Chapter 9

EUROPE’S FORGOTTEN CRISIS: EASTERN EUROPE

B y October 2008 the Fed’s swap line facilities defined a relationship of dependence and interdependence between the US central bank and an exclusive club of privileged central bank counterparties. But that posed a question. Who was in and who was out? What were the criteria of membership in the swap line club? 1 On October 28, 2008, Nathan Sheets, the director of the Division of International Finance at the Fed, set out a short list of three criteria. 2 The recipients of swap lines must be:

Of significant economic and financial mass so that there can be spillover to the US.

Well-managed with ‘prudent’ policies so that the problems they have encountered are clearly the result of contagion from US and ‘other advanced economies’ and therefore warrant US assistance.

The problem faced by local banks should be one of dollar funding stress so that swap lines would actually make a difference.”

Ultimately, the Fed had to justify its measures in terms of benefits to the US economy. There were economies that were too small to warrant action. There were countries that were experiencing stress as a result of a collapse of trade or commodity prices that could not be helped by swap lines. But it was point 2, with its stress on “prudent policy,” that offered the scope for political discrimination. What was a prudent policy was very much in the eye of the beholder. As two US analysts attached to the National Intelligence Council remarked at the end of 2009: “Artificial divisions between ‘economic’ and ‘foreign’ policy present a false dichotomy. To whom one extends swap lines” is as much a “foreign policy as economic decisions.” 3 The Fed was well aware that with the swap lines it was treading onto the terrain of geopolitics. Each of the fourteen European, Latin American and Asian central banks included in the swap network was approved by the Treasury and the State Department. They were clearly safe bets. The Fed did everything it could to dissuade further applications. Nevertheless, two further countries did apply and were denied. Their identities are shrouded in secrecy. But there were clearly some countries that were never going to make it onto the Fed’s list, no matter how large or hard hit by the crisis they were.

I

On November 14, 2008, Sarkozy hosted President Medvedev of Russia, who was en route to the first leader-level G20 summit in Washington. Sarkozy and Medvedev exchanged congratulations over the peace settlement that Sarkozy had brokered in Georgia in August. But this was not the only topic of Franco-Russian backslapping. Sarkozy also expressed his agreement with recent initiatives from Moscow on the currency question. 4 Over the summer, with the price of oil at all-time highs, Medvedev had been pushing for a diversification of reserve currencies and a greater use of the ruble. Days before arriving in France, Medvedev had given a speech to the Russian parliament in which he drew parallels between the crisis in Georgia and the global financial debacle. They were “two very different problems,” as Medvedev told the Federal Assembly in November 2008, but they had “common features” and a “common origin”: the presumption of an American government that “refuse[d] to accept criticism and prefer[red] unilateral decisions.” 5 This played well with the nationalist gallery in Russia, but there was not much dissent from the European side either. At their summit in Nice, Medvedev noted that on currency issues “the Russian and European positions were practically the same.” What he did not mention was that whereas France’s banks could count on limitless dollar liquidity from the Fed, the Russians were on their own.

If Moscow’s increasing assertiveness had been buoyed by oil prices surging to $145 per barrel, the crisis was a severe setback. By the end of 2008 oil prices had plunged, reaching their nadir at $34 on December 21. With natural resource rents accounting for 20 percent of Russian GDP, the impact of the commodity price crash was devastating. Tax revenue per metric ton of oil fell by 80 percent. 6 But the Russian state had the resources to cope. Unlike in 1998, by 2008 Moscow had accumulated enough financial reserves to withstand the pressure of the global crisis. At their peak, Russia’s foreign currency holdings were estimated at $600 billion. It was not the state but Russia’s globalized business sector that was in trouble.

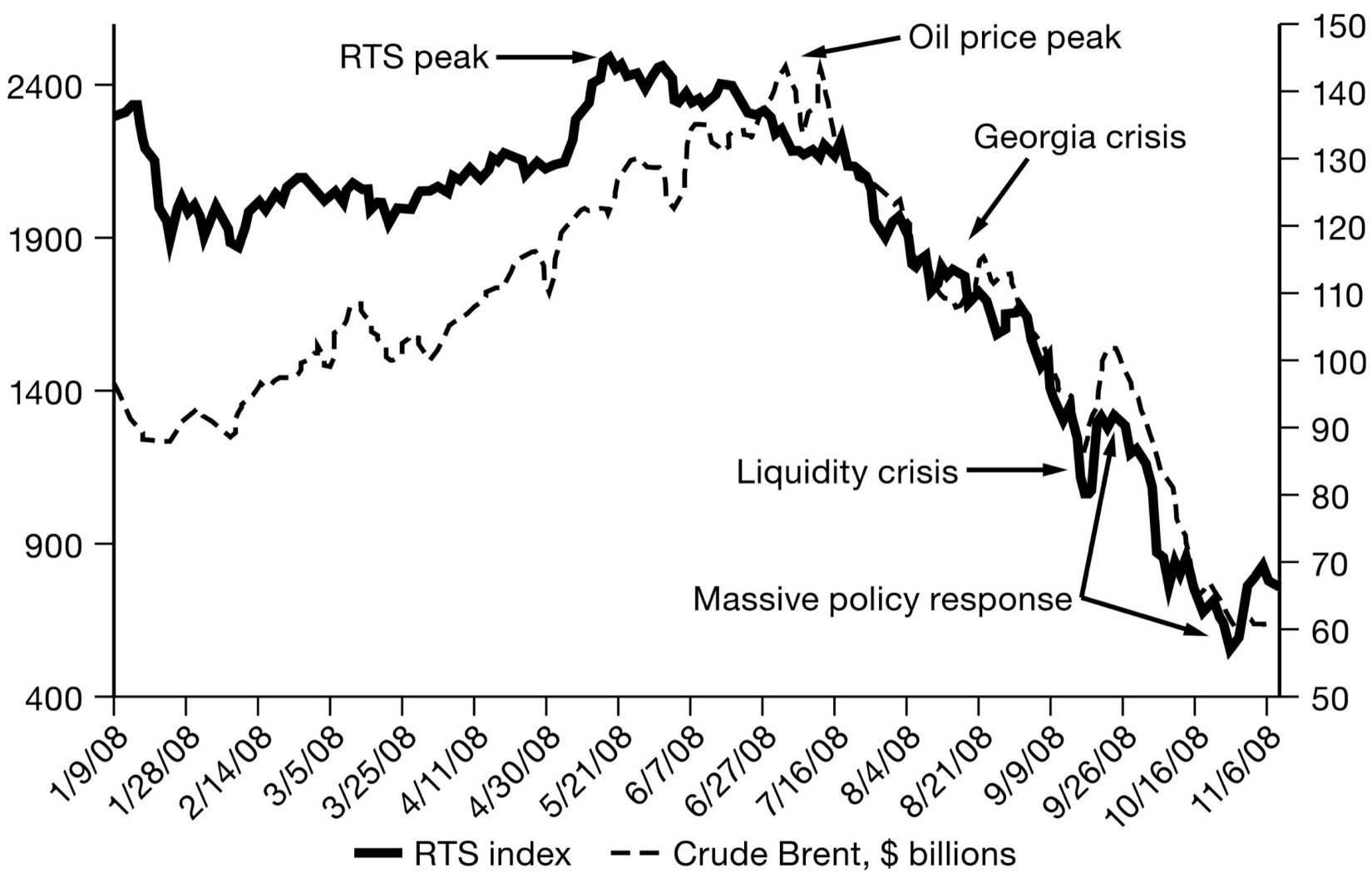

Russian Stock Market and Oil Prices, 2008

Source: World Bank in Russia, Russian Economic Report 17 (November 2008), figure 2.1. Data: RTS, Thomson Datastream.

As oil prices plunged, so did the Russian stock market. By September 15 the Russian market was already 54 percent off its peak in May 2008. In the days after Lehman, trading was so jumpy that Moscow regulators took the decision to suspend trading. When the markets reopened on September 19, jitters continued, with October 6 seeing a single-day fall of 18 percent. 7 According to one widely quoted estimate, Russia’s oligarchs saw their combined wealth slashed from $520 billion at the beginning of 2008 to a mere $148 billion by early 2009. 8 What was spooking investors, apart from oil, was the likely impact of a sharp ruble devaluation on Russian balance sheets. It was the private, not the public, sector that was in danger.

By the third quarter of 2008, Russia’s banks, raw material producers and industrial conglomerates had run up external debts of $540 billion, half owed by Russian industrial corporations and the rest by banks. This debt mountain matched Russia’s official reserves and was roughly equivalent to Lehman’s balance sheet. A substantial fraction was short-term debt. Having adopted the market-based banking model, Russia’s banks were particularly at risk, needing to refinance as much as $72 billion due by the end of 2008. 9 Apart from the banks, the list of stressed dollar borrowers included all the major Russian oligopolies: Gazprom ($55 billion), Rosneft ($23 billion), Rusal ($11.2 billion), TNK-BP ($7.5 billion), Evraz ($6.4 billion), Norilsk ($6.3 billion) and Lukoil ($6 billion). Collapsing commodity prices slashed their revenues and a slide in the ruble would put even heavier pressure on those that billed in local currency rather than dollars—a major issue for Gazprom, Russia’s largest gas supplier.

As in the West, the crisis and the terms of the bailout opened the question of the balance of power. To some it seemed that the Kremlin was bent only on saving the skins of its cronies at the expense of the Russian taxpayer. 10 On this reading, the Russian story was an even more corrupt and brutal version of the drama played out in America. 11 Like the barons of Wall Street, Russia’s oligarchs needed state aid and the regime came to their rescue. It is certainly true that Russia avoided dramatic bankruptcies, and considerable state resources were deployed to make sure of that. But putting events in Russia side by side with those in the United States or Europe, one is struck less by the self-dealing of Russian crisis management than by the frankness with which the question of power was ventilated in Russia and the obvious willingness of President Medvedev and Prime Minister Putin to use the occasion to shift the balance in their favor. Since the breakup of oil conglomerate Yukos in 2003, none of the oligarchs had dared to challenge the Kremlin. Now Medvedev and Putin were turning the screw. They offered financial protection, but they exacted a price.

