Chapter 3

TRANSATLANTIC FINANCE

A mericans liked to think of their problems as American and outsiders were only too happy to concur. As the mortgage meltdown spread like a lethal virus across urban America in 2007–2008, European commentators took up the narrative of an American national crisis. “Feral” financial capitalism, like the Iraq war and climate change denial, was part of a toxic Anglo-American variant on modernity. 1 When the storm broke in 2008, the Schadenfreude among European politicians was palpable. The polite phrases at the UN only scratched the surface. On September 16, 2008, as Wall Street unraveled, Peer Steinbrück, Germany’s tough-talking SPD finance minister, went before the Bundestag to announce that the global financial system faced a crisis originating in America from which Germany had so far been spared. “America’s laissez-faire ideology,” as practiced during the subprime crisis, “was as simplistic as it was dangerous,” he later told Germany’s parliamentarians. He confidently expected that America would soon forfeit its role as financial superpower. 2 French president Sarkozy chirped along with him. Just returned from New York on September 25, Sarkozy, who had formerly been regarded as a true disciple of Atlantic capitalism, told a crowd in Toulon that “the idea that the markets were always right was mad . . . laissez-faire is finished. The all-powerful market that always knows best is finished.” 3 And just in case anyone wondered where the home of that mad idea was, Giulio Tremonti, Silvio Berlusconi’s outspoken finance minister, boasted that Italy’s banking system would be fine because “it did not speak English.” 4 It was convenient, but it was a self-deception. America’s securitized mortgage system had been designed from the outset to suck foreign capital into US financial markets and foreign banks had not been slow to see the opportunity.

I

Since the 1980s Americans had grown used to the idea that Asians—first the Japanese, now the Chinese—owned their government debt. That was the anxiety that haunted the Hamilton Project. What they did not reckon with was that foreigners owned a large portion of America’s houses. By 2008 roughly a quarter of all securitized mortgages were held by foreign investors. Fannie Mae and Freddie Mac funded $1.7 trillion of their portfolio of $5.4 trillion in mortgage-backed securities by selling securities to foreigners. China was by far the biggest foreign investor in these “Agency bonds,” with holdings estimated at $500–600 billion. 5 But in the riskier segment of the securitized mortgage business it was Europeans, not Asians, who led the way. 6

For nonconforming high-risk MBS, those not backed by Fannie Mae or Freddie Mac, the share held by European investors was in the order of 29 percent. 7 In 2006, at the height of the US mortgage securitization boom, a third of newly issued private label MBS were backed by British or European banks. 8 The segment of the securitization chain in which European banks were of truly crucial importance was also the weakest link in the chain, ABCP. In the summer of 2007, though it was Citigroup that had the largest off balance sheet SIV exposure, it was European banks that dominated the market. Overall, two thirds of the commercial paper issued had European sponsors, including 57 percent of the dollar-denominated commercial paper. Europe’s banks had good standing with the ratings agencies, but they did not have large dollar-denominated depositor bases. If they wanted to get in on the MBS boom, they needed to go to the wholesale market.

Among the European sponsors, German financial institutions were particularly prominent, and what was remarkable was the kind of German bank that was involved. Germany’s giant, Deutsche Bank, was a leading player on Wall Street. It is not for nothing that it featured as prominently as it did in Michael Lewis’s bestselling narrative of the crisis, The Big Short , or in the subsequent Senate investigation. 9 Dresdner Bank, Germany’s number two, was also heavily involved in the United States. But it was Germany’s smaller regional banks, the Landesbanken, that threw themselves head over heels into the American adventure. In the early 2000s, at the insistence of Brussels, the Landesbanken were stripped of the local state guarantees that lowered their funding costs. They responded by taking a punt on adventurous financial engineering. Banks from the former industrial heartland of Germany, such as Sachsen-Finanzgruppe, WestLB and IKB of Düsseldorf, took huge gambles on real estate investments in the United States. At least four German sponsors—Sachsen, WestLB, IKB and Dresdner—had ABCP exposure large enough to wipe out their equity capital several times over.

