Chapter 6

“THE WORST FINANCIAL CRISIS IN GLOBAL HISTORY”

A merica’s real estate prices peaked in the summer of 2006 and began, slowly at first, to ease. In Ireland the turning point came in March 2007. By the summer construction sites began to close in Spain. October 2007 saw the first dip in UK house prices. Tens of millions of home owners now felt the force of asset valuation go into reverse gear. 1 As house prices fell, equity dwindled, and the hardest hit slid into negative equity. Families scrambled to slash spending and pay down credit card and other short-term debt. The result was a smothering recession in consumer demand. Whatever else happened, a large part of the North Atlantic economy was headed into a downturn. On the face of it, this was precisely the sort of contingency that financial engineering was supposed to deal with. Through securitization, risks were supposed to have been spread so that even severe losses would be absorbed across the broad base of the economy. That was the theory. By the late summer of 2007 it was evident that the reality was different. Though mortgage-backed securities had indeed been sold far and wide, lethal pockets of risk were concentrated in some of the most vulnerable nodes of the shadow banking system.

The first mortgage issuers to die were in the bottom tier. 2 The aptly named Ownit Mortgage Solutions, one of the feeders for Merrill Lynch’s securitization pipeline, was the first to go, on January 3, 2007. On February 8, 2007, the crisis moved up the food chain when HSBC, whose offices spanned Hong Kong, Shanghai and London, announced it was making a $10.6 billion provision for losses on mortgage investments. On March 7, Ben Bernanke was still in a sanguine mood, declaring that he thought the subprime problem was contained. But the bad news kept coming. In April New Century Financial, the largest stand-alone subprime lender, folded. May saw Swiss megabank UBS announce that it was closing its Dillon Read Capital Management hedge fund. 3 On June 22, Bear Stearns was forced to bail out two funds that had made heavy losses on MBS. By then it was clear that the foundations were shaking. It was in the late summer that the full scale of the financial fallout began to become clear. On July 29, 2007, the small German lender IKB had to be bailed out by a consortium of banks with public backing. 4 On August 8, 2007, another of Germany’s overextended regional banks, WestLB, announced outsized losses on a real estate fund and stopped payouts. Within days it was followed by Sachsen LB. But the really decisive break in market confidence came on the morning of August 9, 2007, when BNP Paribas, France’s most prominent bank, announced that it was freezing three of its funds. 5 The explanation Paribas offered marked a decisive moment in the opening of the crisis: “The complete evaporation of liquidity in certain market segments of the U.S. securitisation market has made it impossible to value certain assets fairly regardless of their quality or credit rating.” 6 Without valuation the assets could not be used as collateral. Without collateral there was no funding. And if there was no funding all the banks were in trouble, no matter how large their exposure to real estate. In a general liquidity freeze, the equivalent of a giant bank run, no bank was safe. As the implications of the announcement from Paris sank in, around noon Central European Time on August 9, 2007, the cost of borrowing on European interbank markets surged. 7 As one senior bank executive commented, the event was disorientating: “It was something none of us had experienced. It was as if your entire life you had turned the spigot and water came out. And now there was no water.” 8

The ECB did not at this point have data on the subprime exposure of Europe’s banks. But the stress in the interbank lending market was all too obvious. In response Jean-Claude Trichet and his colleagues opened the liquidity tap, offering funds at attractive rates in unlimited quantities. By the end of the day on August 9, Europe’s banks had taken 94.8 billion euros, and they took another 50 billion on August 10. It was the scale and urgency of this action that finally brought home to Ben Bernanke and Hank Paulson the true severity of the situation. As Larry Elliott, economics editor of the Guardian, commented: “As far as the financial markets are concerned, August 9 2007 has all the resonance of August 4 1914. It marks the cut-off point between ‘an Edwardian summer’ of prosperity and tranquility and the trench warfare of the credit crunch—the failed banks, the petrified markets, the property markets blown to pieces by a shortage of credit.” 9 Quite how bad things were soon going to get was suggested three weeks later, when on September 14, Northern Rock, one of Britain’s largest mortgage lenders, failed. On TV screens, the Northern Rock panic looked like a classic bank run. Anxious depositors queued up outside beleaguered bank branches to retrieve their funds. News photographers and camera crews had a field day. But off camera something even worse was happening. The trillion-dollar global funding market was shutting down. 10

I

Northern Rock was a product of Britain’s overheated housing bubble. Formed in the 1960s through amalgamation of two nineteenth-century building societies (thrifts) and headquartered in gritty Newcastle, it had by the 1990s acquired fifty-three competitors across the north of England. To create the platform for further growth in October 1997, it converted from thrift status to a public limited company and floated on the London Stock Exchange. Then, between 1998 and 2007, in a gigantic surge of growth, it quintupled its balance sheet. As house prices faltered, some of its more marginal loans were primed to go bad. It was no surprise that “the Rock” got into trouble. But the obviousness of this connection is deceptive. What triggered the collapse in 2007 were not the loans on its balance sheet but the mechanism of their funding. Northern Rock was the model of a modern highly leveraged bank: 80 percent of its funding was sourced not from deposits but wholesale, at the lowest rates global money markets would offer. The bank’s 2006 annual report gives an idea of this far-flung funding operation:

“During the year, we raised £3.2 billion medium term wholesale funds from a variety of globally spread sources, with specific emphasis on the US, Europe, Asia and Australia. This included two transactions sold to domestic US investors totalling US$3.5 billion. In January 2007, we raised a further US$2.0 billion under our US MTN [medium-term notes] programme. Key developments during 2006 included the establishment of an Australian debt programme, raising A$1.2 billion from our inaugural issue. This transaction was the largest debut deal in that market for a single A rated financial institution targeted at both domestic Australian investors and the Far East.” 11

Northern Rock had minimal exposure to US subprime. But that didn’t matter, because it sourced its funding from markets heavily used by banks that did. The bad news from Paribas on August 9 was enough to shut down the interbank lending markets and the market for asset-backed commercial paper. It was the seizure in the funding market that poleaxed the entire securitization business and in particular the European side, which had been most actively involved in the issuance of ABCP. Given Northern Rock’s extreme dependence on wholesale funding, it took only two working days after the markets dried up for the bank to notify the Financial Services Authority of an impending crisis. 12 But the Bank of England was in no mood to help. Governor Mervyn King took the view that the overextended mortgage lender should suffer the consequences of its irresponsible expansion. By the end of August Northern Rock’s liquidity problems had become life threatening. But it wasn’t until September 13, after the BBC reported the story and the government acted to address the crisis by announcing a guarantee, that the retail depositors panicked. After that, the main damage to Northern Rock’s balance sheet was done by online withdrawals. The elderly savers queuing in the streets made for alarming TV footage. But it was not their panic that was bringing down the bank. It was a bank run operating on an altogether different scale at the speed of computer terminals in money markets across the world. It was a bank run without deposit withdrawals. There had been no deposits. There was nothing to withdraw. For banks to find themselves a trillion dollars short, all that needed to happen was for major providers of funding to withdraw from the money markets.