The cornerstone of the Kremlin’s crisis-fighting strategy was to prevent a death spiral of devaluation and bankruptcy. In the first phase of the crisis, the central bank deployed its ample foreign currency reserves to stem the fall in the ruble. As a result, as oil prices plunged by 64 percent between October and December 2008, the ruble lost only 6 percent against the dollar. 12 Only in January did Moscow let the ruble go, allowing it to devalue by 34 percent before stabilizing in February. Like any successful rearguard action, it came at a price. The central bank burned $212 billion of its reserves, 35 percent of the total, to slow the slide. But by so doing it bought time, allowing dollar-exposed borrowers to pull in their horns and giving the state some time to launch its own response. 13

A key element of this program was a demand from the Kremlin that the oligarchs sink a large part of their fortunes into stabilizing the stock market. There were rumors of an “all-night mandatory meeting held in the Kremlin” on September 16, the day of the AIG rescue, at which “oligarchs were ordered to plunge cash into their own faltering stocks, buy collapsing financial institutions directly, or simply fork over the cash and/or shares.” 14 Following this “bail-in” of the oligarchs, the government targeted takeovers and bailouts at the smallest and weakest Russian banks. Coordination was provided by state-owned Vneshekonombank (VEB), where Putin, as Russian prime minister, served as chairman of the board. Five billion dollars was used to take over Sviaz Bank, Globex bank and Sobinbank. Then the deposit insurance fund was recapitalized and the insurance limit raised to $28,000. A $50 billion central bank facility put VEB bank in a position to act as the backstop, with a further $35.4 billion in subordinated debt available at tough rates for troubled oligarch enterprises. The loans would be repayable within a year and otherwise convertible into controlling shares. 15 It was not a government takeover, but a conditional threat and a stark demonstration of where power lay.

VEB pumped $4.5 billion into Rusal, the aluminum company majority owned by Oleg Deripaska, to allow it to unwind foreign financing, which it had used to buy a 25 percent stake in mining giant Norilsk Nickel. VEB also put $2 billion into Mikhail Fridman’s Alfa Group to help it to pay off Deutsche Bank and rescue Alfa’s large stake in Russia’s number two mobile phone firm, VimpelCom, which might otherwise have been forfeited as collateral. As investment plunged and domestic economic activity began to spiral downward, unemployment rates doubled. This was particularly worrying in the so-called monotowns—the urban legacy of Stalinist industrialization. 16 On October 16, 2008, Igor Sechin, Putin’s right hand, convened an industrywide brainstorming session on the car industry at Togliatti, the company town of AvtoVAZ, the bankrupt inheritor of the Soviet car industry. He announced an immediate $1 billion loan for AvtoVAZ from VEB that would keep the factory and its staff of 100,000 working. 17 By the end of the crisis, $1.7 billion would be pumped into the Russian auto bailout.

In the wake of the oil price shock, the Russian federal budget was reset on the assumption of an average oil price of $41 per barrel by contrast with the June 2008 budget, which had assumed $95 per barrel. With tax revenues plunging, Putin, as prime minister, took credit for a large fiscal stimulus. A quarter of the government’s 9.7 trillion ruble budget was dedicated to crisis spending on work creation, industrial subsidies and tax cuts. Relative to the size of its economy, commonly compared with that of Spain and roughly comparable to that of Texas, the Russian crisis response was one of the largest in the world, dwarfing those undertaken by West European governments. 18 It was heavily skewed toward the largest, best-connected corporations that were included in a list of 295 nationally important corporations and 1,148 regionally important firms. It was a top-down, corporatist stimulus, and Moscow made clear that it expected the oligarchs to reciprocate. Indeed, it was unafraid to call them out by name. On one notable occasion, Putin singled out four of them as follows: “Vladimir Potanin (Interros Holding), Leonid Lebedev (Sintez Group), Mikhail Prokhorov (Onexim Group), and Viktor Vekselberg (Renova Group) . . . I have known all of you for many years; in essence, we have been working jointly. Let me repeat that during the difficult conditions of the crisis we have made every effort to support you in the various directions of your business. The crisis is waning. It’s not yet over, but it’s on its way.” Now Putin expected them to make good on their commitments. “We agreed to meet you half-way in this area as well. We postponed the deadlines for investments. There will be no more such adjustments of schedules. Please focus your utmost attention on meeting your commitments.” 19 What would happen if an oligarch failed in his responsibilities was demonstrated in June 2009 when Putin descended on Pikalevo, a small town south of St. Petersburg dominated by the metallurgical empire of Oleg Deripaska. Deripaska, who had once been listed as the richest man in Russia, with a fortune estimated at $28 billion, had seen it reduced to $3.5 billion. But that was no excuse for not paying wages. 20 Indignant workers were blockading the Moscow highway, causing a 250-mile traffic jam. In front of the TV cameras Putin upbraided Deripaska. Tossing him a pen, the premier demanded that the oligarch sign the paychecks there and then. It was economic management by personal intimidation of the telegenic tub-thumping variety. 21 The message was clear. Ten years on from the humiliation of 1998, there were men in charge who would see to it that things “got done.”

In its way, it was effective. It demonstrated leadership. It humbled the oligarchs. It rallied Russian social interests around the state that provided for them. It kept Prime Minister Putin in the limelight. But was it a long-term strategy for growth? Liberal economists were skeptical. So too was Medvedev, who had succeeded Putin as president in 2008. Even before the crisis, the expert advisers that Medvedev cultivated in his personal entourage had been calling for a new course. 22 In the wake of the crisis their message was even louder. What had made Russia so vulnerable in 2008 was its lopsided integration into the world economy: on the one hand, its excessive reliance on oil and gas; on the other hand, the corrupt culture of capital flight, in which Russian oligarchs sluiced money in and out of the country through the off-shore banking system. How else could one account for the bizarre anomaly that made tiny Cyprus into one of Russia’s main sources of foreign investment? What Russia needed was modernization. As Medvedev remarked on September 10, 2009: “Can a primitive economy based on raw materials and economic corruption lead us into the future?” 23 Two-fisted crisis fighting was not enough. A mere recovery from the shock of 2008 would lead “nowhere. We need to get out of the crisis by reforming our own economy.” 24 What Russia needed was economic transformation, and for that it needed not less but more interaction with the world economy, and above all with its technological leaders. And this had wider implications. After the shocking confrontation with the West in August 2008, Moscow needed to change course. With the crushing of Georgia, the Kremlin had made its point. In the future, Medvedev asserted, the success or failure of Russian foreign policy should be judged by a single criterion: “whether it contributes to improving living standards in our country.” Rather than “puffing out its cheeks” to threaten others, Russia should concentrate on attracting foreign technology and capital. 25 It was a message of modernization and partnership that was eagerly taken up both in European capitals and by the new administration in Washington.

II

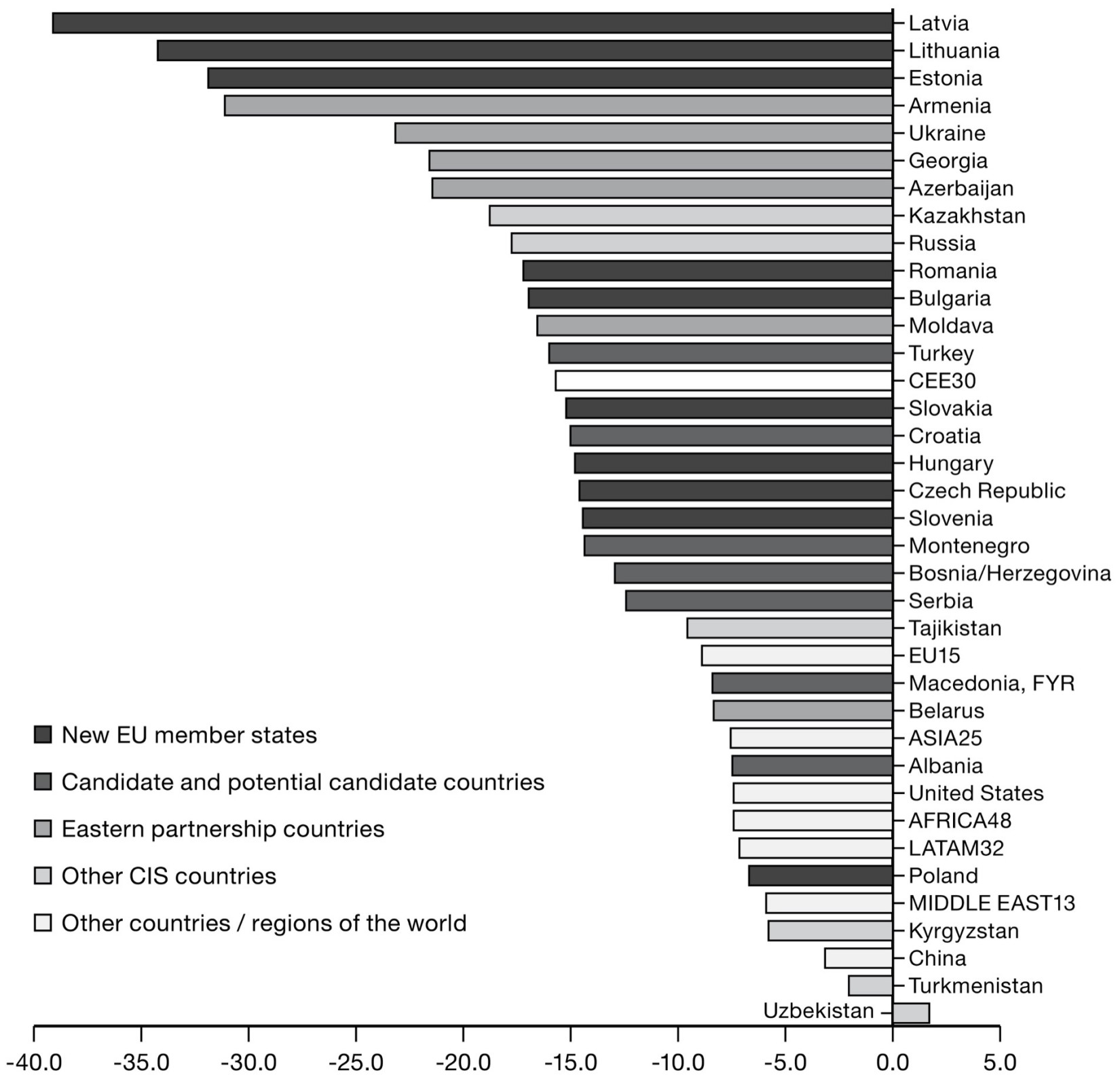

It might be tempting to conclude that by taming Russia, the effect of the crisis was to calm international relations. And in the short run this was surely true. But in the international sphere, power is judged by relative standards. And if Russia was hard hit by the 2008 crisis, the impact on Eastern Europe was even worse. The shock to the most highly leveraged transition states of the former Communist bloc was staggering. If we compare the forecasts for 2010 made in October 2007 with the expected outturn two years later, we see how radically the crisis changed the outlook for the worst-hit countries in the region.