ABCP Sponsor Location and Funding Currency (in $ millions)

|

Currency / Sponsor location |

US dollars |

Euro |

Yen |

Other |

Total |

|

Belgium |

30,473 |

4,729 |

0 |

0 |

35,202 |

|

Denmark |

1,796 |

0 |

0 |

0 |

1,796 |

|

France |

51,237 |

23,670 |

228 |

557 |

75,692 |

|

Germany |

139,068 |

62,885 |

0 |

2,566 |

204,519 |

|

Italy |

1,365 |

0 |

0 |

0 |

1,365 |

|

Japan |

18,107 |

0 |

22,713 |

0 |

40,820 |

|

Netherlands |

56,790 |

65,859 |

0 |

3,116 |

125,765 |

|

Sweden |

1,719 |

0 |

0 |

0 |

1,719 |

|

Switzerland |

13,082 |

0 |

0 |

0 |

13,082 |

|

United Kingdom |

92,842 |

62,298 |

0 |

3,209 |

158,349 |

|

United States |

302,054 |

0 |

0 |

2,996 |

305,050 |

|

Total |

714,871 |

219,441 |

22,941 |

12,444 |

969,697 |

Source: Viral V. Acharya and Philipp Schnabl, “Do Global Banks Spread Global Imbalances? Asset-Backed Commercial Paper During the Financial Crisis of 2007–09,” IMF Economic Review 58, no. 1 (2010): 37–73, figure 15. Based on data from Moody’s.

Nor did European banks confine themselves to dealing in the securities. The Europeans went native, joining their American counterparts in integrating down the supply chain so as to control mortgage origination itself. After all, if a Wall Street investment bank could do it, why not a European bank with some experience in retail banking? From the mid-1990s banks like Britain’s HSBC aggressively bought into the American mortgage market. By 2005 HSBC could boast of having serviced 450,000 mortgages to a total value of $70 billion. 10 Credit Suisse built an American mortgage-servicing department that fed one of the largest ABS CDO operations of the early 2000s. 11 Deutsche Bank had close relationships with the giant mortgage-generating machines at Countrywide and AmeriQuest. In 2006 the German bank bought the subprime specialists MortgageIT Holdings and Chapel Funding LLC. As a Deutsche Bank press release glowed, ownership of these operations at the bottom of the US credit pyramid would “provide significant competitive advantages, such as access to a steady source of product for distribution into the mortgage capital markets.” 12 From the point of view of generating high-yielding CDOs, it was precisely the bottom of the mortgage barrel that was most attractive.

II

How was this possible? It was easy enough to understand how China acquired claims on the United States. It had a gigantic trade surplus, the dollar proceeds of which were bought up by its financial authorities and invested in US Treasurys, giving rise to Larry Summers’s scenario of a “balance of financial terror.” But among those who worried about global macroeconomic imbalances, Europe was rarely mentioned. The EU current account surplus with the United States was modest compared with that of China. With the world as a whole, Europe’s current account was in modest deficit. The Europeans did not peg their currencies against the dollar. There was no agency in Brussels accumulating foreign assets as part of a currency stabilization effort, no German sovereign wealth funds. So how did European banks end up owning such a large slice of American mortgage debt?