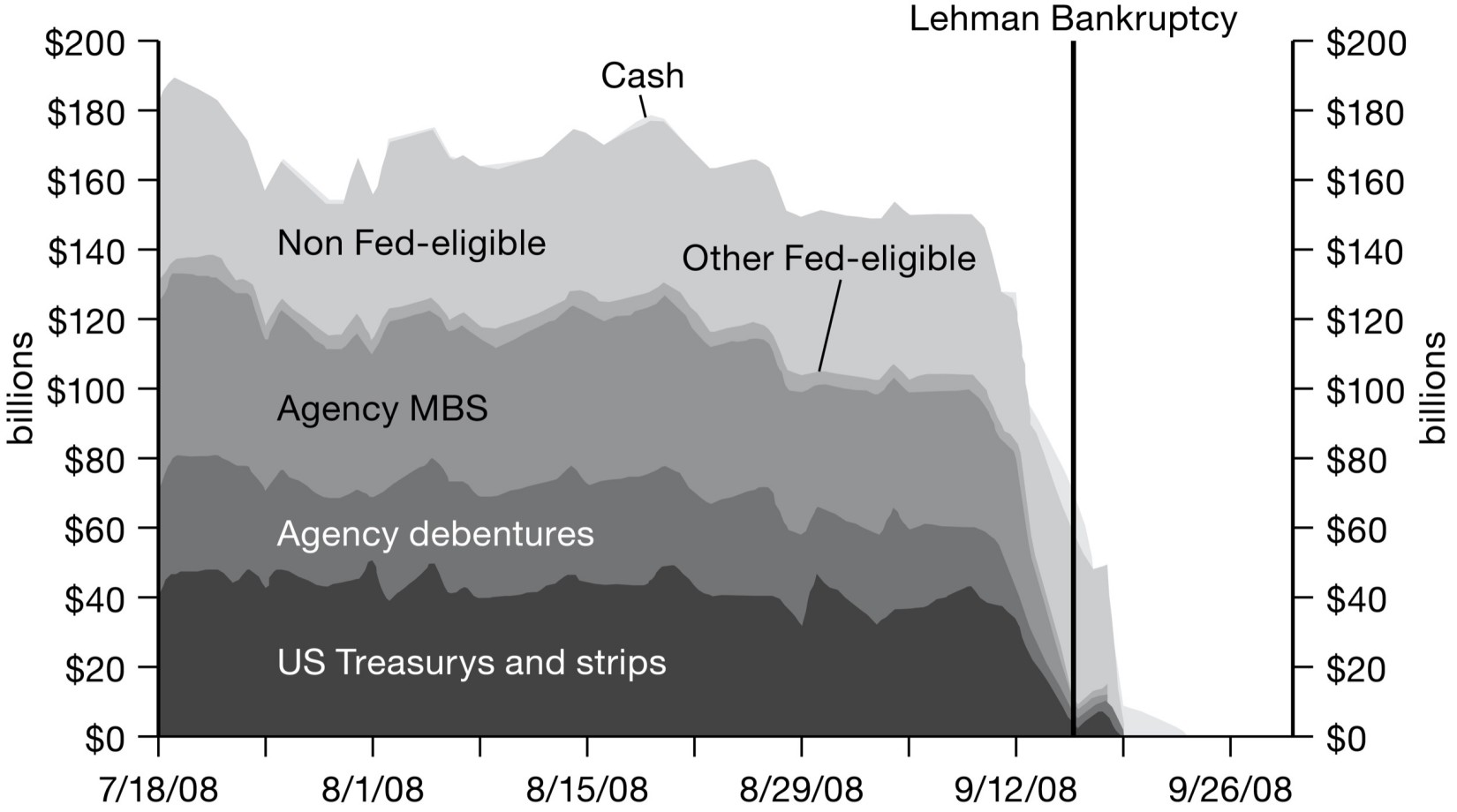

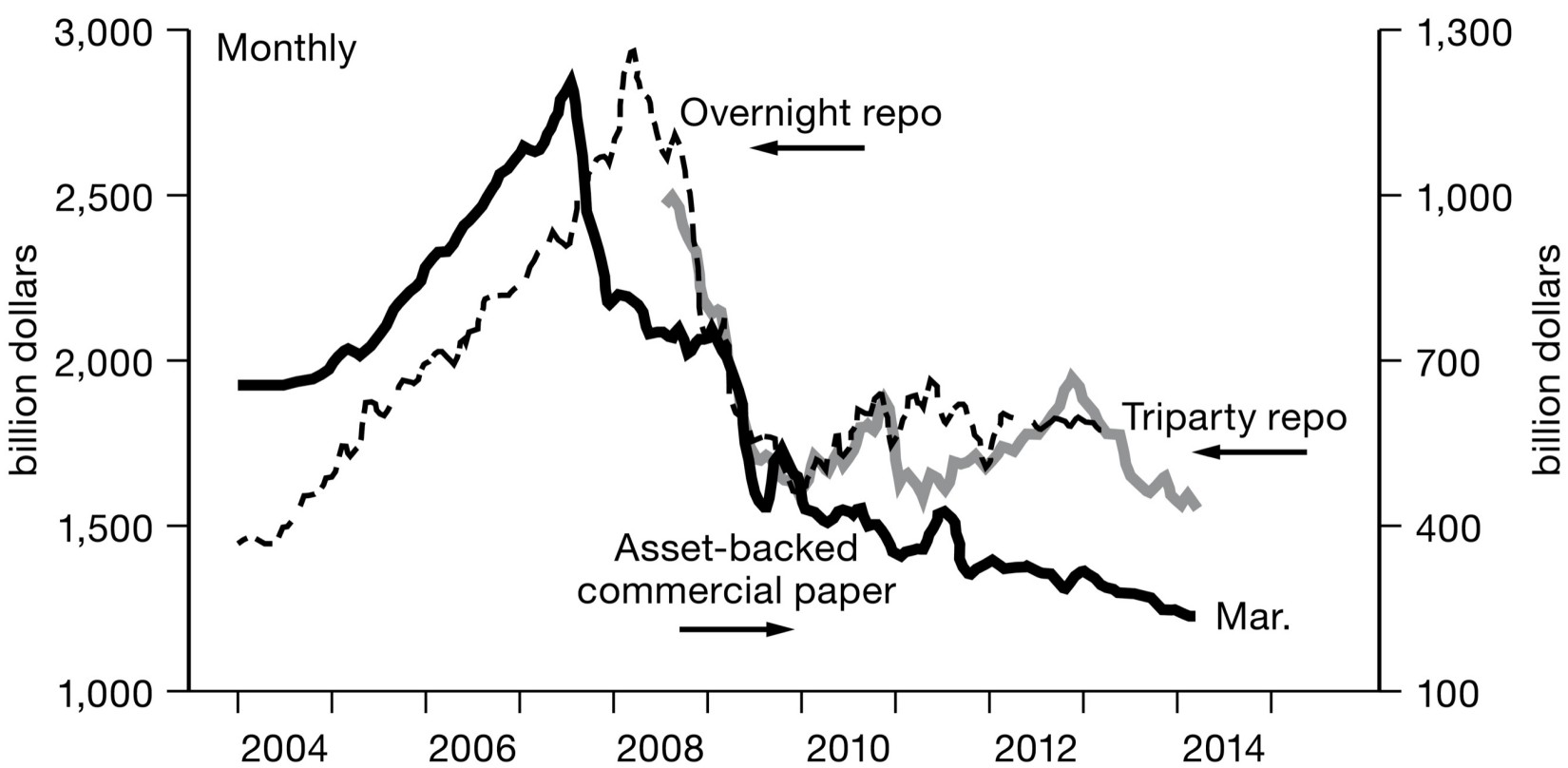

The Rise and Fall of Commercial Paper and Repo Financing, 2004–2014

Source: Tobias Adrian, Daniel Covitz and Nellie Liang, “Financial Stability Monitoring,” Annual Review of Financial Economics 7 (2015): 357–395, chart 15.

ABCP was always the weakest link in the shadow banking chain. Repo, as fully collateralized lending, was supposed to be safe. Initially, that expectation was borne out. Bear Stearns, the smallest of the US investment banks, reported the first loss in the firm’s history in the first quarter of 2007. 13 As was common knowledge, it was heavily involved in mortgage securitization. That was enough to restrict its access to commercial paper markets. The bank’s ABCP issuance plunged from $21 billion at the end of 2006 to $4 billion a year later. Initially, Bear was able to make up for this shortfall by increasing its repo funding from $69 billion to $102 billion. To back this up, as late as Monday, March 10, 2008, Bear still held an $18 billion “pool” of ultraliquid, high-quality securities. But then collateralized borrowing began to fail too.

Unlike the implosion of ABCP, the “run on repo” was a surprise. 14 Under British and American law, the holder of repo collateral is entitled to seize it ahead of any other claimant in the bankruptcy queue. So even allowing for Bear’s large portfolio of toxic mortgage-backed securities, its repo ought to have been good. A Treasury security is a Treasury security. Unfortunately for Bear, given that there were plenty of other counterparties to engage in repo trades with, no one wanted to take the risk of having to seize collateral from a failing bank, even if the collateral was as highly rated and as liquid as US Treasurys. When news of a new round of mortgage failures hit the markets in March 2008 and hedge funds began emptying their prime brokerage accounts, quite suddenly the haircuts Bear Stearns faced in the bilateral repo market steepened and access to trilateral repo funding was shut off. A bank that in early March had easily been able to raise $100 billion overnight in exchange for good collateral could no longer fund itself. On Thursday, March 13, with its liquidity reserve down to only $2 billion, Bear’s directors were told that $14 billion in repos would not “roll” the next day and that they were at imminent risk of running out of cash. This was a modern bank failure. There were no queuing depositors. Bear did not cater to pensioners. It died, because doubts about its business led it to be cut out of wholesale funding markets.

Then something even worse began to happen. The uncertainty spread from individual weak banks to the entire system. First in the spring of 2008 and then in June, the haircuts on bilateral repo took a severe step up across the board, for all asset classes, for all parties. 15 This meant that the amount of capital that was required to hold the outstanding stock of bonds leaped upward, across the entire banking system. Repo in US Treasurys and GSE-backed mortgage-backed securities was the least badly affected. As top-quality collateral they were reserved mainly for use in triparty repo overseen by JPMorgan Chase and Bank of New York Mellon. As long as a counterparty remained in good standing and had top-quality collateral, that repo market remained open and stable. But in the interbank bilateral repo market where private label ABS was used as collateral, funding terms were getting stiffer and stiffer. 16

Haircuts on Repo Agreements (%)

|

Securities |

April ’07 |

August ’08 |

|

US Treasurys |

0.25 |

3 |

|

Investment-grade bonds |

0–3 |

8–12 |

|

High-yield bonds |

10–15 |

25–40 |

|

Equities |

15 |

20 |

|

Senior-leveraged loans |

10–12 |

15–20 |

|

Mezzanine-leveraged loans |

18–25 |

35+ |

|

Prime MBS |

2–4 |

10–20 |

|

ABS |

3–5 |

50–60 |

Source: Tobias Adrian and Hyun Song Shin, “The Shadow Banking System: Implications for Financial Regulation,” Federal Reserve Bank of New York Staff Reports 382, July 2009, table 9. Based on IMF Global Financial Stability Report, October 2008.

The step up in haircuts would put huge pressure on the investment banks that relied most heavily on short-term funding markets. And it was clear which of those, after Bear, was most vulnerable. The warning signs at Lehman were unmistakable. 17 Like Bear, it was known to have taken huge risks on real estate in the hope of catapulting up the Wall Street league table. It had fully integrated its business with the mortgage securitization pipeline. Since the beginning of 2008, the bank’s stock had lost 73 percent of its value. As at Bear, commercial paper issuance by Lehman fell from $8 billion in 2007 to $4 billion in 2008. Nevertheless, on May 31, 2008, its liquidity pool, which was intended to cover cash outflows over a twelve-month period, was as high as $45 billion. 18 In June 2008 investors were sufficiently confident to commit $6 billion in new share capital. What pushed Lehman over the edge were collateral calls by anxious lenders. Given the falling value of its stock, J.P. Morgan demanded large postings of collateral to back up daytime triparty repo risks. By Tuesday, September 9, allowing for liens on its assets, Lehman’s liquidity pool was down to $22 billion. Two days later, on Thursday, September 11, Lehman was still posting $150 billion as collateral in the repo market. 19 But then confidence broke. S&P, Fitch and Moody’s all downgraded Lehman. Its share price fell and with that went its standing in the repo markets; $20 billion in repo did not roll and J.P. Morgan demanded $5 billion in collateral to sustain even the most essential part of Lehman’s triparty repo business. Within a matter of hours on Friday, September 12, the Lehman liquidity pool was down to $1.4 billion and it was clear that, barring a weekend rescue, it would be forced to file for bankruptcy.

On Monday, September 15, as Lehman’s staff around the world stumbled dazed out onto the pavement, the question was who might be next. Bear and Lehman were badly run. Under intense competitive pressure they made high-risk bets on some of the worst parts of the mortgage securitization business. But they were not exceptional. Merrill Lynch too had huge real estate exposure, and it was funding $194 billion of its balance sheet on a short-term basis in the summer of 2008. 20 In total, prior to the Lehman bankruptcy, $2.5 trillion in collateral was posted in the triparty segment of the repo market alone on a daily basis. This gigantic pile of claims and counterclaims could become destabilized in a matter of hours. Market analysts recognized the bimodal quality of this experience. It was a “massive game theory,” one commented. 21 In trilateral repo, given the unimpeachable quality of the collateral used, there was effectively no price adjustment mechanism. One day the investment banks, dealers and those they borrowed from and lent securities to all functioned as a gigantic trillion-dollar machine based on confidence and widely acceptable collateral. The next day even a very large player in the system could be shut out.