The most extreme case was Latvia. One year into the crisis, in October 2009, the IMF’s forecast for Latvia’s GDP in 2010 was 39 percent lower than it had been in October 2007. Over the same two-year period, Estonia’s and Lithuania’s GDP expectations were revised downward by a whopping one-third. Slovenia, the Czech Republic, Slovakia, Hungary, Bulgaria and Romania all experienced downward shocks of between 15 and 18 percent, more than twice that suffered by the United States. In the adjoining post-Soviet Commonwealth of Independent States (CIS), the downward revision of growth expectations ranged from 18 percent for Russia to 32 percent for Armenia. The pattern was not uniform. Poland, notably, escaped largely unscathed. 26 But all the most severe casualties of the 2008–2009 crisis are to be found among the transition economies of the former Eastern bloc.

The Shock: October 2009 Forecasts for GDP in 2010 compared to Octoer 2007 Forecast, Percentage Difference

Source: Zsolt Darvas, “The EU’s Role in Supporting Crisis-Hit Countries in Central and Eastern Europe,” Bruegel Policy Contribution 2009/17 (December 2009), figure 1.

Individually, the East European states are not big economies. But taken together they formed a substantial unit comparable in economic heft to France or the state of California. They were the pride of Europe’s transformation process, and the battleground in the new confrontation with Russia that had taken shape between 2007 and 2008. They were eager disciples of market liberalization and financial globalization. That put them especially at risk as global financial markets collapsed. The situation was made even worse, however, by the source of the capital that fueled their growth: the overleveraged banks of Western Europe. In total, the West European banks and their local branches had $1.3 trillion at stake in emerging Europe, $1.08 trillion excluding Russia. 27 As the balance sheets of the European banks were being crushed on the other side of the Atlantic, the risk was that they would dramatically curtail their operations in Eastern Europe.

Before the crisis struck it was normal to see an average of $50 billion flowing into the emerging markets of Eastern Europe and the post-Soviet world every quarter. In the last quarter of 2008 that suddenly reversed, with an outflow of $100 billion and a further $50 billion in the first quarter of 2009. 28 The pyramid of credit established over the previous fifteen years was shaking. In a “natural” process of adjustment, the floating currencies of Eastern Europe plunged. The result was a catastrophic increase in the local currency cost of servicing international loans. 29 In Bulgaria, Romania, Hungary and Lithuania, foreign loans made up more than half of all credit. As the forint plunged, in a matter of weeks Hungarian families saw their mortgage and car loan bills surge by 20 percent. The worst affected were the Hungarian families whose debts were denominated in Japanese yen. They faced a 40 percent increase in their debt burden as the yen soared. 30

Whereas Russia had reacted to its humiliation in the 1990s by accumulating a substantial currency reserve, the East European states had no such defense. For them security lay in integration with the West, or at least so they imagined. With the Fed having used swap lines to stabilize a core group of economies in which American interests were undeniable, one might have expected the ECB to extend similar support to the East European neighbors of the eurozone. Certainly this was the expectation of the Fed. If one applied the three criteria set out by Nathan Sheets to Eastern Europe, the case for ECB assistance was clear-cut. 31 The East Europeans were EU members and aspired to future eurozone membership. As such, the respectability of their economic policy was vouched for in general terms. The crisis in Eastern Europe was immediately caused by a sudden stop in foreign credit supply. And the eurozone’s own banks were deeply involved and stood to suffer substantial losses. The risk of blowback was acute. As Sheets remarked to the FOMC: “I think it is very appropriate for all the European EMEs to report to the ECB for their liquidity needs.” 32 But whereas the Fed had effectively licensed the ECB to issue dollars, the ECB had no intention of extending equivalent privileges to Poland or Romania. With Sweden and Denmark the ECB established publicly announced swap lines. Their banks would supply liquidity to Eastern Europe. Meanwhile, the central banks of Poland and Hungary were fobbed off with repo arrangements that treated them no better than stressed commercial banks in need of extra liquidity. The only assistance that the ECB was willing to provide was to give them short-term funding in exchange for first-class euro-denominated securities. When the problem was a shortage of euro funding, that was not a great help. What they needed was a swap facility for Hungarian forint or Polish zloty. Even the limited facilities offered by the ECB were extracted only thanks to urgent pressure from the Austrian and French central banks, which had particular reason to worry about the losses their banks might suffer on their East European portfolios. 33 Austria’s banks were in particular difficulty because they had made loans in Swiss francs, funding them with borrowing in Switzerland, where interest rates were low. Now the Swiss franc was soaring and funding was scarce. To tide them over, the Swiss Central Bank offered full currency swap lines in exchange for euros, but not for Polish zlotys or Hungarian forints. 34

Membership in the EU and NATO was supposed to have promoted Eastern Europe from their inferior status in the global pecking order. Ex-members of the Warsaw Pact and former Soviet republics had eagerly refashioned themselves as exponents of Donald Rumsfeld’s new Europe. They now found their prospects for growth shattered and their governments thrown back to where their post-Communist careers had begun, as lesser sovereigns, and more or less resentful supplicants for international financial assistance. The IMF was their last resort. This was traumatic. No one in Eastern Europe wanted to relive the bitter aftermath of the collapse of communism, with which the IMF was indelibly associated.

The first and most desperate application for assistance from within the EU was Hungary’s. 35 On October 27, 2008, Budapest reached agreement with the IMF and the EU (as opposed to the ECB) on a $25 billion loan package. At 20 percent of Hungarian precrisis GDP, it was a very substantial commitment and an unusually generous multiple of Hungary’s IMF capital quota. 36 The IMF considered the program to be unusually lenient. Unsurprisingly, the Hungarians did not see it in such favorable terms. Hungarian politics polarized as the austerity program bit. The nationalist daily Magyar Hírlap described Hungary as being slowly garroted by a “credit noose around our necks.” 37 For the extremists of Hungary’s Far Right it was a short step back in time from the “neocolonialism” of the EU and the IMF to the Treaty of Trianon, which had eviscerated Hungary after World War I. In 2010 the right-wing Fidesz party would reap the benefits with a crushing electoral victory, setting Hungary on the path to a self-declared illiberal democracy.

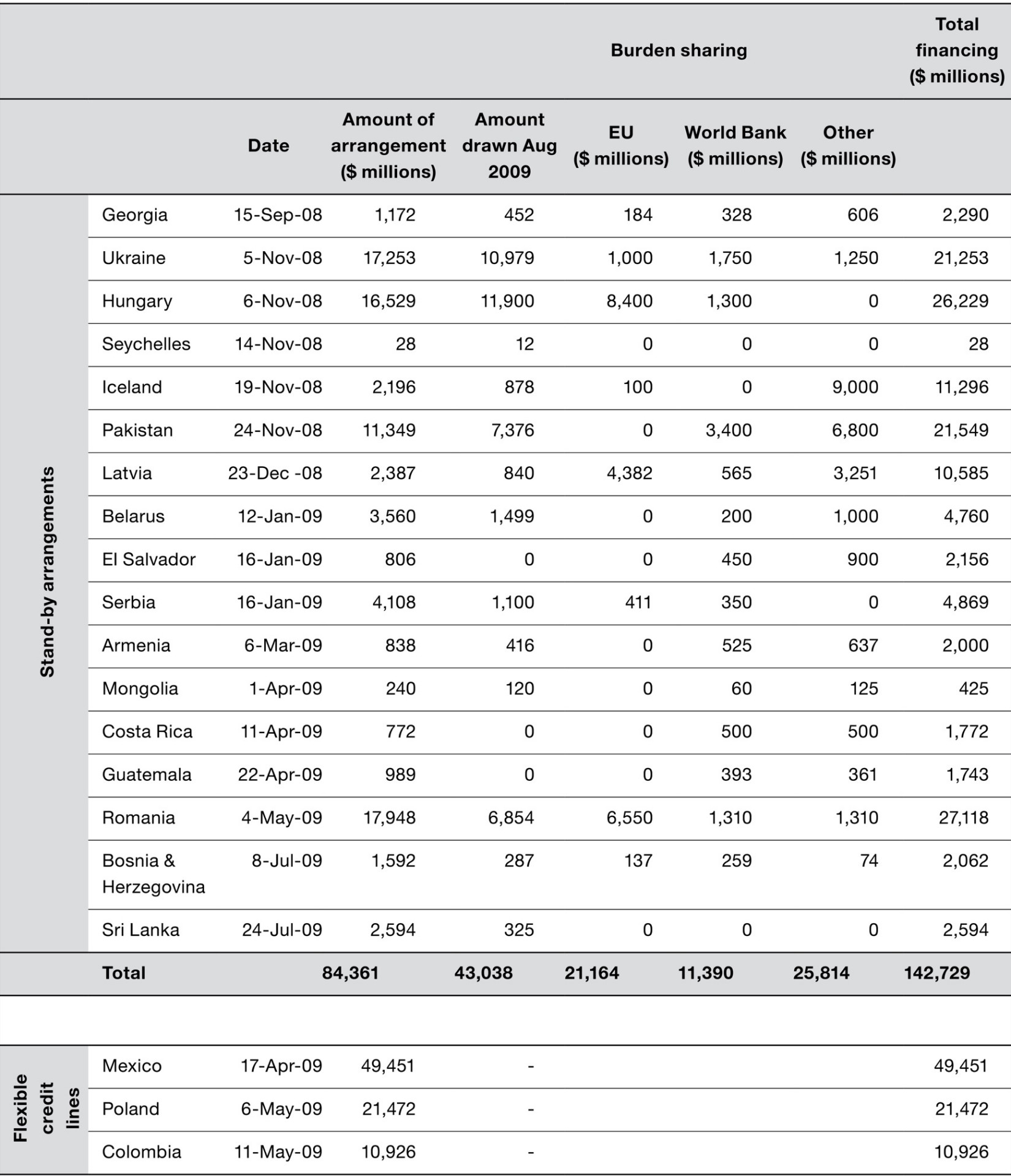

IMF Crisis Programs (as of August 2009)

Source: IMF, Review of Recent Crisis Programs (September 14, 2009), Appendix I, https://www.imf.org/external/np/pp/eng/2009/091409.pdf .