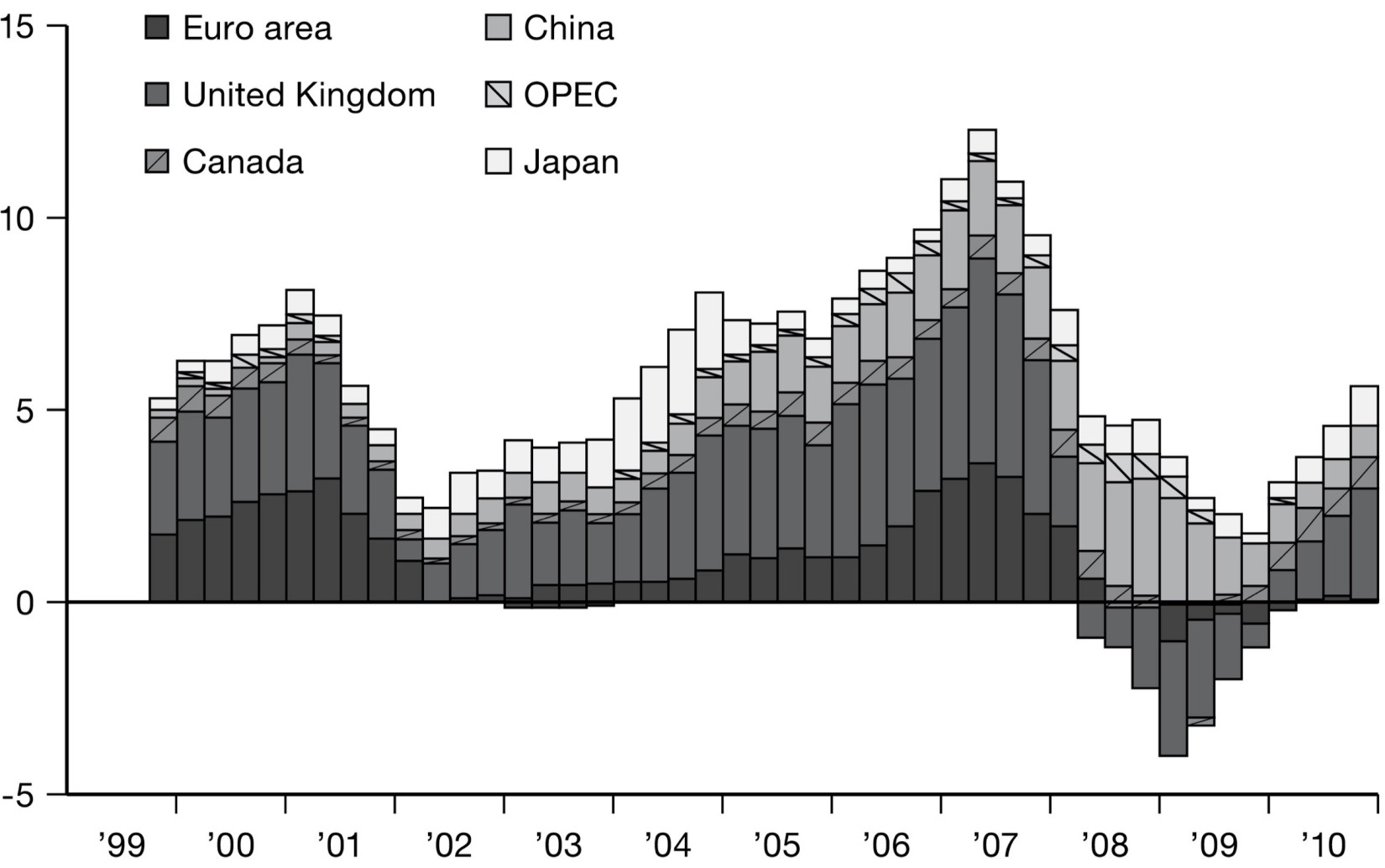

The answer is that European banks operated just like their adventurous American counterparts. They borrowed dollars to lend dollars. And the scale of this activity is revealed if we look not at the net flow of capital in and out of the United States (inflows minus outflows), which has its counterpart in the trade deficit or surplus, but at the gross flows, which record how many assets were bought and sold in each direction. As the gross inflow data show, by far the largest purchasers of US assets, by far the largest foreign lenders to the United States prior to the crisis, were not Asian but European. Indeed, in 2007, roughly twice as much money flowed from the UK to the United States as from China.

