spending, whether on infrastructure or on education, was incidental. What was crucial was getting the banks back on their feet. It was music to the ears of the man who would deliver the “tough love” that Obama promised—Tim Geithner, his Treasury secretary. For Geithner nationalization was never an option. In 2008 at the New York Fed he had seen the depth of the market panic. He had witnessed the ructions over Bear and Fannie Mae and Freddie Mac. He had been in the room on the afternoon of Monday, October 13, alongside Paulson, Bernanke and Bair when they forced the bankers to take TARP capital. That was enough. As far as Geithner was concerned, to have pushed for further nationalizations in 2009 would have been a “deeply transforming policy mistake.” 11

Despite the united front against the Swedish option that Obama and Geithner presented, given boiling public resentment and the drip of scandalous revelations about the bailouts, the way ahead was far from obvious. Larry Summers and Christina Romer, the leading economists in the administration, were compelled by the Swedish example, as was Paul Volcker. Perhaps a short, sharp restructuring under state ownership was what America’s financial system needed. So intense did the debate become that on the afternoon of March 15, 2008, a summit was convened in the White House to clear the air. 12 With the president looking on, the argument swayed back and forth for several hours before Obama impatiently declared that he had other business to attend to and he expected a conclusion by the end of the night. After the president left the room the issue was decided by his foul-mouthed chief of staff, Rahm Emanuel. If bank restructuring and comprehensive recapitalization along Swedish lines would cost upward of $700 billion, it was not going to “f***ing happen.” After TARP and the stimulus, with health reform in the pipeline, Emanuel could not ask the centrist Democrats in the House to back more spending. The economists would have to come up with another plan.

By 2009 the problem was no longer the investment banks. They were back in profit. The problem was the ailing commercial banks. Citi was the worst. So rather than a comprehensive restructuring of the entire American banking system, the meeting agreed that the remaining TARP funds should be concentrated on backstopping a “resolution” of Citigroup. This gigantic, oversized monolith should be broken up, downsized, restructured and the worst assets hived off to a bad bank. Without alerting Sheila Bair of the FDIC to the intensity of the debate going on inside the administration, Summers had sounded out with her the possibility of creating an $800 billion bad bank for Citi’s worst assets and bailing in its shareholders. 13 The Citi plan was approved by Obama later that evening. The Treasury was charged with working out the details. It ought to have been momentous. Citigroup was huge. Back in 1998 its merger with Travelers Group had sounded the death knell of the old days of “boring” high street banking. By way of Rubin, it was tightly politically connected to the Democratic Party. And the pressure for action was only increased the following day, when the scandal erupted over bonuses paid to AIG’s senior staff. The president was furious. He wanted action. The nation’s top thirteen bank bosses were summoned to a meeting in the White House. 14

At this moment there was a real fear on Wall Street that the Obama administration was about to go to war. Given how unpopular the banks were, it would have made good politics. But it didn’t happen. Despite the decision endorsed by the president on March 15, Geithner never agreed with restructuring Citigroup. No one had ever unraveled a bank of Citigroup’s complexity. It was not clear that the Treasury had the resources and legal authority to carry it through. A protracted restructuring would spook the markets. In the words of a later postmortem compiled by one of Obama’s closest advisers, the Treasury “slow walked” the Citigroup proposal. 15 Though this delaying action bordered on insubordination, Obama showed little inclination to impose his will. As his remarks about the “Swedish case” had suggested, he was far from being a radical on banking issues. When Obama confronted the bank CEOs on March 27 the atmosphere was frosty. But he had summoned them to Washington not to punish them but to remonstrate with them. He appealed to the bankers to show restraint in their compensation and bonuses. “Help me help you,” the president pleaded. When several of the CEOs offered the customary justifications for their exorbitant compensation—their businesses were large and risky; they were competing in an international talent pool—the president interrupted in exasperation: “Be careful how you make those statements, gentlemen. The public isn’t buying that. . . . My administration is the only thing between you and the pitchforks.” 16