Quantites of Assets of Various Classes Financed by Lehman Brothers Through Tripart Repos

Source: Adam Copeland, Antoine Martin and Michael Walker, “Repo Runs: Evidence from the Tri-Party Repo Market,” Federal Reserve Bank of New York Staff Reports 506, July 2011 (revised August 2014).

After Lehman, the next link in the shadow banking chain to come under acute pressure was AIG, the insurer. In a dramatic burst of expansion from the 1990s onward, the Financial Products division of AIG had developed into a major player in the derivatives markets. In total in 2007 it had a book of $2.7 trillion in derivatives contracts. 22 Of this total, credit default swaps accounted for $527 billion. Of these, $70 billion were on mortgage-backed securities, and of those, $55 billion had exposure to dangerous subprime. Given its inside knowledge of the property market, AIG had stopped writing new CDS already in 2005. But given the relatively small size of the portfolio and the AAA rating of the assets it had written CDS on, it had not thought it necessary to insulate itself against losses. It was a fatal mistake. Out of a total of 44,000 derivatives contracts on the books of AIGFP, there were, it turned out, a cluster of 125 CDS on mortgage-backed securities that were about to go bad in a spectacular way. Those 125 contracts would inflict book value losses on AIG of $11.5 billion, twice what the ill-fated AIGFP unit had earned between 1994 and 2006. This was a heavy blow, but given its enormous global business, AIG could absorb portfolio losses on this scale. In due course the market would bounce back. Nor was AIG facing demands to pay out on MBS that had actually defaulted. As at Bear and Lehman, it was not the slow-moving crisis in real estate markets that threatened AIG. An avalanche of defaults and foreclosures would in due course grind its way through the system. But that would take years. The first credit default event on which AIG had to pay out did not occur until December 2008. The problem was the anticipatory reaction of financial markets and the fast-moving revaluation of securitized mortgages and the derivatives based on them. In the case of AIG, as it lost its top-tier credit rating, this triggered immediate margin calls from the counterparties to AIG’s insurance contracts. They wanted collateral to prove that AIG could meet its obligations if the mortgages did go bad. It was these collateral calls, running into tens of billions, that threatened to tip AIG over the edge.

AIG’s troubles did not end there. It had made life much harder for itself by engaging in the securities lending business. A group within AIG specialized in pooling the high-quality Treasurys and other securities held by AIG’s insurance funds. It lent those assets to other investors in exchange for cash, a trade akin to a repo. AIG’s securities-lending business then looked to maximize returns by investing the cash it received from the securities loan in higher-yielding but more risky mortgage-backed securities. Perversely, the securities lending office of AIG began to take those risky bets in 2005 precisely at the moment that AIG’s own Financial Products division decided it was too risky to continue writing CDS on mortgage-backed securities. By the summer of 2007, AIG’s securities lending program had $45 billion invested in high-yield private label MBS. As the securitization business collapsed, those assets became virtually unsalable, leaving AIG scrambling to find funds with which to repay the securities borrowers who now wanted their cash back. In search of profit, a cash-rich insurance company sitting on a giant portfolio of high-quality securities had turned itself into a dangerously leveraged shadow bank with a serious maturity mismatch. And to make matters worse, it was dealing with some of the most heavy-hitting players in global finance.

Taking the lead in making collateral calls against AIG was Goldman Sachs. 23 It was one of the sharpest operators in the market. But it was also an investment bank with no FDIC-insured deposit base. Like Bear, Lehman and Merrill, Goldman was acutely vulnerable to a loss of confidence. One of the plays that would see Goldman through the crisis was the big short position it had built, betting against mortgage-backed securities. A big piece of that bet was placed by buying CDS from AIG. Already by June 30, 2008, Goldman had called $7.5 billion in collateral. When AIG was downgraded on September 15, there was a new surge in margin calls. Of the total claim against AIG, which now topped $32 billion, Goldman Sachs and its partner Société Générale accounted for $19.8 billion. 24 For AIG the consequences were drastic. It was scrambling for cash at the worst possible moment. With its rating on the downgrade it could not borrow tens of billions through ordinary channels. It could raise the funds only through fire sales, and that meant recognizing the losses on its balance sheet, which would make its position only even more precarious. By the morning of September 16, AIG was hours away from default.

With ABCP, repo and CDS having gone into crisis, the next link to snap in the shadow banking chain was the money market funds. On September 10, ahead of the Lehman failure, MMF collectively administered $3.58 trillion in savings and cash resources for individuals, pension funds and other investors. 25 An essential part of their appeal was that while they offered better returns than ordinary savings accounts, they also promised that the principal invested was safe. They would return a dollar on the dollar whatever happened. The day after Lehman, on September 16, that illusion burst. The Reserve Primary Fund, one of the oldest and most respected in the business, with more than $62 billion under management, alerted the Fed that it was about to “break the buck.” It could no longer guarantee a payout of one dollar for every dollar invested. In August 2007 the Reserve Primary Fund had been under intense competitive pressure. To improve its yield and attract more investors it had committed 60 percent of its funds to buying ABCP just as other investors pulled out. 26 The high yields on offer from desperate borrowers catapulted the fund from the bottom 20 percent to the top 10 percent in the performance league and doubled its assets under management in a single year. But it also exposed its investors to serious risks. In general its managers picked well. But 1.2 percent of its funds were invested in high-yielding Lehman ABCP, and by September those had plunged in value. The eventual losses at Reserve Primary were tiny. By 2014 the fund would pay out 99.1 cents on the dollar, but in the days following September 15, with investors no longer certain that they would get full reimbursement, half a trillion dollars fled out of exposed mutual funds looking for the safety of US Treasurys. 27

The events of September 2008 brought the spectacular contraction of wholesale funding markets that had begun in August 2007 to crisis point. An index of haircuts on lower-quality collateral used in the biparty repo market surged from the elevated level of 25 percent it had reached over the summer of 2008 to 45 percent. 28 This had the effect of doubling the amount of money an investment bank would have to mobilize to hold anything other than top-quality securities on its books. Even at Goldman Sachs, the strongest of the stand-alone investment banks, its vital liquidity reserve, which it had pumped from $60 billion in 2007 to $113 billion by the third quarter of 2008, plunged on September 18 to a nominal total of $66 billion. 29 If that slide continued, the game would soon be up.

Meanwhile, the run for safety contracted balance sheets, which had the effect of withdrawing credit from the rest of the system. Loans by banks, investment banks, hedge funds and mutual funds to big businesses in the United States—so-called syndicated loans—fell from $702 billion in the second quarter of 2007 to as little as $150 billion in the fourth quarter of 2008. Interest rates demanded from high-yield, high-risk corporate borrowers surged to 23 percent, shutting out all but the most desperate borrowers. 30 This put a huge squeeze on all business activities. At the same time, corporations that were finding it hard to gain credit elsewhere increased the draw down on their existing credit lines, putting further pressure on the banks. 31

As money market mutual funds, repo, ABCP and AIG’s credit default swaps all came into question, the shock waves spread far beyond the United States. Among the investments most favored by the money market funds were European bank debts. They were a key source of dollar funding for the European megabanks. 32 With the mutual funds pulling back, how were the European banks to fund their large books of dollar assets? With interbank lending shutting down, the European banks resorted to a variety of roundabout mechanisms to obtain dollar funding. A measure of their desperation was the price that they were willing to pay to borrow in euro, sterling, yen, Swiss francs and Australian dollars, and then to swap those loans into dollars. Normally, since these were close to risk-free transactions, the premium was zero. As dollar funding shut down, it soared to 2–3 percent. Applied to balance sheets running into the trillions of dollars, that spread was enough to threaten an avalanche. If the Europeans couldn’t fund their dollar portfolios at affordable rates, they would be forced to sell. But as the Paribas announcement had made clear already in August 2007, there simply was no market for assets, which once had been valued at hundreds of billions of dollars. On Tuesday, September 16, 2008, the day after Lehman, Europe’s funding issues were judged to be so serious that they were first order of business for the Fed’s Open Market Committee meeting, even before Bernanke and his colleagues turned to the problems of AIG. 33

Nor was it just the Fed that was preparing for the end of the world. By conference call early in the morning on Saturday, September 13, Jamie Dimon of J.P. Morgan commanded his astonished senior staff to prepare for Armageddon. While J.P. Morgan would retreat to the safety of its legendary “fortress balance sheet,” they should brace for the bankruptcy of every investment bank on Wall Street, not just Lehman, but Merrill Lynch, Morgan Stanley and Goldman too. 34 Meanwhile, on the other side of the Atlantic, the impact of the funding crisis on a string of big European lenders was devastating. HBOS and RBS in Britain, Fortis and Dexia in the Benelux, Hypo Real Estate in Munich, Anglo Irish Bank, UBS, Credit Suisse and dozens of others all faced failure. Given that there weren’t any deposits, no one needed to run. You just stopped transacting in money markets and pulled in your horns. The result of the collective flight to safety, not by households but by the largest actors in the global financial system, was a trillion-dollar disaster.

II

Beyond Manhattan and the City of London, the economic news was devastating. Real business activity was collapsing on both sides of the Atlantic. In Europe no less than in the United States it was the crisis of 2008, not the later eurozone debacle, that marked the decisive break in investment, consumption and unemployment. From the second half of 2007, as banks great and small in Germany, France, Britain, Switzerland, and the Benelux began to acknowledge the scale of their losses, lending collapsed. The banking sector felt the pressure first because it was most dependent on the daily churn of vast volumes of credit. But soon the crunch extended to nonfinancial corporations and households too. In the eurozone, after running at between 10 and 15 percent, growth in new lending plummeted to zero. It wasn’t the sovereign debt crisis of 2010 that halted Europe’s growth, it was the transatlantic banking crisis of 2008.

Lending In Eurozone to Households and Businesses Other Than Banks, Year-on-Year Growth (%)

Source: http://macro-man.blogspot.co.uk/2016/06/a-broad-scan.html .