Gross Capital Flows to the US by Region (% US GDB)

Source: Claudio Borio and Piti Disyatat, “Global Imbalances and the Financial Crisis: Link or No Link?,” BIS Working Paper 346 (2011), graph 6.

Before 2008 the net financial flow from Asia to the United States could reasonably be construed as the financial counterpart to America’s trade deficit with Asia. By contrast, the financial flows between Europe and the United States made up a financial circulatory system quite independent of the trade connections between the two. Across the Pacific, from Asia to the United States, money flowed one way. In the North Atlantic financial system it flowed both ways, both in and out of the United States. This was in the logic of the market-based banking model. Europe’s banks did not have branches spread across the United States. But a Wall Street firm like Lehman didn’t either. This was the beauty of the market-based model of banking. You borrowed the dollars on Wall Street to fund your holdings of mortgages from all over the United States.

The ABCP market was a showcase for this transatlantic system. The ABCP conduits organized bundles of securitized assets from the United States and Europe. 13 With those securities as collateral they then issued short-term commercial paper, which was bought by the managers of cash pools in the United States. In 2008, $1 trillion, or half of the prime nongovernment money market funds in the United States, were invested in the debt and commercial paper of European banks and their vehicles. 14 A large portion of this simply moved from one office on Wall Street to another, with one address being adorned with the name of a European bank. But hundreds of billions of dollars took a more circuitous route. They flowed out of the United States from the branches of foreign banks in New York to the head offices of European banks, from which they returned for investment in the United States, sometimes by way of an offshore tax haven such as Dublin or the Cayman Islands. 15 It was the spinning motion of this transatlantic financial axis that impelled the surge in financial globalization in the early twenty-first century.

In managing these flows, the multicurrency balance sheets of European banks played a crucial role. To understand the nature of these flows, take the example of a German bank keen to participate in the lucrative American mortgage business. The bank did not have an existing depositor base in dollars. Its existing liabilities—deposits, bonds issued and short-term borrowing—were in euros. This meant that the German bank had a funding problem if it wanted to lend in dollars. But in that respect it was no different from a Wall Street investment bank. To participate in the profitable American securitization wave, European banks exchanged part of their euro funding for dollars (option 1), holding a long dollar position or hedging by way of swap agreements (option 2). Or the German bank could borrow directly in the United States (option 3), for instance from an American money market fund eager to earn slightly more than the returns offered by Treasurys, now that the Chinese were buying them. The result would be a German bank with a balance sheet that featured liabilities and assets of different maturities and denominated in a variety of currencies. And its counterparts would include a bank or other business that had lent dollars in exchange for euros (if it had chosen funding options 1 or 2), or an American money market fund holding dollar-denominated debt issued by a German bank (option 3). In the national balance of payments statistics one would see both borrowing from and lending to America happening within the accounts of the same bank. One could net the flows out to identify how much, on balance, flowed one way rather than the other, but that would give no idea of the scale of the commitments on each side. It would be akin to noting that two elephants on either end of a circus seesaw leave a net balance of zero. It would be true, but it would not be a very adequate description of the forces in play.