In the spring of 2009, rather than going over to the offensive, Obama and Geithner positioned themselves as the last line of defense for America’s financial system. It was their self-appointed mission to calm “the mob.” Of course, playing the good cop is a tried-and-tested negotiating tactic. But it is usually combined with stiff demands. Someone has to play bad cop. What was remarkable in 2009 was how little the Obama administration asked in return for the protection it offered. To the amazement of the hardened Wall Street deal makers, the only item on the table on March 27 was voluntary restraint on compensation. That was even less than Paulson had asked for six months earlier when he foisted TARP on them. In truth, if there were pitchforks being wielded by anyone in the spring of 2009, it was not by the Left against the banks but by the right-wing populists. With the lavish attention of Fox News and subsidies from friendly oligarchs, they were organizing themselves in the Tea Party movement. The target of their anger was not Wall Street but the liberals in the White House. The uncomfortable truth was that the Obamians lacked pitchforks of their own. Reviled by the Right and suspected by the Left of being in the pocket of Wall Street, as Geithner himself admitted, the administration would find itself in political “no-man’s land.” 17

In his early days as Treasury secretary, Geithner was quite commonly described as being formerly of Goldman Sachs. 18 Given the precedent set by Paulson and Rubin, it was only to be expected. Geithner looked the part. He had the precocious youthfulness and pugnacity of a hotshot investment banker. The diary log of the New York Fed revealed that during his time there, Geithner regularly socialized with Citigroup executives, where his mentor Robert Rubin held court. 19 And as Treasury secretary, Geithner continued those habits. 20 But for all his cultivation of Wall Street, Geithner was until 2013 a career public servant, and a proud one at that. In his self-portrayal Geithner was not a banker but a soldier, a man of fortitude, serving in the interest of the national economy and the American people, willing to take upon himself the moral burden of dirty hands, to do what was necessary in the public interest. But how did Geithner define that public interest? First and foremost his commitment was to upholding the stability of “the financial system,” because without that, the entire economy was bound to fail. 21 That was his key article of faith. The interests of America and the financial system were aligned. To explain his actions we do not need to imagine that he was in the pocket of any particular bank. It was his commitment to the system that dictated that Citigroup should not be broken up. Even more important, the key institutions of financial regulation and government must be protected too. When Geithner resisted bank nationalization it was to shield the monetary authorities as much as any individual bank. A comprehensive attack on Wall Street could all too easily spill over into an attack on the agencies that oversaw its business. In 2009 “audit the Fed” was a battle cry on both left and right.

With Geithner at the helm, the Treasury’s response to the crisis was not to tackle “too big to fail” by breaking up the biggest banks. Nor was it to bring the interests of wider society to bear by way of politicized oversight. Instead, the Treasury’s solution was to increase the oversight and managerial capacities of the state’s regulatory agencies—the Treasury itself, the key regulators and the Fed. If capitalist finance was a given, then one would have to accept the necessity of dealing with gigantic banks and complex, fast-moving markets. One had to accept also that this system was crisis prone. Crises, indeed, were inevitable. All one could hope to do was to build a crisis-fighting capacity at the national and international levels that was adequate to cope. In 2008 the Fed and the Treasury had acted on a spectacular scale with effects well beyond the boundaries of the American national economy. At the London G20 the IMF had been given the firepower it needed. What the Treasury aimed to do in 2009 was to continue the consolidation at the national level. As it had done since October 2008, this would revolve around recapitalization. As they recovered from the shock the banks were champing at the bit to repay the TARP funds. To further force the pace the Fed and the Treasury cooperated to introduce a new regime of regulation and oversight known as stress testing. This would be followed by a major political effort to get legislation through Congress that would legitimize and regularize the business of overseeing financial stability. As the acute crisis of 2008 passed into memory, a new relationship between the big banks and the authorities would be given permanent shape.