As new mortgage borrowing contracted, the slide in the housing market accelerated. Falling house prices and collapsing financial markets slashed personal wealth. In Spain net wealth per person fell by at least 10 percent between 2007 and 2009. Within five years personal wealth would plunge by 28 percent, or 1.4 trillion euros, more than a year’s worth of output. 35 In the UK, as the stock market and house prices slumped, household wealth losses in 2008–2009 were estimated by the IMF at $1.5 trillion—50 percent of GDP in a matter of twelve months. Ten percent of home owners found themselves mired in negative equity. 36 In Ireland, house prices, having quadrupled between 1994 and 2007, halved between 2008 and 2012, taking household wealth with them. 37 These were severe shocks, but for sheer scale the US crisis trumped them all. An early IMF estimate in the summer of 2009 put US household wealth losses at $11 trillion. 38 By 2012 the US Treasury would raise that to $19.2 trillion. 39 Independent estimates put the figure closer to $21–22 trillion—$7 trillion from real estate, $11 trillion in the stock market and $3.4–4 trillion in retirement savings. 40 From their peak in 2006, by 2009 US house prices had fallen by a third. At the worst point in the crisis, 10 percent of home loans across the United States would be seriously in arrears and 4.5 percent of all mortgages crashed into foreclosure. More than 9 million families would lose their homes. Millions more suffered years of anxiety as they struggled to make payments on homes that were no longer worth the mortgages secured on them. At the worst point in the crisis more than a quarter of US homes had negative equity. 41

And the pain was compounded by the distribution of losses between wealthier and poorer households. Between 2007 and 2010 the mean wealth of American households fell from $563,000 to $463,000. But those figures are elevated by the huge fortunes of the very wealthy. If we look instead at the median household—the household that sits at the 50 percent mark in the wealth distribution—it saw its net worth halved from $107,000 to $57,800. 42 And as bad as these figures are, the experience of America’s minority populations was worse. The median wealth of the Hispanic population, which had participated particularly actively in the housing boom, plunged by 86.3 percent between 2007 and 2010. 43 The median African American household saw virtually its entire housing wealth wiped out, and African American home owners were twice as likely to suffer foreclosure as white borrowers. 44 It did not produce the memorable imagery of the 1930s Dust Bowl, but the housing crisis that began in 2007 forced the largest mass movement of people in the United States since the Great Depression. And as minority home ownership collapsed, the result was resegregation along racial lines. 45

With households suffering, in America’s economic downswing of 2008 it was consumption that led the way. 46 As demand fell, so did production and employment. In the Central Valley in California, which witnessed a collapse of 50 percent in home values, consumption was cut by 30 percent. 47 Every kind of expenditure that could be postponed was cut back. For America’s long-ailing motor vehicle industry it was the coup de grâce. Car and light vehicle sales plunged from an annual rate of 16 million units in 2007 to as few as 9 million per annum in 2009. By December 2008 it was clear that both Chrysler and General Motors would fail. In the early twenty-first century GM was no longer the national totem that it had once been. Its total worldwide employment in 2007 was 266,000, compared with a peak of 853,000 in 1979. But as 2008 began it was still the largest car company in the world. GM paid $476 million in salaries each month as well as the health-care and pension benefits for 493,000 retired workers. Its production operations generated $50 billion in orders for parts and services supplied by 11,500 vendors. 48 In total, industry lobbyists claimed that c. 4.5 percent of all US jobs were supported by the auto industry, paying more than $500 billion annually in wages and generating more than $70 billion in tax revenues. 49 On November 7, 2008, GM declared that, barring government aid, it would face insolvency by the summer of 2009.

The imminent failure of GM and Chrysler was an exclamation point on the long-running decline of the American auto industry. One version of the American Dream was dying. But Detroit’s crisis sent shock waves around the world. The future of GM’s long-established UK and German divisions, Vauxhall and Opel, was in doubt. 50 So too were Detroit’s operations in Mexico. Under the NAFTA free trade system, interconnected production systems, known as value chains, had been stretched from one end of North America to the other. As a result, Mexico’s dependence on the United States was overwhelming. In 2007, 80 percent of Mexico’s exports were sent to the United States. As the American crisis hit, Mexico’s GDP fell by almost 7 percent, a worse contraction even than during the homegrown financial crisis of 1995—the so-called Tequila Crisis. 51 Mexico’s nonoil exports fell by 28 percent between May 2008 and May 2009. Automotive exports fell by 50 percent. 52 In the northern industrial cities of Ciudad Juárez and Tijuana, the great maquiladora export processing centers, employment in manufacturing fell by more than 20 percent. Together with the surging violence of the drug wars, the recession led more than 100,000 desperate workers and their families to abandon Juárez. As unemployment surged north of the border, remittances dried up and hundreds of thousands of migrants returned home, making the situation of the poorest Mexicans progressively more desperate. Meanwhile, the inflow of new foreign investment in Mexico halved and the peso plunged in value from 11 to 15 to the dollar, driving up the cost of living.

Nor was the pain confined to North America. For decades GM’s great global rival was Toyota, and 2008 would be the year in which Toyota claimed the title of the world’s leading car producer. It paid a heavy price. In 2009 Japan was rocked by a “Toyota shock” as its national champion reported its first loss in seventy years and cut global production by 22 percent. 53 From a profit of $28 billion in 2007–2008, Toyota slid to a loss of $1.7 billion in 2008–2009. In the words of its president, Katsuaki Watanabe, “The change in the world economy is of a magnitude that comes once every hundred years. . . . We are facing an unprecedented emergency.” 54 As inventories of unsold cars piled up in the United States and Europe, Japanese car exports fell by two-thirds. 55 Japan’s investment industries stopped in their tracks. Hitachi, the giant producer of capital goods and electronics, was worst hit, facing a record loss for a Japanese industrial company of $7.87 billion. 56 Consumer electronics icon Sony announced a loss of $2.6 billion. Toshiba expected to lose $2.8 billion, Panasonic $3.8 billion. 57 All in all, in January 2009 Japan’s economy contracted at a rate of 20 percent per annum and exports by 50 percent year on year. 58 The largest part of this was accounted for by a fall in exports to the United States, followed by Japan’s immediate Asian neighbors, China, Taiwan and Korea, all of which were plunged into recession.

As the shock of 2008 revealed, with supply chains synchronized to perfection, “factory Asia” responded within a matter of weeks to any hesitation of demand in Europe and America. Nor were they the only ones to be hit. Germany suffered a 34 percent fall in exports between the second quarter of 2008 and 2009, with its machinery and transport equipment sector taking a deep dive. It was the most severe economic shock suffered by the Federal Republic since its foundation in 1949. As one bank economist remarked: “One has to go back to the 1930s during the Great Depression to find comparably horrible figures.” 59 Meanwhile, emerging markets were hit too. Turkey, which had joined the club of rapidly growing economies after its financial stabilization in 2004, suffered a sudden and jarring stop. By the first quarter of 2009, Turkey’s GDP was falling by 14.7 percent on an annualized basis. Unemployment rocketed from 8.6 percent in the summer of 2008 to 14.6 percent in the first winter of the crisis. It was the worst affected of any of the emerging markets outside Eastern Europe. Turkey had not seen a situation so bad as this since the disastrous financial crisis of 2001. 60 Istanbul’s stock market plunged by 54 percent between December 2007 and November 2008. 61

What made the collapse of 2008 so severe was its extraordinary global synchronization. Of the 104 countries for which the World Trade Organization collects data, every single one experienced a fall in both imports and exports between the second half of 2008 and the first half of 2009. Every country and every type of traded goods, without exception, experienced a decline. 62

If in manufacturing the downturn was in the volume of trade—the number of cars shipped or the number of cell phones exported—in commodities the shock was to prices. In the worst six months of 2008, oil prices fell by more than 76 percent. That in turn wreaked havoc with the budgets of the petrostates. Saudi Arabia swung from a budget surplus of 23 percent of GDP in 2008 to a substantial deficit. 63 Kuwait was rocked by the crisis at Gulf Bank, which faced losses on currency trades. 64 But nowhere was worse affected than the boomtown of Dubai. Driven by surging commodity prices, heavily backed by international banks such as RBS and Standard Chartered, Dubai’s real estate sector had become the center of a global construction frenzy. 65 By 2008 the city bristled with construction cranes. Its palatial malls boasted floor space four times the per capita level in the United States. In the autumn of 2008 the bubble burst. New credit was slashed. By February 2009 Dubai’s rip-roaring six-year construction boom had come to a halt. Half of a portfolio of $1.1 trillion in construction projects being undertaken in the Gulf Cooperation Council was canceled in a matter of months. Luxury cars were abandoned in droves as Western contract workers scuttled to the airport to escape debtor’s prison. An airlift of charter flights repatriated tens of thousands of migrant guest workers to India. 66

As both household consumption and business investment plummeted, of the sixty countries that supply the IMF with quarterly GDP statistics, fifty-two registered a contraction in the second quarter of 2009. 67 Not since records began had there been such a massive synchronized recession. Tens of millions of people were thrown into unemployment. Though it was dazed bankers with boxes of belongings stumbling out of office towers in London and New York that attracted the TV cameras, it was young, unskilled blue-collar workers who suffered the worst. 68 In the United States, the epicenter of the crisis, the month-on-month fall in employment over the winter of 2008–2009 was breathtaking. In the worst period, the monthly rate of job losses topped 800,000. Among the African American population the surge was particularly dramatic, with unemployment rising from 8 percent in 2007 to 16 percent by early 2010. 69 Young black workers were particularly hard hit, with their unemployment rate surging to 32.5 percent by January 2010. At the very bottom of the pile were young African American men with no high school diploma. In New York City in 2009 their unemployment rate was more than 50 percent. 70 Precisely how many people lost their jobs across the global economy depends on our guess as to joblessness among China’s giant migrant workforce. But reasonable estimates range between 27 million and something closer to 40 million unemployed worldwide. 71