The IMF’s Hungarian aid package of October 2008 was followed by programs for Iceland, Latvia, Ukraine and Pakistan. 38 In 2009 Armenia, Belarus and Mongolia would be forced to apply to the IMF for help. Less than a year after it had played host to the contentious NATO summit, Bucharest found itself negotiating an IMF program. Precautionary credits would be offered to Costa Rica, El Salvador, Guatemala, Serbia, and Bosnia and Herzegovina. Additionally, at the urging of Washington, a new, minimally invasive flexible credit facility, offering a total of more than $80 billion in ready cash, was made available to Mexico, Poland and Colombia. Mexico thus had the singular distinction of receiving both a swap line and an IMF credit facility.

Thanks to the IMF and EU intervention, an immediate meltdown was avoided on the East European periphery of Europe in the fall of 2008. 39 But the situation remained extremely precarious. And it was dangerous not only to the borrowers. Austria’s adventurous banks had since the 1990s accumulated claims on Eastern Europe equal to more than 55 percent of Austrian GDP. The exposure of Austrian banks to Hungary and Romania, the countries with flexible exchange rates that seemed most likely to suffer payment shock, came to 20 percent of Austria’s GDP. German, French and Italian banks all had large claims on Eastern Europe, but these were manageable in relation to domestic resources. The other lender that was seriously exposed was Sweden, whose banks had almost entirely monopolized the banking markets of the Baltics, feeding a roaring real estate boom. There was acute anxiety on the part of international agencies such as the World Bank and the Bank for European Reconstruction and Development that an abrupt withdrawal by one or more stressed West European banks could precipitate a chain reaction that would overwhelm the modest resources provided by the IMF and the EU Commission. Desperate to reduce leverage on all fronts, West European banks would pull out of Eastern Europe en masse, unleashing a ruinous rush to the exit. Bob Zoellick, George Bush’s nominee to head the World Bank, was deeply concerned about Europe’s future. “It’s 20 years after Europe was united in 1989,” Zoellick reminded the readers of the Financial Times in early 2009, “what a tragedy if you allow Europe to split again.” 40 The new Europe, which the United States and the two Bush presidencies in particular had been fostering since the end of the cold war, was in jeopardy. Evoking a different chapter in Europe’s history, the Viennese press was warning of a “monetary Stalingrad” that threatened Austria’s and Italy’s banks. 41

The situation was serious. But the alarmist talk in Central Europe was also a reflection of the fact that Western Europe wasn’t listening. Berlin was no more enthusiastic about a collective European solution in Eastern Europe than it had been in the eurozone. Germany shot down Austrian and Hungarian initiatives for a common support fund. 42 “Not our problem,” Peer Steinbrück announced. East Europeans did not fail to notice that as a eurozone member, Greece seemed to be weathering the storm rather better than Hungary, even though its financial fundamentals were no better. 43 In early 2009 there were calls, ironic in light of later events, for Poland and other East European EU members to be put on a fast track to eurozone membership, thus bringing them under the protective umbrella of the ECB. 44 A confidential IMF staff report backed the proposal arguing that “[f]or countries in the EU, euro-isation offers the largest benefits in terms of resolving the foreign currency debt overhang [accumulation], removing uncertainty and restoring confidence. Without euro-isation, addressing the foreign debt currency overhang would require massive domestic retrenchment in some countries, against growing political resistance.” 45 But no help was to be expected from the ECB. It had no interest in entangling itself in Eastern Europe.

In December 2008 the most exposed Italian and Austrian banks began clamoring for a concerted program of international assistance. Finding the door closed in Brussels, they turned to Vienna, which, given the extent of Austria’s entanglement, could not afford to let things slide. Circumventing Brussels, the Austrian government announced what became known as the Vienna Initiative. This multilateral scheme committed the World Bank, the European Bank for Reconstruction and Development and the European Investment Bank to a program of 24.5 billion euros in new lending and capital injections. Crucially, it was flanked by an agreement with at least some of the leading private banks. On a case-by-case basis the Vienna Initiative extracted pledges from the leading lenders that they would maintain their lines of credit to the region, thus preventing an even more dramatic credit stop. 46 UniCredit and Banca Intesa of Italy, Raiffeisen of Austria and Swedbank of Sweden all participated. Commerzbank of Germany and Deutsche Bank did not. 47

As it turned out, the most important battleground for East European stabilization was a long way from Vienna. As the twenty-first century began, Latvia, Lithuania and Estonia had seemed like the lucky ones. Unlike other former Soviet republics, such as Ukraine, Georgia or Belarus, they had successfully transitioned to full membership in both the EU and NATO. Furthermore, unlike Hungary or Poland, the Baltics were eager to join the euro as soon as possible. In anticipation they had pegged their currencies. In 2008, despite the sudden stop to foreign capital inflows, they were under great pressure to remain on their convergence track. But as foreign credit dried up, maintaining their fixed exchange rates became ever more painful. When in early 2008 the IMF had contemplated the possibility of a crisis triggered by macroeconomic imbalances, Latvia, with its yawning current account deficit, had been singled out as particularly vulnerable. 48 Then it had been viewed in isolation as a national problem case. Now Latvia faced the unwinding of its huge deficits in the context of a comprehensive global crisis that had forced its regional competitors in Poland, Hungary and Romania to devalue. If the Baltics did not follow suit, how were they to keep up? How would they cope without foreign funding? How could they regain export competitiveness and shrink imports if they could not adjust their currencies against the euro? Without devaluation the only way to right the trade balance was by rebalancing domestic demand, cutting wages, raising taxes and slashing government spending. This was painful, but given the advanced stage of financial integration that the Baltic countries had already reached, devaluation was dangerous too. With 80 percent of credit outstanding sourced from their European neighbors, any substantial depreciation was likely to trigger wholesale default. The cost of servicing their debts in euros would simply have become prohibitive. Though they were not yet members of the eurozone, in early 2009 the Baltics faced a predicament that was a grim precursor of things to come.

Because of the scale of its debts and the deep involvement of Scandinavian banks, Latvia was commonly seen as the key to stability in the Baltics. 49 If it abandoned its peg, contagion would most likely spread to Estonia and Lithuania, and from there to Slovakia and Bulgaria, which were also struggling to hold their currencies in line with the euro. 50 Once a wave of further devaluations began, it would be impossible to uphold the defenses put in place by the Vienna Initiative. Fire sales would sweep Eastern Europe. Some might get out alive. But for two of Sweden’s most important banks, Swedbank and Nordea, the entanglement with the Baltics was existential. 51 If their loans were written off, the capital of both banks would be completely wiped out. As a BNP Paribas analyst put it, “Latvia may be a small country but it has vast repercussions.” 52 One Central European minister of finance, who preferred to remain anonymous, predicted that the chain reaction across Central and Eastern Europe would take down at least half a dozen European banks. Latvia would play the role of a Lehman, or, even more ominously, that of the infamous Austrian Kreditanstalt in the financial crisis of 1931, the failure of which had precipitated Weimar Germany’s final slide toward disaster.

For the IMF, the standard prescription for a country in Latvia’s position was a one-off devaluation followed by debt restructuring or rescheduling. But the European Commission dug in its heels. Latvia was en route to eurozone membership. It must stay the course. If it needed to rebalance its current account it must do so through deflation and austerity. The results for Latvia were drastic. By the summer of 2009 house prices had plunged by 50 percent. Civil servants, including one-third of the country’s teachers, were fired and public salaries were slashed by 35 percent. Unemployment surged from 5 to 20 percent. 53 Remarkably, Latvia clung on, as did its neighbors. In mounting its defense, Latvia received aid totaling 32 percent of its precrisis GDP: 3.1 billion euros came from the European Commission; the IMF provided 1.7 billion; 0.8 billion came from the World Bank and the European Bank for Reconstruction and Development; and 1.9 billion came from Sweden, Denmark, Finland, Norway and Estonia. 54 They all preferred to fight the crisis in Latvia rather than bailing out their banks at home. Significantly, the ECB absented itself from the crisis-fighting coalition.

The financial austerity course imposed a huge pressure on the new democracies of the Baltics. 55 In Latvia popular discontent with the new austerity line and accusations of corruption against the political class led to two referenda calling for protection of pensions and a public right to dissolve the parliament by plebiscite. In January 2009 Riga was rocked by mass protests that escalated into rioting and a night of street battles with police. In February a conservative coalition government took office under the high-profile member of the European Parliament Valdis Dombrovskis. His government’s objective was to stay the course of austere conformity. “We are facing national bankruptcy. It’s going to be tough,” 56 Dombrovskis told the nation. What, after all, was the alternative? The legacy of the Soviet period hung over Latvia. Georgia was a reminder. For the Baltics the choice was between a Western or an Eastern hegemon. Since the 1990s they had managed miraculously to navigate their way under the umbrella of the EU and NATO. At least as far as the Latvian political class was concerned, they intended to stay there.

IV

Faced with the double crisis of 2008 the reaction of Eastern Europe was not uniform. The Baltics stayed the course. Hungarian nationalism rebelled. But nowhere was the double shock more jarring than in Ukraine. The coincidence of the escalation of geopolitical tension between Russia and the West with the financial crisis dealt a shuddering blow to its fragile polity. The route to the Ukraine crisis of 2013 was twisted. But the path that it would travel down was mapped out already five years earlier.

In the spring of 2008 the decision by Ukrainian president Viktor Yushchenko to apply for NATO membership—eagerly applauded by the Bush administration, Poland and the other East Europeans—split Ukrainian politics. Whereas President Yushchenko threw in his lot with the West, Prime Minister Yulia Tymoshenko favored the policy of balance between Russia and the West that Kiev had pursued since independence and that had made her personal fortune as a kingpin in the gas trade. The war in Georgia in August 2008 divided what was left of the political legacy of the revolution of 2004. 57 Then, before the cease-fire in the Caucasus had more than a few weeks to settle, Kiev was rocked by the financial crisis.

Since the 2004 revolution, Ukraine’s economic growth had come to rely on foreign borrowing. By early 2008, foreign funds made up 45 percent of all corporate financing and 65 percent of household loans in Ukraine. 58 Altogether, European banks had lent Ukraine at least $40 billion, with Austrian and French banks responsible for almost half. The onset of the crisis stopped the credit flow. And it hit Ukraine’s exports hard. As one of the legacies of the Soviet era, steel accounted for 42 percent of Ukraine’s foreign currency earnings. No sector was worse hit by the crash in global investment spending than steel. Prices plunged and industrial output by January 2009 was falling at an annualized rate of 34 percent. 59 As Ukraine’s economy slid into recession, millions were left without pay, if they were not actually thrown out of work. Of all economies in the world, only Latvia would suffer a more severe contraction.