II

Purely for internal purposes, the New York Fed had for some time been in the habit of conducting crisis simulations with the main banks on Wall Street. 22 In February 2009, in his first major speech as Treasury secretary, Geithner announced that these so-called stress tests would be turned into a comprehensive exercise of public policy. The Fed and the Treasury would inspect and certify the soundness of every major bank operating in America. To do so, all the largest US banks would submit their accounts for inspection. Fed and Treasury officials would then apply to that data a hypothetical scenario of financial disaster, estimating the losses the banks would suffer and the resources they would be able to mobilize to withstand the shock. Effectively, the Treasury and the Fed would make themselves into the credit-rating agencies in chief—the “United States of Moody’s”—official arbiters of private creditworthiness and guardians of confidence in America’s financial system. 23 Those banks that were shown to be at risk would be mandated to raise additional capital. Those that could not do so in the private capital market would be required to take money from the TARP fund.

In rejecting the Swedish option, President Obama had gestured to America’s “thousands of banks.” At the time the president spoke there were, in fact, 6,978 commercial banks operating in the United States. But those never mattered to Geithner or Bernanke. They were the province of the FDIC. What mattered for systemic stability were the nineteen major banks with assets in excess of $100 billion, c. $10 trillion in total. Subjecting those massively complex institutions to thorough scrutiny would have been a labor of Hercules. The stress tests were something more tactical and fast moving. In a crash effort, a scratch team of two hundred bank examiners, supervisors and analysts ran through the books. 24 The disaster scenario they applied was far from apocalyptic. They assumed that GDP would fall by only 2–3 percent, unemployment would rise to 8.5 percent and house prices would fall by between 14 and 22 percent. That turned out to be optimistic. But even starting from those numbers and the default probabilities they implied was enough to generate sobering conclusions. On top of the losses of $350 billion already recognized by the spring of 2009, under the stress test scenario the banks might expect to suffer a further $600 billion in write-downs and charge-offs by the end of 2010. This, then, posed the truly critical question: How much capital would be required to make the banks safe and restore market confidence? This was a matter of judgment. The Treasury and the Fed weighed a range of options from as little as $35 billion to as much as $175 billion. The risk, if they announced a huge capital shortfall, was that it might shake confidence irreversibly. On the other hand, if they announced a figure that was too low, it would undermine confidence in the stress-testing exercise. 25

According to inside reports, the original estimates caused consternation in banking circles. Bank of America faced a call for $50 billion in extra capital. Citigroup was called on to raise $35 billion. Wells Fargo was so dismayed at the initial ask of $17 billion that it threatened a lawsuit. In the end they settled on a bargained compromise. By far the biggest burden was imposed on Bank of America, which was required to raise $33.9 billion to exit the emergency ward. Wells Fargo’s quota was set at $13.7 billion. As its senior financial officer commented: “In the end we agreed with the number. We didn’t necessarily like the number.” 26 Ailing Citigroup had more reason to be satisfied. By allowing for future revenue streams, its capital requirement was massaged down to a modest $5.5 billion, a seventh of the original figure. 27 It was barely more than the bank would pay out in bonuses that year. After weeks of haggling, on May 7, 2009, the public was informed that America’s big banks needed to raise a manageable total of $75 billion.

The stress tests were a balancing act that began with an exercise in accounting precision and ended in a game of bargaining and confidence. 28 Whether they were taken in or simply delighted to discover how helpful the Treasury and the Fed were being, the markets responded well. The spread between very safe AA corporate bonds and the price that banks paid to borrow on their Baa bond rating fell from 6 percent to 3 percent, reducing funding costs. The week following the release saw a sustained 10 percent rally in bank stocks, a high tide on which the strongest banks immediately raised $20 billion in additional capital. On June 19 the first nine banks repaid and exited the TARP program. Over the months that followed, the eight banks still in the program, including the giants Bank of America and Citigroup, used every trick in the accounting book and all the help the highly cooperative IRS, Fed and Treasury could provide to exit TARP. 29 In an extraordinary two-week period in December 2009, Citigroup, Bank of America and Wells Fargo raced one another to raise a total of $49 billion in common equity. Bank of America’s offering of $19.3 billion was the largest offering of common stock in US history. 30 They crowded the market and could probably have raised more capital at lower cost if they had stretched the issuance over several months. But the authorities were in a hurry to wind up TARP, and for the banks time was of the essence. The sooner they could repay the Treasury, the sooner they could escape the limits on compensation imposed on all TARP recipients, thus allowing them to retain and compete for talent. It was, as Bair ruefully remarked, “all about compensation.” 31