III

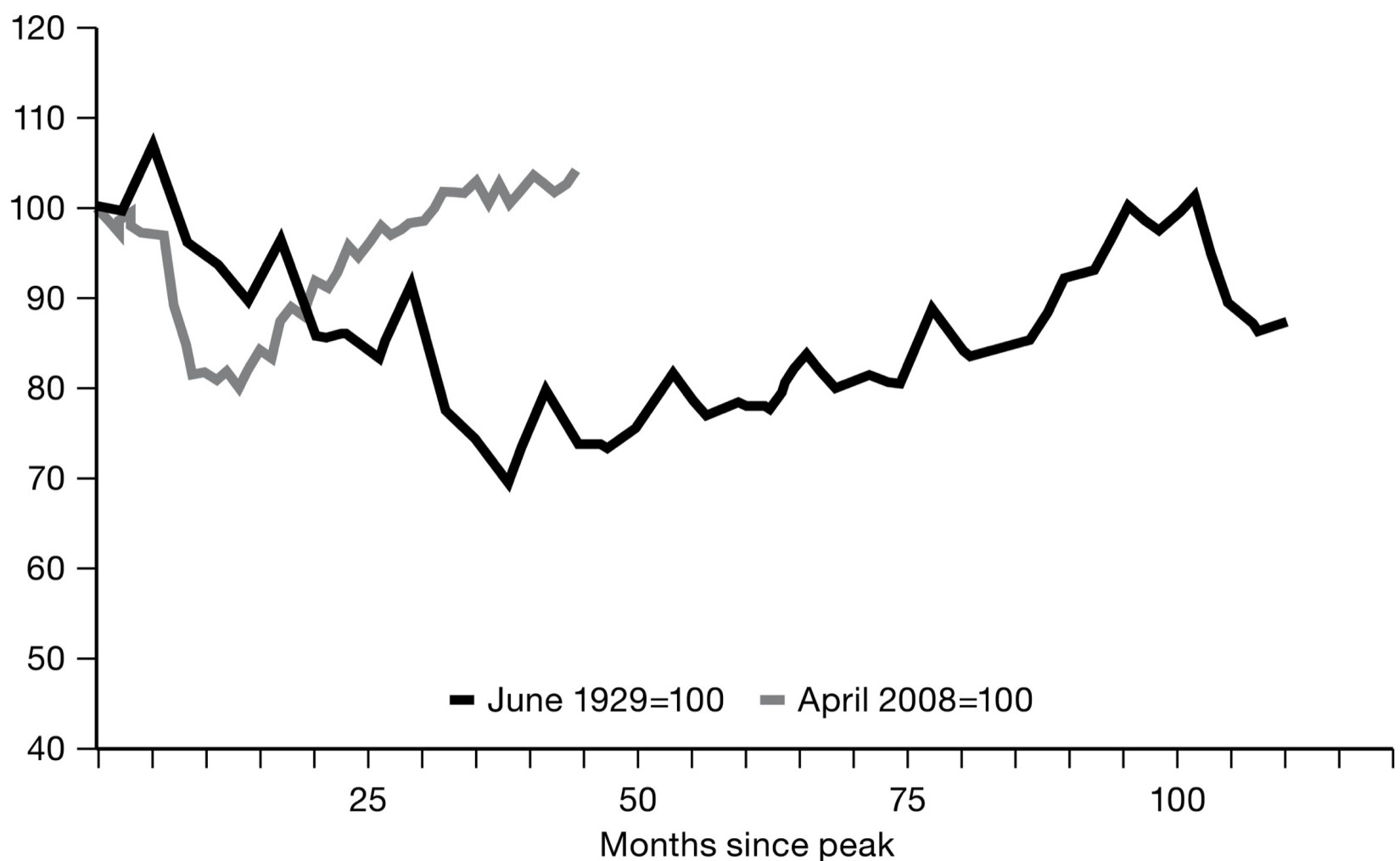

The situation was clearly bad. But in historical terms, how bad was bad? Trying to find his bearings, in the spring of 2009 Paul Krugman concluded that the situation was dire. But at least as far as the industrial economy of the United States was concerned, it was less grim than it had been in the Great Depression of the 1930s. 72 It was, he quipped, only “half a Great Depression.” It was not a judgment that stood for long. As critics scrambled to point out, Krugman’s assessment was deeply parochial. The Great Depression of the 1930s was not confined to the United States, and neither was the crisis that struck in 2008. On a global level, industrial output, stock markets and trade were all falling at least as fast in 2008–2009 as they had in 1929. 73

Volume of World Trade: 1929 and 2008 Compared

Source: Barry Eichengreen and Kevin O’Rourke, “A Tale of Two Depressions Redux,” http://voxeu.org/article/tale-two-depressions-redux .

We now know that urgent and massive countermeasures would forestall the kind of agonizing depression that the world experienced in the early 1930s. But that relatively sanguine perspective depends on the safety of hindsight. In September 2008 the scale of the response was an index of the desperation felt by those at the epicenter of the crisis in the United States. Ben Bernanke at the Fed, Tim Geithner at the New York Fed and Hank Paulson at the Treasury all recounted the experience as traumatic. After Lehman collapsed, Paulson confronted his staff with the prospect of an “economic 9/11.” 74 On the morning of September 20, the US Treasury secretary alerted Congress to the fact that unless they acted fast, $5.5 trillion in wealth would disappear by two p.m. They might be facing the collapse of the world economy “within 24 hours.” 75 In private session with congressional leadership, Bernanke, who is not given to overstatement, warned that unless they authorized immediate action, “we may not have an economy on Monday.” 76

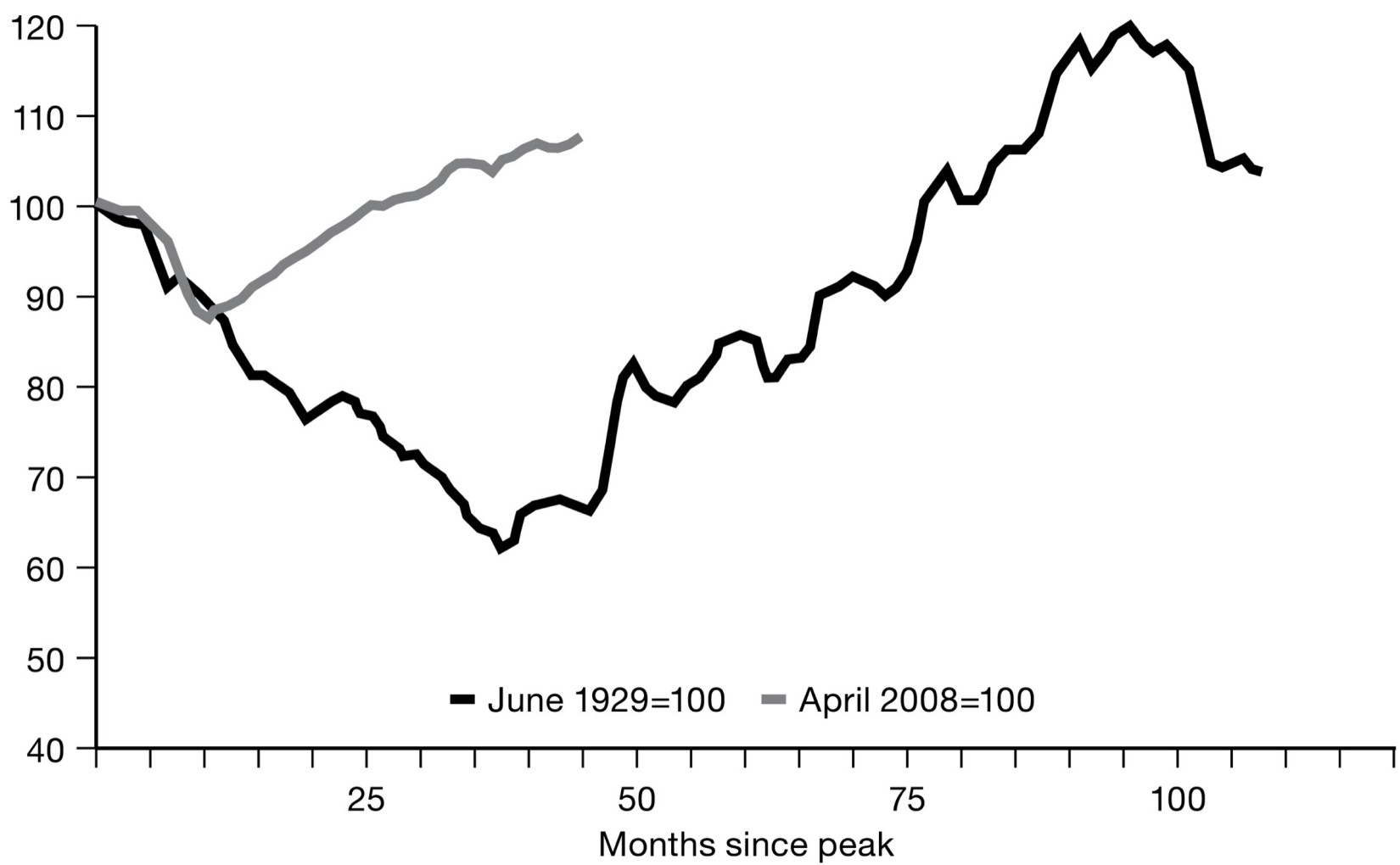

World Industrial Production, Now Versus Then

Source: Barry Eichengreen and Kevin O’Rourke, “A Tale of Two Depressions Redux,” http://voxeu.org/article/tale-two-depressions-redux .

As far as America was concerned, this was clearly an exaggeration. Bernanke was trying to scare Congress into action. But if one looks at data on international investment flows, the picture is truly astonishing. Across the world before the crisis hit, inflows and outflows of capital came to just under 33 percent of world GDP. The vast majority of this was accounted for not by transactions between the advanced world and emerging markets but by flows between advanced economies. At the height of the crisis, between the last quarter of 2008 and the first quarter of 2009, those flows collapsed by 90 percent to less than 3 percent of global GDP. 77 In the second half of 2008 capital flows between rich countries plunged from $17 trillion to barely more than $1.5 trillion. No other aggregate in the global economy was affected on anything like this scale or with this suddenness. It was as though a gigantic stabilizing flywheel suddenly came crashing to a halt, sending a shuddering jolt through the entire financial system.

Gross Capital Flows as a Percentage of World GDP

Source: Claudio Borio and Piti Disyatat, “Global Imbalances and the Financial Crisis: Link or No Link?,” BIS Working Paper 346 (2011), graph 5.