In October 2008 Ukraine had no option but to follow Hungary to the IMF. Kiev signed up to a $16.4 billion loan package. The IMF’s approach was not demanding by its usual standards. It asked for Ukraine to fully fund its budget, to set a realistic exchange rate and to ensure that its financial system was stable. But even this was more than Kiev could manage. The exchange rate was allowed to devalue from the overvalued rate of 5 hryvnia to the dollar to 7.7, though unofficially it traded as low as 10 to the dollar. The tax increases and subsidy cuts necessary to balance the budget were ruinously unpopular. 60 Asked in 2009, “Who bears the most responsibility for the difficult socioeconomic situation in Ukraine?” 69 percent blamed the heroes of 2004, with 47 percent singling out Yushchenko and 22 percent naming Tymoshenko. Yushchenko’s personal approval rating hovered between 2.5 and 5 percent. 61 The upshot was paradoxical. On the one hand, the impasse in Ukraine’s post–cold war development was more evident than ever. What hope there was of economic development lay in further integration with the West even at the expense of painful structural adjustment. On the other hand, by the autumn of 2009 the most popular politician in Ukraine was Viktor Yanukovych, the representative of the Russian-oriented “party of the regions” with its base in eastern Ukraine, the thuggish dinosaur of the transition era whose rigged election victory in 2004 had triggered the Orange Revolution.

The one point of relief for Ukraine in 2009 was that geopolitical tension between East and West seemed to be subsiding. With Medvedev in the Kremlin, the West scrambled to “reset” relations with Russia. But the fragility of the situation was painfully exposed in January 2009 when a dispute between Russia and Ukraine over unpaid bills and gas prices left Ukraine without heat in the depth of winter and interrupted flow through the pipelines running west to Europe. 62 The dispute was resolved only with EU mediation and a price increase for Gazprom that would become an albatross around the neck of Prime Minister Tymoshenko. Though Ukraine was far from being headline news, it was already in 2008–2009 drifting into an explosive state. As Austrian foreign minister Josef Proell presciently remarked in February 2009: “Ukraine is a very important keystone country and we must avoid a domino effect inside the EU, if there is economic and political catastrophe in such a huge neighbouring country. . . . We don’t see this scenario developing now. But we must prepare and keep an eye on Ukraine.” 63

Chapter 10

THE WIND FROM THE EAST: CHINA

I f the immediate impact of the financial crisis was to impose an uneasy truce on the old battlefields of the European cold war, the shocking realization of 2008 was how far both sides were willing to go. In Moscow, NATO’s heedless attempt at expansion and the clash with Georgia would not be forgotten. Russia had made good on Putin’s announcement at Munich that the unipolar moment was passing. And the Americans knew it was true. But when they thought of multipolarity, they did not think first and foremost of Putin’s ramshackle regime. They thought of China. And so, in fact, did Russia’s own best analysts. 1 The possibility of a Sino-American crisis was obvious to both sides. And the unexpected storm in the North Atlantic financial system further heightened tension. 2 But Beijing and Washington avoided disaster. Neither side wanted to take the kinds of risks that produced the violent clash in the Caucasus.

In 2008 Chinese opinion was alarmed to discover that their prized portfolio of dollar assets contained not just actual Treasurys but GSE debt, issued to finance the expansion of American mortgage lending. As in Russia, public opinion in China was indignant. Why was poor China financing America’s excess? As a sign of its impatience, Beijing allowed its spokesmen to make dramatic and unusually frank statements. If the United States allowed the GSE to fail it would be a “catastrophe,” China let it be known. 3 Toward the end of 2008 the Atlantic magazine garnered an interview with a fast-talking manager of China’s sovereign wealth fund. 4 The result was a startling insight into a topsy-turvy world. Over recent months, Gao Xiqing remarked, the world had watched as America, “after months and months of struggling with your own ideology, with your own pride, your self-righteousness,” had finally applied “one of the great gifts of Americans, which is that you’re pragmatic.” The Fed and the Treasury had intervened on a massive scale to stabilize the financial economy, so now, Gao quipped, when the Chinese looked to the United States, what they saw was not capitalist democracy, but “socialism with American characteristics.”

Cutting though it might have been, Gao’s analysis was not Marxist enough. It hadn’t been only ideology and vanity that stood in the way of a solution in September and October 2008. Interests had been at stake. Convening the “executive committee of the bourgeoisie” was never going to be a simple task. But, then, Gao was not a party theorist. He was an alumnus of Duke Law School and sported a CV including time spent working for Richard Nixon’s Wall Street law firm. But with or without the theory, his sense of the shifting balance of power was acute. “This generation of Americans is so used to your supremacy. Your being treated nicely by everyone. It hurts to think, Okay, now we have to be on equal footing to other people. ‘On equal footing’ would necessarily mean that sometimes you have to stoop to appear to be humble to other people. . . . The simple truth today is that your economy is built on the global economy. And it’s built on the support, the gratuitous support, of a lot of countries. So why don’t you come over and . . . I won’t say kowtow [with a laugh], but at least, be nice to the countries that lend you money. Talk to the Chinese! Talk to the Middle Easterners! And pull your troops back!”

As Barack Obama’s stunning election victory demonstrated, many Americans agreed with Gao. And, in fact, the outgoing Bush administration was doing its very best to be “nice.” What the Chinese really wanted was a total government guarantee for Fannie Mae and Freddie Mac debt. That would have had truly dramatic implications for the US government fiscal position, adding more than $5 trillion to the public debt at a stroke. Fannie Mae had been privatized during the Vietnam War for a reason. But in taking the GSE into conservatorship, Treasury Secretary Paulson did the next best thing. Even if it outraged the right wing of the Republican Party, the managerial elite knew that it was essential. Nor was President Bush too proud to phone Beijing to deliver the message personally. 5

The Chinese cut back their GSE holdings but they did not offload them like Russia, they merely reduced them to their level in the summer of 2007 before Gao and his colleagues had embarked on their ill-advised program of reserve diversification. Chinese purchases of Treasurys, meanwhile, increased. China’s total holding of US securities continued to rise from $922 billion in June 2007 to $1,464 billion two years later. 6 Nor was this surprising. Panic and crisis, turned US Treasurys into the most desirable asset in the world. Everyone wanted safety. Treasury prices were rising, yields soaring, so too was the dollar. If China had wanted to diversify out of its dollar assets, this was the moment to do it. There was insatiable global demand for safe dollar assets. But what the crisis revealed was that China’s options were limited. What other safe assets were there to buy? For China to have bought Japanese bonds would have created an entanglement that was potentially even more explosive. European bond markets weren’t deep enough. China and America were locked together willy-nilly. Their interdependence was structurally conditioned and this went not only for foreign investments, but for trade too.

I

Given the scale of Chinese export success and its accumulation of foreign assets, Western observers are apt to believe that China’s growth must be “export dependent.” But this is an optical illusion that reflects our recalcitrant Western-centric view. Exports are important to China, and its insertion into the world economy has transformed global trade. But even before the crisis China’s domestic economy was large and it was growing extraordinarily rapidly, far more rapidly than China’s markets abroad. China had made itself into an export champion, but in so doing it had also fostered imports—of commodities and components from Australasia, the Middle East, Africa, the rest of Asia and Latin America, as well as technology and advanced machinery from the West. A large part of the value in China’s world-beating exports was accounted for by imported raw materials and subcomponents. As a result, net exports accounted for a smaller share of Chinese GDP growth before 2008 than one might imagine. In fact, no more than one third of China’s growth from 1990 was driven by exports, with two thirds coming from domestic demand. 7 This was a very different balance from that of a truly export-dependent economy, of which Germany was the quintessential example. With slow domestic investment and consumption, the vast majority of Germany’s growth after 2000 was accounted for by foreign demand. In China, far and away the main driver of growth was its enormous wave of domestic investment. As China’s cities expanded and its infrastructure modernized at a staggering rate, the physical reconstruction of the country sucked the entire Chinese economy up with it.

By 2008 the immense dynamism of China’s domestic demand and its central position as a regional trading hub in East Asia suggested to some analysts that Asia might be on the point of “decoupling” from America and Europe. 8 In the spring of 2008, as the rest of the world slid toward recession, Beijing’s main worry was that China’s economy was expanding too fast. Growth in consumption was roaring along at more than 20 percent per annum. The People’s Bank of China raised interest rates and government fiscal policy was tightened to choke off the boom. Meanwhile, China’s government machine was reorganized to concentrate responsibility for more balanced national growth in centralized superministries. 9 What no one reckoned with was the sheer force of the global trade collapse. Whereas in July 2008 Chinese exports were growing by 25 percent, imports by 30 percent and FDI by 65 percent per annum, six months later China’s exports were falling by 18 percent, imports by more than 40 percent and FDI by 30 percent. It was an astonishing switchback. Even if net exports normally accounted for only a third of China’s growth, the impact was severe. In the fall of 2008 South Korean and Taiwanese corporations suddenly began to shutter their Chinese operations. 10 At the same time, cash-hungry Western banks such as Bank of America, UBS and RBS sold up and pulled out. But these were pinpricks when compared with the impact of falling export orders on China’s labor market. As the winter of 2008–2009 approached, 30 percent of China’s gigantic annual surge of college graduates—5.6 million per annum—were unable to find work. The reserve army of tens of millions of rural migrants fared even worse. For the Mid-Autumn Festival in October 2008, 70 million returned to their homes in the provinces, of whom only 56 million made the trip back to the cities after the break. Of those, according to World Bank estimates, 11 million were without jobs. Altogether, at least 20 million, and perhaps as many as 36 million, Chinese workers were left idle. 11

Ever watchful for signs of domestic social unrest, Beijing knew that it had to react. Already on November 5 the State Council convened an emergency meeting to agree on a 4 trillion yuan ($586 billion) spending program. This amounted to a remarkable 12.5 percent of 2008 GDP. It was supplemental to existing investment plans and was to be disbursed by the end of 2010. It was the first truly large-scale fiscal response to the crisis worldwide. On Sunday, November 9, 2008, as the plan was revealed to the press, the State Council declared: “Over the past two months, the global financial crisis has been intensifying daily. . . . In expanding investment, we must be fast and heavy-handed.” 12 And the declaration by the State Council was given additional force by a party instruction, Central Document No. 18, which called for a “package plan to counter the global financial crisis.” The word used to refer to the crisis-fighting measures was the old Mao-era term jihua, or plan, rather than the newfangled word for softer government programs or initiatives, guihua , which had come into widespread currency since 2006. 13 Instructions to the press required reporting to “stay upbeat, to avoid panic and contribute to consumer confidence.” 14