This was the script that the administration liked. A light-touch government intervention had enabled private business to take the lead. Nationalization had been avoided. As President Obama had promised, “[P]rivate capital” would be “fulfilling the core—core investment needs of this country.” But what this celebratory narrative glossed over were the more ambiguous implications of the exercise. The stress tests subjected the accounts of the commanding heights of American finance to intrusive scrutiny not by the public and the markets but by select teams of government bank supervisors. By the same token, they placed a seal of official approval on profit-driven private business activity. They were the model of a new regime of comprehensive, anticipatory oversight but also of entanglement between the American state apparatus and the big banks. This might be obtrusive and expensive in bureaucratic terms. It was onerous for those banks subjected to it. But it also conferred privileges, specifically the implicit promise that a bank that passed the stress test was deemed safe by the Fed and the Treasury. If it came to a crisis, a bank that had passed the test could hardly be denied assistance. Among this group of tightly regulated and closely supported entities, there could be no sudden and unforeseen failures. With that risk removed, it was significantly cheaper for such banks to issue shares and borrow money. One study estimated that in the wake of the crisis the advantage in funding costs enjoyed by the larger banks relative to their smaller peers had more than doubled, from 0.29 to 0.78 percent. For the largest eighteen US banks, this implied an annual subsidy of at least $34 billion. 32

III

It was no surprise, therefore, that the markets liked the news. The banks were clearly in safe hands. With the implicit backing of the authorities, the banks finally stabilized. This bought time to think of longer-term solutions. The Obama administration could embark on the huge challenge of financial reform.

The political stakes were high. By the summer of 2009 the White House badly needed a “win.” The stimulus was a dud in political terms. Health-care reform was facing relentless opposition. Financial reform as a political project was defined by the imperative to “get something done.” This forged an unholy alliance between Geithner’s Treasury and the West Wing’s political operatives headed by Rahm Emanuel. Apart from a pugilistic style and a shared fondness for the f-word, Emanuel’s and Geithner’s intensity and single-mindedness bent in opposite, but complementary, directions. For the political fixer Emanuel, all that mattered was getting “points on the board.” The content of financial reform was someone else’s problem. Conversely, for Geithner, with his suspicion of Congress, all that mattered was passing a piece of legislation that gave as little new power as possible to “populist” politicians and maximized the discretion and firepower of the expert regulators. To achieve this goal, however, the Treasury had to work through Congress, and in particular the two key committee chairs, Barney Frank in the House and Chris Dodd in the Senate. They also had to contend with key regulators like Sheila Bair of the FDIC. They had to channel the energy of campaigners, most notably Elizabeth Warren, the Harvard law professor and consumer rights activist, and fend off the ever present banking lobby. 33

The result was a sprawling piece of legislation running to 849 pages. 34 Rather than offering a single coherent thesis, the Wall Street Reform and Consumer Protection Act, commonly known as Dodd-Frank, embodied a compendium of crisis diagnoses. Was the crisis due to mass predation of poorly informed borrowers? In which case what was needed was Elizabeth Warren’s Bureau of Consumer Financial Protection (Title X). Was it opaque over-the-counter derivatives that had blown up the system? In which case the fix was transparent, market-based trading of derivatives (Title VII—Wall Street Transparency and Accountability). Was it the breakdown of responsibility in the extended chains of mortgage securitization that poisoned the well? In which case securitizers should be required to have skin in the game (Title IX—Investor Protections). Was the sheer size of banks at the root of all the problems? Were they simply too big to fail? In which case the answer was to restrict bailouts and to make the industry pay for them (Title II—Orderly Liquidation Authority) and to cap banks’ further growth (Title VI, sections 622 and 623). Had investment banks used client money to gamble? If so, the thing to do was to reinstate 1930s-style divisions between commercial and investment banking by way of the so-called Volcker rule banning “proprietary trading” (Title VI, Volcker rule). All of these theories about the crisis of 2007–2009 had major political resonance. All of them made their way into the meandering text of Dodd-Frank. Many of them were sensible and worthwhile measures that redressed some of the grosser imbalances in the financial services industry. But in general they had little to do with the implosion of the wholesale-funded shadow banking system that actually brought down the house in 2008.