In public, Ben Bernanke knew it was essential for him to keep a straight face: “Financial panics have a substantial psychological component. Projecting calm, rationality, and reassurance is half the battle,” he would later opine. 78 But as an economist and an economic historian, Bernanke understood the scale of what he was up against. What threatened in 2008 wasn’t 1929. What threatened was something even bigger and quite possibly even worse. As he was to affirm on several occasions afterward, for Bernanke, “September and October of 2008” was clearly the “worst financial crisis in global history, including the Great Depression.” 79 In the 1930s there was no moment of such massive synchronization, no moment in which so many of the world’s largest banks threatened to fail simultaneously. The speed and force of the avalanche was unprecedented. As Bernanke later admitted to the readers of his memoirs, “[I]t was overwhelming, even paralyzing, to think too much about the high stakes involved, so I focused as much as I could on the specific task at hand. . . . [A]s events unfolded I repressed my fears and focused on solving problems.” 80 Only as he neared the end of his second term was he ready to unwind. Looking back, it was like being in a car wreck. “You’re mostly involved in trying to avoid going off the bridge; and then later on you say, ‘oh my god!’” 81

Tim Geithner, from his vantage point at the New York Fed, gave a typically hard-boiled insight into his perspective on the struggle to save the financial system: “I didn’t have a way to explain the terror of those days until later, when I saw The Hurt Locker, the Oscar-winning film about a bomb disposal unit in Iraq. What we went through on interminable conference calls in fancy office buildings obviously did not compare with the horrors of war, but ten minutes into the movie I knew I had finally found something that captured what the crisis felt like: the overwhelming burden of responsibility combined with the paralyzing risk of catastrophic failure; the frustration about the stuff out of your control; the uncertainty about what would help; the knowledge that even good decisions might turn out badly; the pain and guilt of neglecting your family; the loneliness and the numbness.” 82

There is no reason to doubt the sincerity of these professions. It was a fearful situation. But the metaphors—terrorist attack, car wrecks and unexploded improvised explosive devices—are telling. They position the crisis-fighting team as first responders facing a compelling emergency. And they place us, their audience, by their side. Who would not root for the fatherly Ben Bernanke trying to keep the family car on the bridge, or Geithner’s heroic bomb disposal team? Politics is set aside as we anxiously watch our heroes struggle to rescue us from disaster. There is no time to ask why this is happening. We are “all in this together.” But it is precisely with that assertion that a political economy of the crisis begins. 83 Which system was it that needed to be saved in the autumn of 2008? Who was being hurt? Who was included in the circle of those who needed to be protected? And who was not?

As the crisis spiraled toward September 2008 the first responders performed a substitution. It had all started with the predictable but devastating bursting of the housing bubble. That crisis was affecting millions of households on both sides of the Atlantic. But starting with the rash of bank failures and fund failures in the late summer of 2007, the real estate crisis was gradually displaced from the center of attention. What now mattered was the possible failure of an investment bank. By September 2008 it was no longer individual banks but the entire financial system that had to be saved at all costs. It was entire markets and sectors—the repo market, ABCP, the mutual funds—that needed life support. It was the implosion of the financial system, imagined as something akin to a massive electrical power failure that threatened the entire economy.

It was crucial to fix Wall Street, so the slogan went, to help Main Street. The mantra was repeated in local idiom all over the world. And for the purposes of ongoing business activity, it clearly was crucial to maintain business credit. In September even blue-chip businesses could not get short-term funding. McDonald’s could no longer get an overdraft from Bank of America. 84 Engineering giant GE and Harvard University were rumored to be having liquidity issues. 85 But beyond such immediate rescue measures, did the all-out focus on the financial system really serve the interests of the real economy? 86 Was the inability to borrow causing a failure of investment and thus the ongoing depression? Or were the collapsed housing market and cash-strapped households curtailing economic activity such that there was no incentive to invest and thus no demand for loans?

These might seem like academic questions. The bomb was ticking. The car was hurtling off the bridge. Amid a global catastrophe, did it really matter which way the arrow of causation was pointing? Amid the intensity of the financial crisis, why should anyone care? Because the decision made by the American crisis fighters to take those questions off the table and to give absolute priority to saving the financial system shaped everything else that followed. It set the stage for a remarkable and bitterly ironic inversion. Whereas since the 1970s the incessant mantra of the spokespeople of the financial industry had been free markets and light touch regulation, what they were now demanding was the mobilization of all of the resources of the state to save society’s financial infrastructure from a threat of systemic implosion, a threat they likened to a military emergency.

Chapter 7

BAILOUTS

T he ferocity of the financial crisis in 2008 was met with a mobilization of state action without precedent in the history of capitalism. Never before outside wartime had states intervened on such a scale and with such speed. It was a devastating blow to the complacent belief in the great moderation, a shocking overturning of prevailing laissez-faire ideology. To mobilize trillions of dollars on the credit of the taxpayer to save banks from the consequences of their own folly and greed violated maxims of fairness and good government. But given the risk of contagion, how could states not act? Having done so, however, how could they ever go back to the idea that markets were efficient, self-regulating and best left to their own devices? It was a profound challenge to the basic idea that had guided economic government since the 1970s. It was all the more significant for the fact that the challenge came not from the outside. It was not motivated by some radical ideological turn to the Left or the Right. There was precious little time for thought or wider consideration. Intervention was driven by the financial system’s own malfunctioning and the impossibility of separating individual business failure from its wider systemic repercussions. Martin Wolf, the Financial Times ’s esteemed chief economic commentator, dubbed March 14, 2008, “the day the dream of global free-market capitalism died.” 1 That was the day the Bear Stearns rescue was announced. It was only the beginning.

I

Bailout battles were fought all along the contours of the integrated Atlantic financial economy—in the United States, Iceland, Ireland, Britain, France, Germany, the Benelux, Switzerland. The financial firepower deployed was immense and accounting for it became a field of political argument in its own right. But whichever metrics we use, it is clear that there had never before been anything so extensive or massive in scale. Commitments were made in excess of $7 trillion.

The main mechanisms for intervention were fourfold: (1) loans to banks; (2) recapitalization; (3) asset purchases; and (4) state guarantees for bank deposits, bank debts or even for the entire balance sheet. Everywhere the crisis struck, states were forced to take some combination of these measures. The agencies involved were central banks, finance ministries and banking regulators. What summary statistics cast as cool enumerations were, in fact, frantic, improvised solutions that emerged from barely coordinated sessions of all-day, all-night problem solving. As the crisis intensified it put the financial and political resilience of states to the test. Broadly speaking, this produced four types of outcome, which reflect the degree of immersion in global finance, the resources of the states at risk, the shape of the governing elite and the balance of power within the financial sector itself. 2

In the most extreme cases the crisis overwhelmed the state. Ireland and Iceland simply did not have the resources, the institutions or the political capacities to deal with the gigantic shock to their overgrown financial sectors. They would suffer a comprehensive crisis, as would the worst-hit emerging market economies of Eastern Europe. Others were better placed. Despite having a grossly overgrown financial sector, Switzerland survived intact. It did so through early, intense and unrelenting attention to its one failing megabank, UBS. 3 Though it was never nationalized, it became in effect a ward of the state. The larger European states and those with less excessive banking systems—the UK, Germany, France, Belgium and the Netherlands—presented a more mixed bag. Despite the scale of the crises they faced, they had the resources to cope. They attempted comprehensive organizational and financial solutions, including abortive proposals to coordinate a common European response to the crisis. But efforts to achieve consistency and coordination were undermined by national political calculation and the uncooperative behavior of leading banks that fancied themselves large enough to survive without the humiliation of taking state aid. There was no spiraling disaster, but containing the crisis was hugely expensive and success was partial at best.

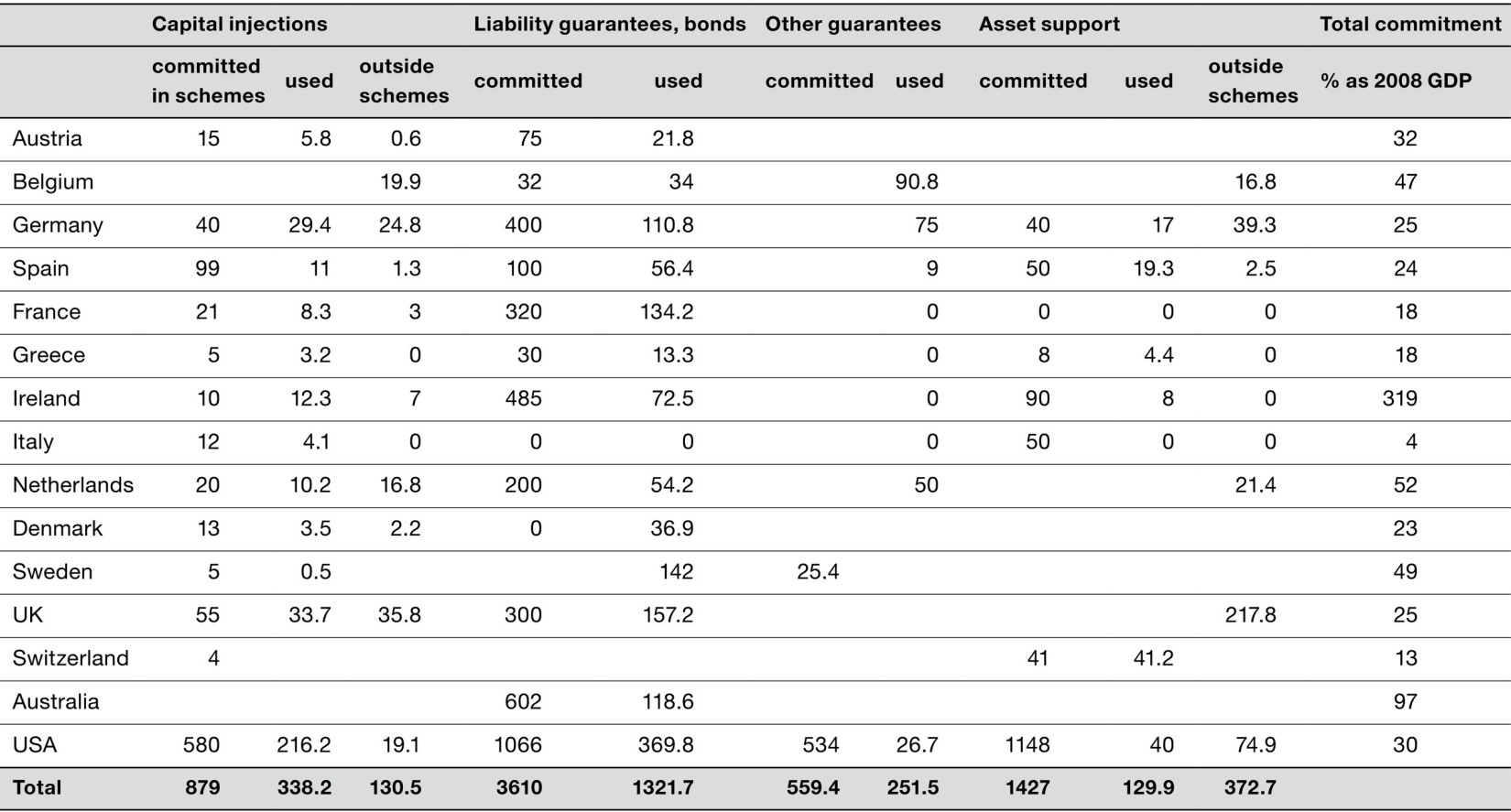

Government Support Measures to Financial Institutions Since October 2008, as of End of May 2010 (in billions of euros unless stated otherwise)

Source: Based on Stéphanie Stolz and Michael Wedow, “Extraordinary Measures in Extraordinary Times: Public Measures in Support of the Financial Sector in the EU and the United States,” Bundesbank Series 1 Discussion Paper 13, 2010.