In November 2008 fiscal policy was pushed in China with the kind of urgency that the West reserved for central bank initiatives and bank bailouts. It was Tim Geithner’s “maximum force” approach but applied to public spending rather than monetary policy. The National Development and Reform Commission, the lead agency for Chinese economic policy, called on local government to “make every second count.” Central Document No. 18 shocked the local party apparatus into action. In the words of a leading American analyst, Document No. 18 “added to the sense of urgency, communicating the sense that it was OK to overturn ordinary obstacles to spending the money.” Over the days that followed, across China, provincial party meetings were hurriedly convened to “seize the favorable opportunity created by expansionary fiscal policy and the ‘appropriately loose’ monetary policy,” as one Shandong committee declared. On the evening of November 11 in Wugong County in Shaanxi Province, a “County Leadership Small Group for Implementing Central Document No. 18” was convened, to make the most of “an extremely rare and precious opportunity.” The aim, the county leadership group declared, was to “concentrate our forces and act quickly, strengthen our links with the provincial and municipal authorities, and make sure that more keypoint investment projects come to our county. . . . Getting more project funding is our top current task.” Within a year this party-led mobilization got 50 percent of China’s stimulus projects under way.

Reconstruction following the terrible Sichuan earthquake of May 2008, which had left more than seventy thousand dead and millions homeless, provided one obvious focus of attention. In the aftermath there had been an upsurge of public criticism and popular activism criticizing the inadequacy of many of China’s public buildings and demanding redress. For the party’s local leaders, crash stimulus spending offered a chance to reassert their authority. 15 A wider programmatic frame was provided by the National Development and Reform Commission’s promise of “scientific developmentalism.” 16 Funds were to be concentrated in ten sectors, including health care, education (particularly in the relatively deprived and politically contested western regions of China), low-income housing on the edges of China’s gigantic new cities, environmental protection, technological innovation, superhighways, urban electrification, the coal distribution network and railways. The popularly minded leadership team of President Hu Jintao had opened discussions of health-care reform already in 2005 in the wake of the SARS crisis. Something needed to be done about the glaring disparities in health coverage between rural and urban areas. 17 After several years of debate, the economic emergency of 2008 swung the decision quite suddenly toward a system centered on central government spending. On April 7, 2009, Beijing announced that health insurance coverage would be extended from 30 to 90 percent of China’s population and that central funds would be allocated to pay for the construction of two thousand county hospitals and five thousand township-level clinical centers. It was the largest expansion in health-care provision in world history to date and it was “inextricably interwoven with the stimulus package.” Beijing was happy to approve spending on hospitals, clinics and public insurance subsidies “because concerns about short-run deficits” had “evaporated. . . . The economic crisis . . . opened a window in which a more aggressive fiscal approach to social policy has become possible.” 18

The gigantic surge in stimulus spending also paid for what is perhaps the most spectacular infrastructure project of the last generation anywhere in the world, the construction of China’s high-speed rail network (HSR). In the first phase of Chinese growth, priority had been given to motorization and highway construction. Now rail came to the fore. After “borrowing” technology from the pioneers of HSR—Japan, Germany and France—China embarked on a program that dwarfed all previous efforts. Between 2008 and 2014 the network of rail lines suitable for traffic at speeds of 250 kilometers per hour or more was expanded from 1,000 kilometers to 11,000 kilometers. Journey times from Beijing to Shanghai were cut to 4.5 hours for an 819-mile trip, compared with the 7 hours that the Acela—the pride of America’s Amtrak—takes to cover the 454 miles from Boston to Washington, DC. Not only did China pioneer ultrafast trains capable of cruising at 360 kilometers per hour. The economies of scale opened up by the gigantic construction program also made China into the technological leader in rail-line and viaduct construction. 19 Gigantic snail-like machines would lay the track in a continuous length, mile after mile, across endless arrays of standardized, prefabricated concrete pillars. According to World Bank estimates, even allowing for lower labor and land costs, China’s costs of construction were a fraction of those in Europe and North America.

Following the spectacular 2008 Olympics, the promptness and scale of China’s fiscal stimulus was further proof of the mobilizing capacity of the Communist regime. Compared with the sluggishness of many Western states, it is hard to avoid invidious comparisons. Both as presidential candidate and newly inaugurated president, Barack Obama referred frequently to China’s great strides in infrastructure. 20 But this well-deserved credit should not obscure the tensions that lurked beneath the surface. In China the stimulus was deeply controversial. To many observers it seemed that, driven by a crisis in the West, the Chinese economy was being sucked in precisely the wrong direction. Was the stimulus a spectacular demonstration of state power, or further proof of the addiction of the Chinese power elite to an unsustainable growth model? 21

II

China’s growth rate was the envy of the world. But at home, given the huge social and environmental costs, reviews were more mixed. The aim of the Hu Jintao leadership when it took office in November 2002 had been to give new priority to consumption and the household standard of living. After a decade of superrapid growth, the Chinese had had enough of heavy industrial development. 22 But investment-driven heavy industrial growth is a hard habit to break. Five years later, in March 2007, in a remarkably frank assessment delivered to the National People’s Congress, Premier Wen Jiabao warned that “the biggest problem with China’s economy” was still that growth was “unstable, unbalanced, uncoordinated, and unsustainable.” 23 When announcing its stimulus response to the 2008 crisis, Beijing pushed high-tech railways and health care as hard as it did because it wanted to escape associations with clichés of heavy industrial growth. The government was determined to avoid “frivolous or speculative investments.” “There won’t be a penny spent on enlarging mass production, or highly polluting and resource intensive sectors,” Zhang Ping, director of the National Reform and Development Commission, stressed. All its efforts would be directed so as to “target spheres that would promote and consolidate the expansion of consumer credit.” 24 In December 2008 the State Council followed the November stimulus announcement with an “Opinion on Stimulating Circulation and Expanding Consumption,” itemizing twenty measures to boost consumption. China’s 220 million rural households were offered state-funded discounts on the purchase of two large household appliances, such as televisions, air conditioners, washing machines and refrigerators. 25 As the average rural household earned less than 16,000 renminbi (RMB—though used interchangeably with yuan, RMB refers to the Chinese currency as such, whereas yuan are the units in which sums are measured) in 2008, buying a computer or color TV for 7,000 RMB was a big step. But over a two- to three-year time horizon, the 140 billion RMB promised by Beijing was a powerful inducement. 26

The aims of China’s leadership were thus clear. And it is tempting to imagine these priorities being rolled out across the country by an all-powerful one-party state. But in practice, Chinese central government is stretched thinly across the giant bulk and complexity of the world’s most populous nation. Though responsibility for revenue collection falls heavily on central government, government expenditure directly controlled from Beijing has amounted to no more than 4 to 5 percent of GDP since the 1990s, a very small figure by comparison with its American or European counterparts. In China, 80 percent of government spending is done at the regional and local levels, where expenditure has surged between 1994 and 2008 from 8 to 18 percent of GDP, even as China’s national income quintupled. 27 The regime thus operates through decentralization and indirect mechanisms, which amplify its power and extend its reach, but also distort and distend Beijing’s intentions.

Of the 4 trillion yuan stimulus announced by the center in November 2008, only 1.18 trillion yuan would be delivered directly from central funds. The rest were to come from local government, a ratio of 1:3, corresponding roughly to the general balance between central and local expenditure. It was the decentralized nature of the state apparatus that made the mobilization of the Communist Party and its nationwide apparatus so vital. Central Document No. 18 energized the networks that linked the Communist Party, local government and business interests. It was precisely this nexus that over the last generation had combined to supercharge China’s spectacular economic growth. But it was that same combination that also went a long way to explaining the lopsided character of China’s growth. To meet a central target or quota, there was always some regional highway connection, housing complex, bridge or industrial park to be built and profits to be made doing so. When the stimulus was launched it was precisely this chain reaction that worried those who advocated a more balanced model of growth. The centrally ordained stimulus would unleash the bulldozers of the infrastructure machine. The results confirmed the critics’ worst fears. In Hubei province, with a population of 57 million and a regional GDP of $225 billion in 2009, there were projects under construction by 2010 notionally costed at $363 billion. 28 A further $390 billion and $450 billion were planned for 2011 and 2012. Taken at face value, this meant that a single Chinese province with a population the size of the UK and a GDP the size of Greece was engaging in a program of investment larger than any stimulus ever attempted in the United States. Across China, within a month of the State Council’s November initiative, eighteen provinces had proposed projects with a total budget of 25 trillion RMB, six times greater than the original proposed stimulus, accounting for more than 80 percent of Chinese GDP. 29 Not only was this proposed spending gargantuan, but within the corporate sector, it was the State Owned Enterprises (SOE) that took charge. Since the 1990s the thrust of central policy had been to shed labor and to streamline these vehicles of Communist economic development policy. 30 Now, under the sign of the stimulus, the SOEs lurched once more to the forefront of Chinese growth.