The Treasury had a clearer view of the mechanics of the crisis. It wanted more capital, less leverage, more liquidity. And it wanted centralized powers in the Treasury and the Fed to deal with the next disaster. It spelled out this vision in a blueprint, which it issued in the summer of 2009. 35 This was in many ways quite different from what emerged as Dodd-Frank. But that was not by accident. Many of the omissions were strategic. As Geithner unabashedly remarked, “[W]e didn’t want Congress designing the new capital ratios or leverage restrictions or liquidity requirements. Whatever their flaws, regulators were much better equipped” to decide those technical issues. “History suggested that Capitol Hill would be too easily swayed by the clout of the financial industry and the politics of the moment; we didn’t think that was the place for the intricate work of calibrating the financial system’s shock absorbers.” 36 In other words, what the Treasury and the Fed knew to be the main drivers of the crisis were kept off the legislative agenda. What the Treasury did want Congress to provide were the legal powers that Geithner believed to have been lacking at the crucial moment in September 2008. If the challenge was to structure a more sustainable symbiosis between Washington and Wall Street, that was better done, in the Treasury’s view, by way of the administrative and regulatory state, rather than by way of congressional pitch battles.

Though the Treasury sought to orchestrate a chorus of regulators behind its proposals over the summer of 2009, it soon realized that it would face dogged resistance from the FDIC and from within Congress. They shared a deep suspicion of the complicity of the Fed and the Treasury with Wall Street and the enhanced powers that Geithner was looking for. To ensure collective responsibility, Bair and Frank insisted that oversight over the entire system should be exercised not by the Treasury and the Fed alone but by a Financial Stability Oversight Council chaired by the Treasury but gathering together all the key regulators. The idea of crisis management by committee appalled Geithner. But the council, in fact, was given many of the powers that he wanted. It would have the right to designate systematically important institutions. Those could be placed under a regime of heightened supervision and regulation including regular stress testing. If a large bank was on the point of causing a systemic crisis, the council’s rights of managerial intervention were extensive. Ahead of time, all systemically important institutions would be required to prepare living wills mapping out how they should be resolved in case of bankruptcy. And this oversight and control could be extended to foreign banks operating in the United States.

The Fed was pivotal to Geithner’s vision of future control. But in political terms it was a liability. To say that the crisis dented the Fed’s public standing would be an understatement. It polarized and in due course flipped the politics of the institution. 37 In 2008 Bernanke, like his predecessor, Alan Greenspan, had been significantly more popular with Republicans than with Democrats. By 2010 he was almost equally unpopular with both, and on the right wing the drumbeat of the Tea Party was mounting. Meanwhile, for Obama, Bernanke was a token of the bipartisanship he craved. In August the president announced his nomination for a second term as Fed chair. Time magazine ended 2009 by naming Bernanke its man of the year. 38 But that did nothing to endear him to either the right wing of the Republicans or the left wing of the Democratic Party. 39 December 2009 and January 2010 saw fierce clashes in the Senate over Bernanke’s reappointment. Desperate to rally support, the White House mobilized influential figures such as Warren Buffett to lobby on Bernanke’s behalf. To make matters worse, at the same time Bernanke himself was working the phones, struggling to stop Dodd’s Senate draft of the financial reform legislation from stripping the Fed of oversight over the largest banks. 40

In their effort to retain the Fed’s role at the heart of financial governance, Bernanke and Geithner were forced to make a pawn sacrifice. They conceded the formation of a separate consumer finance agency—Warren’s Consumer Financial Protection Bureau. 41 It allowed the reform campaign to claim a major win. It drew the fire of lobbyists. And it was largely irrelevant to the vision of systemic stabilization that Geithner and Bernanke were pursuing. They could concede regulation of credit cards and consumer loans as long as they retained oversight over the banks with balance sheets greater than $50 billion. Indeed, consumer protection and macroprudential regulation might very well be at odds. As Larry Summers remarked to the president, the “airline safety board shouldn’t be in charge of protecting the financial viability of the airlines.” 42 That was fair but it begged a further observation. Whereas there are plenty of safety agencies, there are, in fact, no agencies responsible for ensuring the financial viability of airlines or any industry other than banks. Airlines are expected to take care of their own finances. But Geithner and Summers preferred to sidestep the ramifications of that thought.