Out of this trial of strength the United States emerged as the one nation-state with the capacity not only to backstop the biggest financial sector in the world but also to impose a comprehensive solution. Not for nothing, America’s crisis fighters liked to speak in military terms, about “big bazookas” and “shock and awe.” Geithner went furthest in this respect. For inspiration he invoked the war-fighting doctrine developed in the aftermath of the Vietnam debacle by America’s chairman of the Joint Chiefs, Colin Powell: Strike with massive force and plan a clear route out. 4 It was an analogy that had first been invoked by Larry Summers at the time of the Mexico financial crisis in 1994. Now it became Geithner’s mantra. For him, the “Powell Doctrine applied to international finance” meant “the overwhelming use of force, with a clear strategy for resolution.” As Geithner insisted, “There is more risk and greater cost in gradualism than in aggressive action.” For Geithner and his cohorts it was clear that swift and decisive action paid dividends. Compared with the disastrous performance of the European economy, the United States was set back on track. 5 The leadership of American finance renewed itself. Even when viewed narrowly in accounting terms, many of the Treasury and Fed support programs made a profit for the American taxpayer. 6 The benefits of preventing a second Great Depression were vast.

By contrast with the European experience it is not hard to see how this self-congratulatory American narrative gained purchase. But its economic merits are not so obvious as its proponents presume. And it offered no comfort to the advocates of laissez-faire. Gone were the days when economic policy was about shrinking the state to set free the spontaneous order of market liberty. No longer did wisdom lie in devising predictable rules to curtail the arbitrary discretion of policy makers. Economic policy modeled on warfare was a matter of will, vigilance, tactical nous and firepower. And despite the populist appeal of the military rhetoric, there was a political price to pay. 7 The crisis fighting of 2008–2009 scrambled American politics. The Bush administration lost the backing of much of the congressional Republican Party. The crisis snapped the fragile bond between the GOP’s managerial, big-business elite and its right-wing mass base. As the popular wing of the party, backed by maverick oligarch donors, moved increasingly toward indignant antiestablishment opposition, mainline conservatives like Bernanke and Paulson were left to complain that it was not they who left the party, but the party that left them. 8 The Bush administration’s crisis-fighting effort was carried by the Democratic Party’s majorities in Congress. That contradiction would be resolved by Barack Obama’s election victory on November 4, 2008, only weeks after the crisis reached its peak. But the fracture of the American Right would in due course have profound consequences both for America and for the wider world.

II

In 2007 the best hope of the authorities was still that the private sector might rescue itself. J.P. Morgan’s consortium of 1907 was the stuff of Wall Street legend. In late October 2007, with the help of the US Treasury, the three largest banks—Citigroup, Bank of America and JPMorgan Chase—agreed to collaborate in creating a so-called Master Liquidity Enhancement Conduit that would help to stabilize the market for mortgage-backed securities and revive the ABCP market. 9 Not surprisingly, Treasury Secretary Paulson loved the idea. But any private sector arrangement was vulnerable to problems of collective action. Though bankers detested government intervention, they also wanted to avoid the stigma of joining a cartel of ailing firms, especially one including Citigroup, whose balance sheet was particularly toxic. 10 When major global competitor HSBC announced that it would absorb the full amount of $45 billion in losses suffered by its SIVs onto its balance sheets, its largest American rivals could not be seen to be settling for a second-best option. 11 By December 2007 the private bad bank plan had collapsed.

When collective action failed, the state could step in, acting as a matchmaker in chief, brokering takeover deals between individual banks. In Britain in 2008, the Scottish conglomerate HBOS would be sold off to Lloyds Bank with encouragement from Downing Street. 12 Germany’s number two bank, Dresdner, would be amalgamated with Commerzbank, the number three. 13 As both deals would reveal, the risk was that the bank that was in trouble would pull its rescuer down with it. In the United States the amalgamations began in earnest with Bear Stearns, which came to the point of failure on the night of March 13–14, 2008. 14 If it had unloaded its portfolio of $200 billion in asset-backed securities and CDO at fire sale prices, the effect would have been catastrophic. It would have forced all the other banks to recognize crippling losses, spreading the panic. To the relief of the Treasury and the Fed, J.P. Morgan was interested in buying out Bear. Its hard-charging CEO, Jamie Dimon, was confident that his robust balance sheet put him in a position to safely pick over the carcass. But to finalize the deal, Dimon needed the right inducement. Under the emergency powers provided by section 13(3) of the Fed’s statutes, $30 billion in the most toxic assets were taken off Bear’s books by a SIV funded by the New York Fed. 15 Then, at five a.m. on the morning of March 14, with the repo markets closed to Bear, the New York Fed lent $12.9 billion to J.P. Morgan, which J.P. Morgan then lent to Bear. After that, the die was cast. J.P. Morgan initially agreed to pay the laughable price of $2 per share for what was left of Bear. This compared with a valuation of $159 per share only one year earlier. When Bear’s shareholders protested, the price was raised to $10 per share. Whether at $2 or $10, J.P. Morgan was confident it would make a profit.

The Fed’s actions forestalled what might have been a disruptive and chaotic bankruptcy. But the inducements that J.P. Morgan had extracted were debatable, to say the least. Paul Volcker, the legendary ex-chairman of the Fed, would characterize them as extending “to the very edge of its lawful and implied powers.” 16 Strict advocates of moral hazard logic would forever after argue that it was the Bear rescue that set up the Lehman disaster. 17 With one investment bank having been rescued, Lehman’s management felt safe. A solution for their problems would be found too. They could afford to take their time finding the best possible deal, an attitude that would cost them dearly.

Whether it was legal or wise, rescuing investment banks by means of obscure balance sheet transactions was a technical business that could be kept out of the political headlines. That changed with Fannie Mae and Freddie Mac. As the indispensable government-sponsored backdrop to the American housing market, they were at the center of one of the most formidable political networks in Washington. By the summer of 2008, with private securitization stalled, they were also responsible for backstopping 75 percent of new mortgages in the United States. The vast bulk of the Fannie Mae and Freddie Mac balance sheet consisted of top-quality conforming mortgages. If they had had conventional balance sheets, they ought to have been able to ride out the storm. The problem was they did not. In June 2008 Fannie Mae and Freddie Mac held MBS valued at $1.8 trillion and guaranteed another $3.7 trillion on the basis of shareholder equity, which in the case of Fannie Mae came to only $41.2 billion, and in the case of Freddie Mac, to $12.9 billion. 18 It was a leverage ratio that would have made even the boldest investment banker blush. It was conceivable only because Fannie Mae and Freddie Mac were government-sponsored enterprises. In the summer of 2008 the meaning of that term was going to be put to the test. Allowing for only minimal losses, the capital of both Fannie Mae and Freddie Mac would be completely wiped out. If they folded they would take down the last remaining lenders in the mortgage market and put in doubt the credit of the United States. They would put in jeopardy a huge portfolio of securities widely held by foreign investors. In the summer of 2008 foreign investors held $800 billion in debt issued by the GSEs. Fannie Mae and Freddie Mac were, as the influential blogger Brad Setser quipped, “too Chinese to fail.” 19

Desperate to gain a grip on the situation, in the spring of 2008 Hank Paulson’s Treasury began to broker a deal between congressional Democrats and Republicans that would give the federal government the powers necessary to overhaul the mortgage giants. 20 But over the summer Congress dragged its heels. The Republicans were uncooperative and the Democrats insisted that if they were to carry the bill, it must include support for struggling home owners and the transfer of block grants to hard-hit states to buy up foreclosed properties. By mid-July the situation was becoming critical. Given the scale of the crisis and the opacity of the GSEs’ financial situation, the capital injection might need to be huge. 21 The Treasury favored an authorization limited only by the federal government’s borrowing ceiling, putting the full financial clout of the American state behind the GSE. As Paulson famously put it to the Senate Banking Committee, “[I]f you’ve got a squirt gun in your pocket, you may have to take it out. If you’ve got a bazooka, and people know you’ve got it, you may not have to take it out.” 22 Paulson’s request was meant to sound impressive, and his bazooka comment echoed around the world. The US Treasury secretary was desperate to reassure foreign bondholders. Beijing was increasingly alarmed. 23 In his memoirs, Paulson recorded: “I was talking to them [Chinese ministers and officials] regularly because I didn’t want them to dump the securities on the market and precipitate a bigger crisis. . . . And so when I went to Congress and asked for these emergency powers [to stabilize Fannie and Freddie], and I was getting the living daylights beaten out of me by our Congress publicly, I needed to call the Chinese regularly to explain to the People’s Bank of China, ‘listen this is our political system, this is political theatre, we will get this done.’ And I didn’t have quite that much certainty myself but I sure did everything I could to reassure them.” 24

The Chinese might be excused their confusion. The political theater being played in Washington, DC, was new and strange. A conservative, free-market administration led by businessmen was proposing unlimited state spending to nationalize a large part of the housing finance system. The Republican electorate was outraged by the thought of assisting undeserving mortgage borrowers and the New Deal machinery that had aided and abetted their fecklessness. But to Paulson the systemic imperative was obvious. And President Bush stood behind him. “It was a tremendous act of political courage,” Paulson gushed, “It was as if, in the last days of his administration, the president were suddenly switching sides, supporting Democrats and opposing Republicans on matters that went against the basic principles of his administration. But he was determined to do what was best for the country.” 25 Paulson was registering a basic rift within American conservatism. The right wing of the party could not be counted on to give support to measures that were unpopular and distasteful, but were clearly necessary to save “the system.” Paulson recognized that the authorization he was asking for was unprecedented. “I don’t know if any executive branch agency had ever before been given the authority to lend to or invest in an enterprise in an unlimited amount. All I could do was argue that the extraordinary and unpredictable nature of the situation warranted the authority in this case.” 26 He also knew that it was only the Democrats, the party with relatively less inhibition about expanding the scope of government, who were willing to go along with this logic of absolute and unlimited necessity, dictated not by a national security emergency but by a financial crisis.