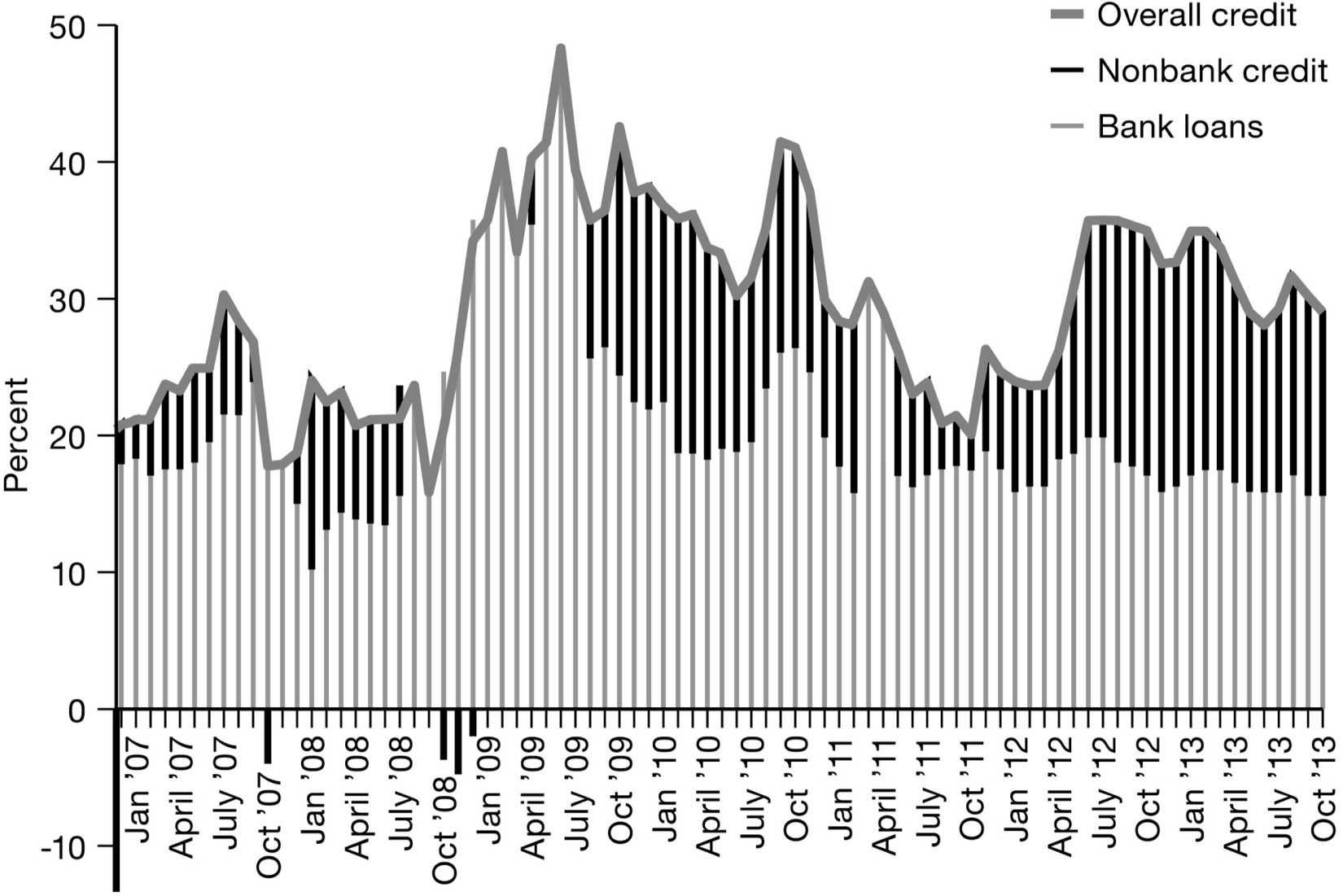

China’s Credit Stimulus, 2007-2013 (year-on-year growth rate)

Source: Yukon Huang and Canyon Bosler, “China’s Debt Dilemma,” 2014, figure 1, http://carnegieendowment.org/2014/09/18/china-s-debt-dilemma-deleveraging-while-generating-growth-pub-56579 . Data: UBS.

Clearly the impetus for spending was massive. But from an economic point of view the vital question was how it was to be financed. This is the key question in any fiscal policy “stimulus.” If spending is paid for by tax increases, this negates any increase in purchasing power. Borrowing by issuing bonds will soak up private savings, which may divert the portfolios of private wealth holders away from other investments. Credit creation is the one surefire way to fund stimulus spending if the aim is immediately to revive an underemployed economy. Beijing’s stimulus was particularly effective precisely because it combined huge government spending with a spectacular loosening of monetary policy.

In China, not only were many major industrial firms state controlled but the banking sector was under the direct influence of the central bank as well. 31 When it wants to control credit, the People’s Bank of China (PBoC) not only sets the interest rates. It set quotas for credit issuance for each of the major banks. To further manipulate the credit flow it can use higher or lower reserve ratios and greater degrees of “sterilization” of its foreign exchange interventions. All of these mechanisms were once commonplace in the West as well, legacies of the World War II era. But from the 1970s onward, direct regulation of bank credit was progressively abandoned in the West. In facing the 2008 crisis these tools of banking control gave Beijing remarkable leverage. In September and November of 2008 the PBoC reversed its tightening of the spring by slashing its interest rate by almost 5 percent. Then it announced that for 2009 it was doubling the banks’ lending target from 4.7 trillion RMB to 10 trillion RMB. Reserve ratios were cut by up to 25 percent for smaller banks. It was, as the PBoC’s Monetary Policy Committee declared in April 2009, an “appropriately loose monetary policy” to sustain the priorities of the stimulus. 32

The banks responded. The Bank of China alone wrote 1 trillion yuan of loans in the first half of 2009, with the Agricultural Bank of China, China Construction Bank and the Industrial and Commercial Bank of China not far behind. Together in the first quarter of 2009 credit issuance came to 4.6 trillion yuan, with the top four being responsible for 3.433 trillion yuan. More new credit was issued in three months than the official fiscal stimulus would provide for the next two years. Meanwhile, provincial and city governments were enjoined to work with local banks. The main mechanism for financing their local spending were so-called city investment companies, or local government financing vehicles—the “shock troops of the stimulus.” These SPVs were endowed with parcels of municipal land against which they borrowed to fund development projects. 33 Between 2008 and 2010 local government debt would rocket from 1 trillion RMB ($146 billion) to an estimated 10 trillion RMB ($1.7 trillion). 34

At the height of the stimulus drive, in the first half of 2009, 7.37 trillion RMB were issued in new loans. This was a 50 percent increase on the year before, which had also been a year of booming economic activity. By the end of the year the total volume of lending hit 9.6 trillion yuan. 35 If we add the government deficit at all levels to the growth in bank credit beyond the 15 percent per annum expansion that had been the norm in China over the previous years, we get a measure of the true scale of China’s stimulus. In 2009 its dimensions were extraordinary—950 billion yuan in deficit, 467 billion in additional bond finance and 5 trillion in bank loans beyond the previous growth norm, for a total stimulus of 6,487 billion RMB, or 19.3 percent of GDP. 36

Big Bang: China’s Bank Lending and Fiscal Stimulus Programs, 2008–2010

|

Stimulus (RMB billions) |

2008 |

2009 |

2010 |

|

Fiscal deficit |

111 |

950 |

650 |

|

Net new bank loans |

252 |

5070 |

1936 |

|

Net new bond finance |

251 |

467 |

-232 |

|

Total |

614 |

6487 |

2354 |

|

Stimulus (% GDP) |

|||

|

Fiscal deficit |

0.4% |

2.8% |

1.6% |

|

Net new bank loans |

0.8% |

15.1% |

4.9% |

|

Net new bond finance |

0.8% |

1.4% |

-0.6% |

|

Total |

2.0% |

19.3% |

5.9% |

Source: C. Wong, “The Fiscal Stimulus Program and Problems of Macroeconomic Management in China,” (2011), table 4, https://ora.ox.ac.uk/objects/uuid:4b8af91e-89c7-4a25-be7c-2394cd3c4e9b . Data: China Data Online.

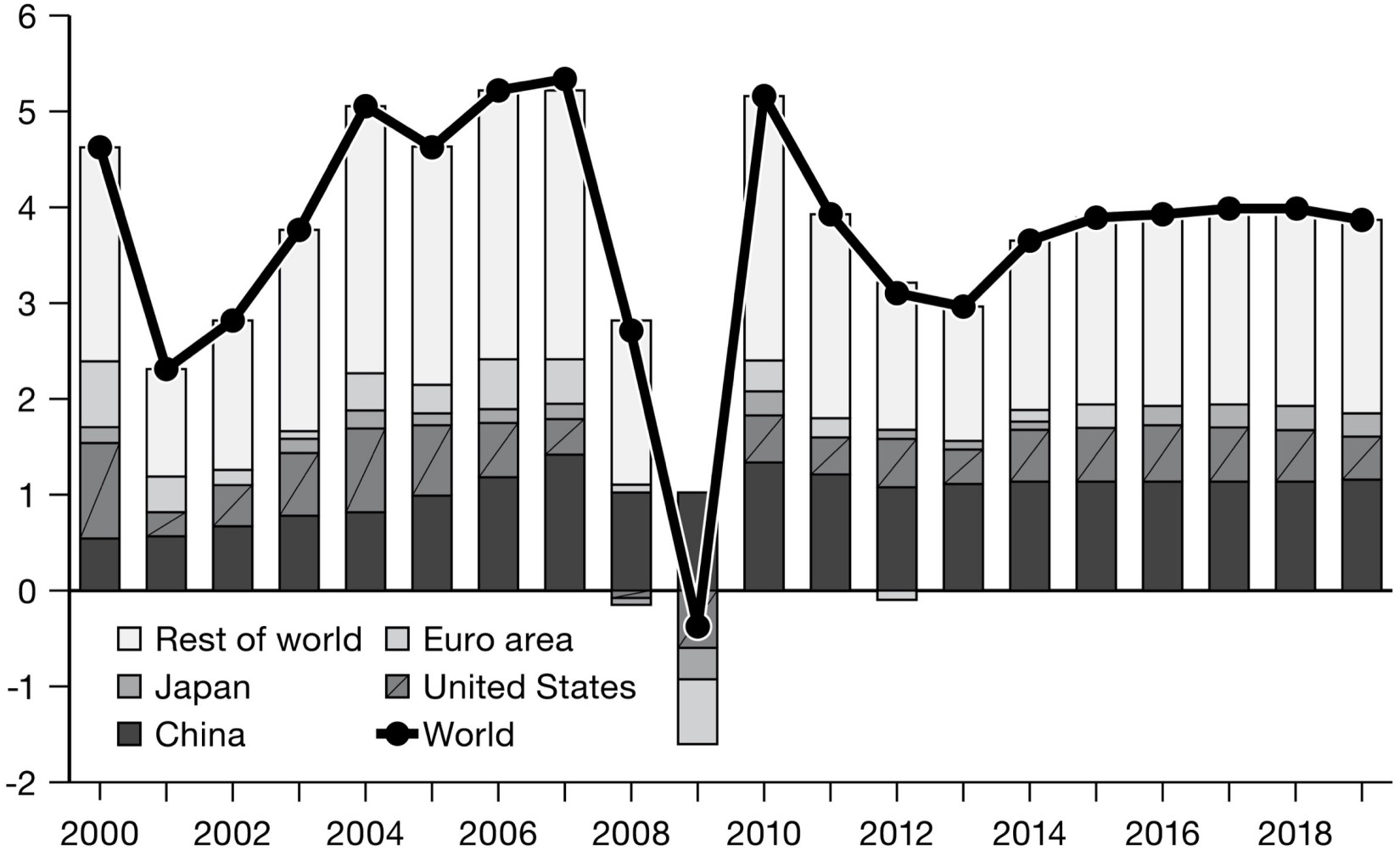

This huge additional growth boost was delivered through a variety of channels. But it was state directed from the top down and supplemental to China’s already enormous growth rate. When the entire complex is accounted for, this was an intervention comparable in scale to anything ever undertaken in the Mao era, or under Soviet communism. The Western capitalist economies had witnessed such huge mobilizations only in times of war. The rate of investment in the Chinese economy surged toward 50 percent of GDP, a level rarely, if ever, seen before. It was enough to offset even the worst shock to global trade. 37 At 9.1 percent, China’s growth rate in 2009 was barely lower than it had been in 2008 and vastly higher than anywhere else in the world. And given the size to which the Chinese economy had expanded, this was decisive. In 2009, for the first time in the modern era, it was the movement of the Chinese economy that carried the entire world economy. Together with the huge liquidity stimulus delivered by the US Federal Reserve, China’s combined fiscal and financial stimulus was the main force counteracting the global crisis. Though they were not coordinated policies, they made real the vision of a G2: China and America leading the world.