In the wake of Lehman what preoccupied the Treasury most was the question of how a failing megabank could be safely contained. For Geithner there was no substitute for the combination that had finally stabilized the situation in October 2008—wide-ranging guarantee powers by the FDIC ideally in combination with general liquidity support from the Fed and recapitalization and ring fencing of losses orchestrated by the Fed and the Treasury. The crisis had shown the need to add well-resourced resolution authority for those banks that were beyond saving. But the mood in Congress was ugly and Sheila Bair was on the warpath. In the end Dodd-Frank embodied a severe rejection of the practices of 2008. There would be no more taxpayer-funded bailouts. The Fed could offer general liquidity support but was barred from offering facilities tailor-made for specific banks. In consultation with the president and the Fed, the Treasury was required to place failing institutions under the control of the FDIC. It would operate the bank as a going concern with a view to breaking it up and selling off the component parts. The one element of control that the Treasury preserved was that it would be responsible for funding the FDIC’s resolution, with the costs to be recouped after the crisis had passed by a levy on the financial industry. Bernanke and the Fed thought they could live with the deal. The Fed chair had always been unhappy with the ad hoc interventions he had had to make under the terms of section 13(3) emergencies. From Geithner’s point of view it was an alarming restriction. As ever, he turned to his favorite analogy between financial crises and national security: “The president is entrusted with extraordinary powers to protect the country from threats to our national security. These powers come with carefully designed constraints, but they allow the president to act quickly in extremis. Congress should give the president and the financial first responders the powers necessary to protect the country from the devastation of financial crises.” 43

For Geithner the “populist fury” of the “atonement agenda” was a dangerous distraction from the tough-minded technical business of addressing a crisis. 44 But the grief and distress caused by the crisis were forces to be reckoned with. They ran through American society in waves, and early 2010, as Dodd-Frank reached a critical point in its labored passage through Congress, was one such moment. Three years since the real estate bubble burst, the full effects of the credit crunch and mass unemployment were making themselves felt. Between 2007 and 2009, 2.5 million homes had been foreclosed and the crest had not yet been reached. As 2010 began, 3.7 million families were more than ninety days past due on their mortgage payments. Millions more were struggling to make ends meet, one or two months behind on their payments. Over the next twelve months 1.178 million homes would slide into foreclosure, the worst year of the crisis. With prices still falling, ever more properties were sinking into negative equity. As one analyst remarked in early 2010: “We’re now at the point of maximum vulnerability. People’s emotional attachment to their property is melting into air.” 45 In the worst-hit areas, such as Florida, fully 12 percent of properties were given up by their owners or seized by banks for foreclosure. Foreclosure proceedings were operating at such a pace that they were given over to quasi-automated legal processes that turned out to be ruinously flawed. In a nightmarish administrative and legal tangle, ever more victims were sucked into the crisis.

The contrast in fortunes between Wall Street and Main Street was increasingly intolerable. The big banks had been bailed out. Some of the most unscrupulous bosses might face legal action, but they were not facing personal ruin. They retired to lifestyles of wealth and comfort. 46 None had gone to jail. And those at the top of the tree on Wall Street were bouncing back apparently without shame or second thought. The bonus season in 2009 was better than ever, netting $145 billion for the executives at the top investment banks, asset managers and hedge funds, as compared with $117 billion in 2008. 47 Goldman made $13.4 billion in profit for its shareholders and paid its own staff $16.2 billion in compensation and bonuses. 48 Astonishingly, even Citigroup, which had a loss of $1.6 billion in 2009 and survived the year only due to government action, paid out $5 billion in bonuses. The bankers were happy to leave the past behind, but the American public was not. In the spring of 2010 Wall Street’s approval rating with the general public stood at 6 percent. 49 And the regulators and their lawyers were finally catching up with the events of the last three years. On April 16, 2010, the SEC announced that it would be bringing charges against Goldman Sachs for misleading the investors to whom it had sold inferior quality mortgage-backed securities. The announcement unleashed a firestorm of indignation. Finally a really big name was going to have to face the music. To the embarrassment of the administration, Dodd-Frank was carried across the finish line not by the energy of the Treasury or the White House but by a new wave of popular fury.