Paulson’s extraordinary plenipotentiary authorization to rescue Fannie Mae and Freddie Mac passed Congress on July 26, with three quarters of House Republicans voting against. It was signed into law on July 30. The White House thought it best to forgo the usual festive Oval Office ceremony. There was no reason to goad the Republicans and no time to lose. With a team recruited from Morgan Stanley on a pro bono basis, the Treasury plunged into weeks of forensic investigation and negotiations with the GSEs’ failed regulators. The results were dispiriting. Both of the GSEs were insolvent. Liquidity support would not be enough. On Sunday, September 7, 2008, Fannie Mae and Freddie Mac were placed under conservatorship. It was nationalization in all but name. If necessary, the Treasury would replenish their capital to make up any gap between assets and liabilities up to an initial maximum of $100 billion each. The Fed provided credit lines and undertook to buy whatever MBS the ailing GSEs needed to offload. It wasn’t so much a bazooka as the nuclear option.

The crucial effect of this intervention was to reassure bondholders, especially those abroad, that Fannie Mae and Freddie Mac would not fail. Despite the machinations of Russia, the breakdown of America’s government-sponsored mortgage machine did not spill over into a global crisis. But the political fallout was dire and it had serious implications for the future course of the crisis. On the right wing of the Republican Party, fully mobilized for the hotly contested presidential election, the nationalization of Fannie Mae and Freddie Mac unleashed a firestorm. 27 The Treasury did its best to ward off allegations of cronyism by imposing a punitive dividend for the capital it contributed, wiping out the GSEs’ existing shareholders. The American Bankers Association rallied to the administration, calling on Republicans to support the rescue effort. But it was immediately countered by the conservative Club for Growth, a key right-wing lobby group funded by the Koch brothers. House leader John Boehner and former speaker Newt Gingrich spoke out against Paulson’s bailout. John McCain personally was thought to favor a rescue. But on August 29 he nominated the populist Alaskan governor Sarah Palin as his vice-presidential running mate. Palin did not have coherent views on the GSEs or the financial crisis. But her bluff persona fired up the passions of the Republican base. As the crisis deepened, the Bush administration was terrified that they might find themselves facing an insurgency from within their own party led by a presidential candidate on the warpath against bailouts. What made the Republican brush fire so worrying was that by early September it was clear that the rescue of Fannie Mae and Freddie Mac was only the first round, and that the next phase of the battle would be decided not in Washington but on Wall Street.

For months the Treasury had been anxiously watching as Lehman Brothers looked for a buyer. By the second week of September options were running out. Talks with a potential Korean suitor had stalled. In frantic negotiations hosted by Geithner’s New York Federal Reserve and personally overseen by Paulson, the search for a private sector solution failed. The culminating moment came on the weekend of September 13–14. What exactly happened in those forty-eight hours will remain forever a matter of controversy. What is beyond dispute is that Bank of America, the giant commercial bank that had been expected to act as the white knight for Lehman, bought Merrill Lynch instead.

Merrill was bigger than Lehman. It too was heavily exposed to the real estate bust. Like Lehman it was an investment bank that could not function without access to the repo market. After Lehman it would certainly have been the next to fail. 28 But unlike Lehman, Merrill’s management was nimble and saved its bank by pushing for direct talks with Bank of America. It was well known that Bank of America CEO Ken Lewis had long wanted to emulate Citigroup in integrating an investment bank with his commercial banking business. On the desperate weekend of September 13–14, 2008, Bank of America’s hundreds of billions of retail deposits guaranteed by the FDIC were one part of the financial system that was not running. That funding base gave Bank of America the platform to buy out Merrill Lynch. But on what terms? On the face of it Merrill was a prize. One of the biggest names on Wall Street, at the end of 2007 it was valued at $150 billion, with $1.02 trillion in assets and more than sixty thousand employees worldwide. But given the potential losses on its books and its precarious wholesale funding, what was Merrill worth in September 2008? In the event, under huge pressure from Paulson and Bernanke, Bank of America paid $50 billion, $29 per share, a third of what Merrill had recently been worth, but 40 percent more than its market valuation the previous week.

After Bank of America took Merrill, for Lehman, the last remaining hope was a transatlantic deal with the British bank Barclays, where the expat American Bob Diamond, formerly of Morgan Stanley and Credit Suisse, was calling the shots. But Prime Minister Gordon Brown and Chancellor Alistair Darling refused to loosen regulations to allow the takeover to go ahead without full shareholder approval and without commitments of support from the US Treasury. If Bank of America had chosen Merrill, what was wrong with Lehman? They told Paulson that London did not want to “import America’s cancer.” 29

The basic question is why the options for Lehman were so narrow? Why were the Fed and the Treasury unwilling to sweeten the Lehman deal in the way that they had J.P. Morgan’s takeover of Bear Stearns? 30 Why, following the failure of the private option, was some other kind of backstop not worked out, of the kind that they would provide so liberally in the weeks to come? Geithner, Paulson and Bernanke have all insisted that the question is otiose. The problem was not that the Treasury and the Fed lacked the will, but that they lacked the means. The Lehman collapse was not the result of a deliberate intention on the part of the authorities. “We hadn’t done it on purpose,” Geithner insisted. “We had run up against the limits of our authority and the fears of the British regulators.” 31 The Fed could not lend to Lehman, Bernanke maintains, because the Fed lends only against good collateral to solvent banks. 32 Lehman was insolvent and, due to the nature of its investment banking business, its lack of depositor base and alternative income streams, it lacked the collateral. But these are retrospective justifications. At the time Lehman’s failure was seen as the result of a deliberate decision, and a welcome one. On September 17, Democratic congressman Barney Frank declared in a hearing with Treasury officials that Monday, September 15, the day of Lehman’s failure, would long be celebrated as “Free Market Day.” 33 Frank was joking. But others were not. As one of Paulson’s assistants remarked, September 15 felt like a “good day at the Treasury.” They had let markets do their work. 34 A New York Times editorial declared that it was “oddly reassuring” that Lehman had been allowed to fail. 35 The Wall Street Journal congratulated Paulson on not blinking. “[T]he government had to draw a line somewhere.” 36 For Geithner at the New York Fed, this was no comfort: “We hadn’t chosen to draw a line. We had been powerless, not fearless. We had tried but failed to prevent a catastrophic default.” 37

On this interpretation of the crisis, Geithner would go on to base an entire program of state building. If in 2008 what had been missing were adequate state powers of intervention, the answer was to equip the Fed and the Treasury with the right tools. What Geithner could not admit is the possibility that “Hank and Ben” had, in fact, made a mistake. That they might have underestimated the severity of the fallout that Lehman’s failure would cause. Or that Paulson, as a Republican Treasury secretary, might, in fact, have been constrained by politics. But this is what subsequent forensic reconstruction suggests. The best available contemporary evidence, rather than the self-justifications that the actors fashioned for themselves after the catastrophic consequences of Lehman’s failure became apparent, suggests that the basic constraint on the Lehman rescue was Paulson’s refusal, from the outset, to consider another bailout. 38 British chancellor Alistair Darling was in frequent contact with New York throughout the critical weekend. His perspective is telling: “What was worrying was that it was becoming more evident that the US Treasury was reluctant to provide the financial support to make the deal work. I was not entirely surprised. . . . I didn’t think he had enough political capital to persuade the Republicans to nationalize another bank.” 39 It was a judgment that would be borne out two weeks later in the desperate battle to pass the Troubled Asset Relief Program (TARP). Though it was Paulson who took the lead in the Lehman talks in New York, from Washington Bernanke was fully in agreement. The Fed was notably uncooperative in the desperate efforts of Lehman’s management to buy time. Contrary to the impression created by Bernanke’s retrospective testimony, the Fed concertedly pushed Lehman toward bankruptcy. The argument made at the time was that ending uncertainty by means of bankruptcy would help to calm the markets. It is easy to say with hindsight, but it was a spectacular error of judgment.

The scale of that error became clear within hours as the shock wave from the Lehman failure impacted the American and the world economy. A day later, Paulson, Bernanke and Geithner had to face the question of what to do about the insurance giant AIG. 40 Here too their first impulse was to look for a private solution, with J.P. Morgan and Goldman Sachs leading “frenetic” discussions throughout Monday, September 15. But by seven p.m. any hope of a private rescue had evaporated. When the bailout team had reached a similar conclusion about Lehman twenty-four hours earlier, they had started preparing for bankruptcy. This time, the conclusion was the opposite. The financial markets would not withstand a second shock, and AIG’s level of interconnectedness through derivatives, repo and securities lending was even greater than that of Lehman. Letting AIG fail would, in the words of one Wall Street player, have been an “extinction-level” event. Instead, the Fed stepped in. As it had done with Bear Stearns, the Fed declared a section 13(3) emergency. The New York Fed would offer a secured credit facility of up to $85 billion. On the early afternoon of Tuesday, September 16, Fed security personnel rushed to the offices of AIG at 80 Pine Street in Lower Manhattan to gather up tens of billions of dollars of share certificates to serve as collateral. With the deeds to the world’s second-largest insurance company safely stashed in the vaults of the New York Fed, the first phase of the rescue was announced at 3:30 p.m. The Fed backstopped AIG’s credit default swap portfolio and its securities lending business. In exchange it would take stock in AIG and its subsidiaries that would give the US government a 79.9 percent equity stake in AIG’s global insurance business. Following the template established with the Fannie Mae and Freddie Mac nationalization, the deal inflicted a huge loss on AIG’s existing shareholders. The securities lending business was unwound, with the New York Fed purchasing from AIG its depreciated portfolio of MBS, enabling it to pay off its securities-lending counterparties. Most generous of all was the resolution of the CDS portfolio, which was accomplished by buying out the dangerous CDO on which AIG had written insurance. In effect, together with the collateral they had already claimed from AIG, the counterparties received payment at 100 percent of par on $62.2 billion in toxic mortgage-backed securities, the market value of which was closer to $27.2 billion. How little they would have been worth if AIG had been driven into bankruptcy is anyone’s guess. In any case, the subsidy to the counterparties and their clients clearly ran into the billions. Nor was it only the American financial system that benefited. In the course of the bailout, the Fed made sure to leave in place the insurance contracts that AIG had offered to European banks to provide “regulatory relief.” If they had been voided, the Americans estimated that the European banks would have faced calls for at least $16 billion in additional capital. “For fear of shouting ‘Fire!’ in a crowded theater,” the New York Fed later told Congress, it thought it best not even to mention this potential fallout from AIG’s crisis to European regulators.

III