Drivers of World Growth (in percentage points)

Source: S. Barnett, “China: Size Matters,” IMF (blog), https://blogs.imf.org/2014/03/26/china-size-matters/ .

III

Given the geopolitical conclusions that are apt to be drawn from China’s “overtaking” of the United States, it is worth noting that the 2008 mobilization was not part of any master plan. It was a hyperactive response to an unforeseen emergency that struck China from the outside. The origin of that negative shock was in the West. It unleashed forces within China that took its economy in directions that the Beijing leadership had been struggling to counteract and that were widely unpopular in China. And the dramatic impact of the stimulus had consequences that were political and geopolitical as well as economic.

The spectacular state action fit well within popular narratives of China’s rise. As the twenty-first century began Chinese audiences were hooked on a massive diet of TV and film offerings preoccupied with the question of the rise and fall of great powers. 38 On the Internet there was a spectacular surge in public discussion of “Chinese greatness” and the “China model.” 39 In the wider world, surveys conducted by the authoritative US polling center the Pew Charitable Trusts registered a dramatic shift in popular understanding of the global center of gravity. As the impact of the economic crisis sank in, the number of respondents identifying the United States as the dominant economy in the world began to decline sharply. By 2010 pluralities of respondents in both the United States and Europe would identify China as the “world’s leading economy.” 40 In material terms it empowered the Communist Party and the growth coalitions built around it. Because of the decentralized nature of power, those coalitions came in different colorations, ranging from Shanghai’s hypermodernity to the neo-Maoism of Bo Xilai’s “Chongqing Model.” What was striking, however, was that these were overwhelmingly civilian coalitions. Unlike other historical examples of great growth spurts, China’s stimulus was not a military-industrial push.

Unlike subordinate parts of America’s global network, like Japan or Germany, for instance, China had a conventional view of national power. It took for granted that national autonomy implied autonomy in security policy. Given China’s booming economy, spending on defense increased with spending on everything else. Already in 1999 the military-industrial complex had been restructured to increase competition. In 2005–2006 the Chinese military formulated a major technological modernization program. 41 But this was merely a recognition of how far China lagged behind. The army was oversized and underpowered in technological terms. A society entering into mass affluence as rapidly as China was doing does not offer a congenial habitat for the underpaid profession of soldiering. Rather than raw recruits, the Chinese military needed technologists, but they were scarce and expensive. China’s military equipment and infrastructure were far behind those of Western militaries and behind the standard set by China’s booming business sector. And though it was increasing rapidly in absolute terms, as a share of GDP, China’s military spending remained flat at 2 percent throughout the crisis—half the level that the United States had sustained since 9/11. As the civilian-centered stimulus program hit in 2008–2009, the share of military expenditure in total public spending halved from 12 to 6 percent. 42

These facts were public knowledge, but Washington’s seismograph reacts sensitively to any challenge. When in March 2009 a flotilla of Chinese trawlers harassed an American naval reconnaissance vessel off Hainan island, the incident was promptly declared to be a sign of escalating confrontation. 43 The Obama administration’s first encounters with the Chinese were frosty. Treasury Secretary Geithner provoked laughter from nationalist students at Peking University when he declared that American debt was “very safe.” 44 As one American analyst remarked, “2009–2010 will be remembered as the years in which China became difficult for the world to deal with.” 45 Whether this reflected geopolitical ambition was not yet clear. But as far as strategists in Washington, DC, were concerned, this was incidental. 46 It was the economy itself that was decisive. Washington was convinced that China’s military potential would grow with time, as would its ambition. What underpinned both was its spectacular economic growth, and what was decisive was Beijing’s ability to control it. In this sense the financial crisis marked a moment of transition, as much on the Western side as in China itself. Given Beijing’s response to the crisis of 2008, its emergence as a decisive force in world affairs was undeniable. As was the other realization taught by 2008: If China was not export dependent, it was massively interdependent with the West. It had a measure of control but not insulation. Since the early 2000s, Washington’s ambition had been to develop China as a “responsible stakeholder” in the world economy. Now the question was reversed. In the wake of the crisis what Beijing needed to know was what to expect from America. As Gao remarked to the interviewer at the Atlantic : “Why don’t we get together and think about this? If China has $2 trillion [in US assets], Japan has almost $2 trillion, and Russia has some, and all the others, then—let’s throw away the ideological differences and think about what’s good for everyone. We can get all the relevant people together and think up what people are calling a second Bretton Woods system, like the first Bretton Woods convention did.” 47

Chapter 11

G20

C hina’s stimulus benefited all its trading partners, from Australia to Brazil. 1 Across the world the share of China trade increased. 2 But, having recognized the scale and significance of the Chinese effort, it is important not to fall into the trap of allowing it to overshadow everything else. If we replace a narrowly Western view with a one-eyed focus on China, we fail to grasp the drama and complexity of the transition to a truly multipolar world. Ten years on from the emerging market debt crises of 1997–1998, what was impressive about 2008 was the policy response across the emerging economies. At the UN General Assembly meeting in New York in September 2008 it was the Latin Americans who were the most vociferous. But in responding to the crisis, it was “emerging Asia” that set the pace.

I

In the summer of 1997 the Asian financial crisis had started in Thailand and had spread from there across Southeast Asia to Indonesia, Malaysia and Singapore, before ricocheting two thousand miles to the northeast to unleash havoc in South Korea. After a year of severe recession, by 2000 Thailand, Indonesia, Malaysia and Korea were all growing again. From a combined GDP in 1997 of $2.3 trillion in purchasing power parity (PPP) terms, by 2008 the output of these four economies had nearly doubled to $4.4 trillion. 3 This gave them a weight in the world economy comparable in PPP terms to France and Italy combined, or California plus Texas. In terms of economic policy, the East Asian economies were model students. Learning the lessons commonly prescribed after the crises of the 1990s, they adopted tight fiscal policies and built up huge currency reserves. Indonesia, where the 1998 crisis had triggered the fall of Suharto’s dictatorship, went so far as to adopt a fiscal straitjacket modeled on the EU’s Maastricht criteria. 4 Though this discipline was restrictive and particularly so for a developing economy in need of public investment, when the crisis struck in 2008, the regions of Southeast and East Asia had room to maneuver. 5 And they needed it. Though the crisis did not originate in Asia, they were acutely vulnerable to global shocks.

Most at risk in 2008 was South Korea, whose famous corporate export champions, the chaebol —Daewoo, Hyundai, Samsung—and their giant steel plants, shipyards and car factories suffered a shuddering blow. “We are collateral damage in a crisis that is not our doing,” observed one professor at Korea University in Seoul. “We live in an unfair world.” 6 But however real this sense of victimization, it does not capture the complex reality of South Korea’s situation. What set South Korea apart in Asia, and gave it a vulnerability akin to that of Eastern Europe or Russia, was the global integration of its financial system. 7 After the shock of the 1990s the South Korean central bank had made sure to accumulate ample foreign reserves—$240 billion by the summer of 2008. But this did not cancel out the vulnerabilities in the Korean financial system. Unlike in Europe, subprime wasn’t the issue. South Korean holding of toxic US mortgage securities amounted to only $850 million. 8 The problem was not on the asset, but on the funding, side of the balance sheet. Since the early 2000s, Seoul had promoted itself as a regional financial hub for Northeast Asia. It had liberalized currency and capital flows. A large part of South Korean banking was owned by foreign investors, and Korea’s banks had shifted to the unstable new model of wholesale funding, borrowing short term on global dollar markets to invest long term at higher interest rates in Korea. This was made all the more attractive by South Korea’s export success and the steady appreciation of the Korean won against the dollar. The problem for the chaebol was to hedge their dollar export earnings against devaluation. One way to do this was to borrow in dollars and invest in Korean assets, repaying the dollar loan at more favorable exchange rates in the future. 9 The trade was profitable if short-term dollar funding remained cheap and exchange rates continued to move as expected. By June 2008, as a result of this hedging tactic, South Korean businesses had $176 billion in short-term dollar loans outstanding, an increase of 150 percent since 2005. The banking sector owed $80 billion, which had to be rolled over by the summer of 2009.

When short-term dollar lending markets shut down across the world and the dollar surged, the logic of the won-dollar carry trade went abruptly into reverse. As Korean businesses scrambled to cover their dollar exposure, a disastrous cycle ensued. Preemptive buying of dollars led to an immediate collapse in the value of the won. When national currency holdings slid perilously close to the psychological threshold of $200 billion, that added to the panic. 10 Between the summer of 2008 and May 2009 the won plunged from 1,000 to 1,600 to the dollar, increasing the local cost of US dollar loans by 60 percent. Only tiny bankrupt Iceland suffered a more drastic depreciation. The cost for Korean borrowers of insuring dollar bonds against default (CDS premiums) surged from 20 basis points (0.2 percent of the value of the loan) in the summer of 2007 to 700 by October 2008. 11 Adding 7 percent to the interest burden of a bank bond ruled out further borrowing for the foreseeable future. Even banks with government backing, such as Woori, found themselves shut out of repo markets.