Emotions ran so high in the spring of 2010 that it took a coalition of Treasury, centrist Democrats and business lobbyists to block a last-minute effort to ban any banks enjoying an FDIC guarantee from engaging in derivatives trading of any kind. For the biggest banks this would have been truly costly. The resulting compromise “pushed out” only 10 percent of the least dangerous derivatives. Similarly, a last-minute proposal to address “too big to fail” by putting a cap on the total size of bank balance sheets was blocked in the banking committee by Chris Dodd and other “moderate” allies. One vital late amendment that did make it into the final law was the Collins Amendment of May 2010. 50 Drafted behind the scenes by the FDIC, it demanded that whatever capital standards the Fed and the regulators set for the biggest banks should at least match the level required of the smaller FDIC-regulated banks. Bair wanted to roll back the favoritism shown to the big banks under the Basel II regime. She also wanted to ensure that capital standards applied to holding companies as well as commercial banking subsidiaries. The Fed and the Treasury resisted. They insisted that setting capital requirements was their regulatory prerogative. The banks screamed that the demanding new capital standards would force them to cut credit by $1.5 trillion. It came down to a struggle in the House and Senate reconciliation process, in which Senator Susan Collins and Bair prevailed with the backing of Dodd.

IV

The Dodd-Frank legislation that Obama signed into law on July 21, 2010, was hailed as the most significant act of regulation since the 1930s. Critics scoffed that it did not set a very high bar. It is easy to be cynical about a messy piece of legislation riddled with compromises and defined as much by what it left out as what it covered. And the incoherence became worse after the passage of the law. While the legislation was in Congress the bank lobbyists—conscious of how high emotions were running—had held back. As they well understood, passing the act was only the first round. Once the law was on the statute books and the argument over implementation began behind closed doors, they swarmed all over the legislation. Amid the inherent complexity of the subject matter, the rivalry between the regulators and the vociferous clamor of the lobbyists, implementing Dodd-Frank became a quagmire.

All told, Dodd-Frank called on regulators and agencies to formulate 398 new rules for the financial sector. Each one became the target for no-holds-barred lobbying by interested parties, who could now operate outside the limelight of congressional debate. By July 2013, three years on from the passage of the law, barely 155 of the 398 required rules had been finalized. 51 The highly controversial Volcker rule was a case in point. 52 How to draw internal divisions inside banks to insulate client money from proprietary trading was a hugely technical and contentious business. Even with the best will in the world it was nearly impossible to draw a line between the actions of a bank in making a market for a client and trading on its own behalf. What emerged was less a “bright” regulatory line than a Rorschach blot. It took until December 2013 for the five agencies involved to agree on a wording of the basic Volcker rule, 1,238 days after Dodd-Frank was passed. 53 The result was a 71-page document with an explanatory addendum that ran to a modest 900 pages. Banks were not so much told what to do as they were invited to demonstrate that they were not in violation of the rule. What exactly would constitute proof of compliance was a matter for further negotiation. 54 The best advice the lawyers could offer was that it was up to banks to decide the level of “regulatory risk tolerance” they were comfortable with. After passing the law in July 2010 and issuing the “final” formulation of the Volcker rule in December 2013, 2014 began with a new round of discussions about the “guidance” that would be issued to explain those regulatory risks. The only thing that was clear was that it would generate enormous demand for compliance officers and corporate lawyers. As Jamie Dimon of J.P. Morgan famously griped, to negotiate the new “system,” a banker needed the services not only of a lawyer but of a psychiatrist too. 55