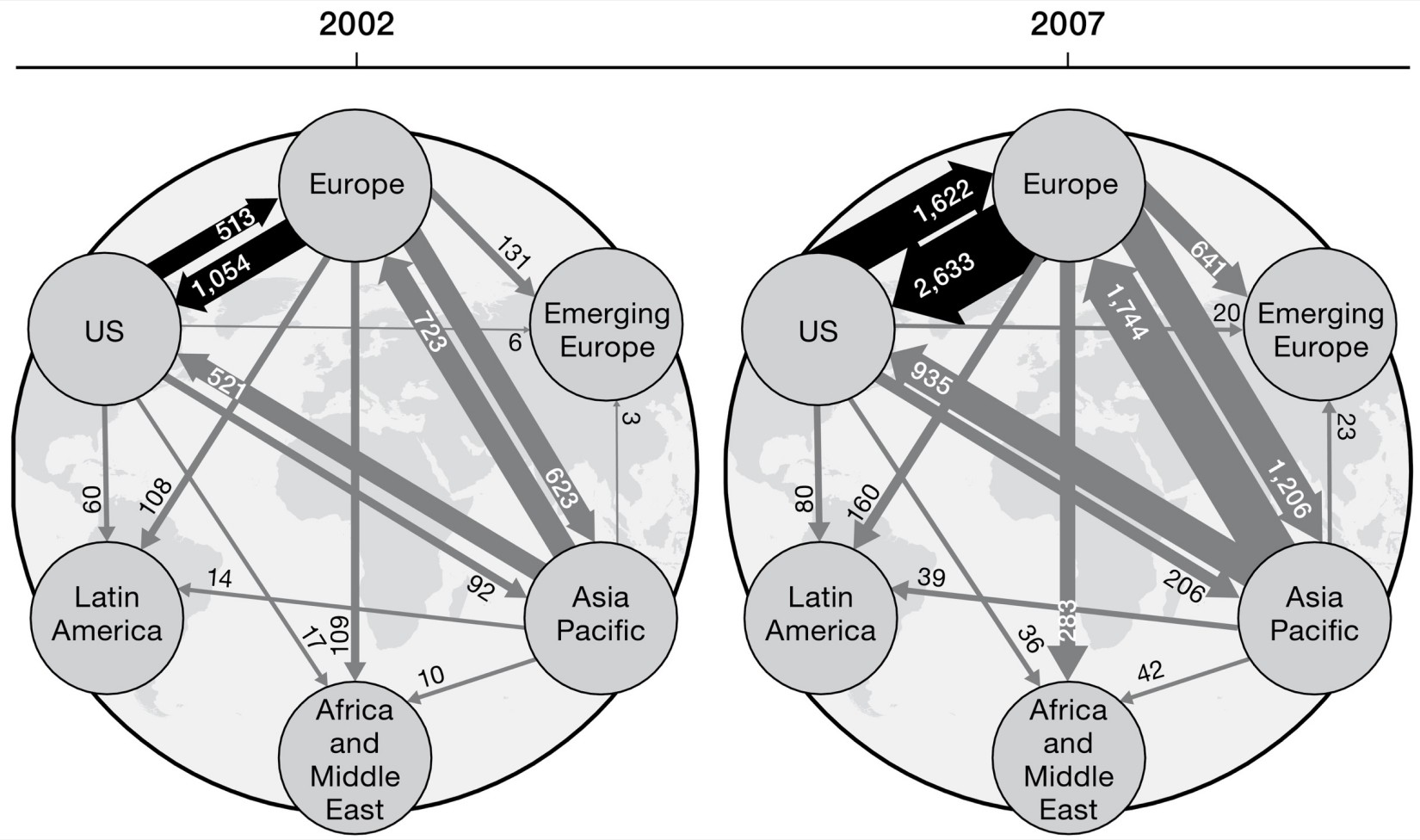

Financial Globaliszation Revolves Around Europe: Cross-Border Bank Claims (in $ billions)

Note: The thickness of the arrows indicates the size of the outstanding stock of claims. The direction of the arrows indicates the direction of the claims: Arrows directed from region A to region B indicate lending from banks located in region A to borrowers located in region B.

Source: Stefan Avdjiev, Robert N. McCauley and Hyun Song Shin, “Breaking Free of the Triple Coincidence in International Finance,” Economic Policy 31, no. 87 (2016): 409–451, graph 6.

The rise of China dominated contemporary perceptions of early twenty-first-century globalization. And the axis of imbalance that attracted most attention was that between China and the United States. Worries about geopolitics, Larry Summers’s balance of financial terror, Ben Bernanke’s savings glut, all pointed the finger in that direction. But if we map not annual flows but cross-border banking claims, this gives further proof of how one-sided the Sino-American view of the buildup to the crisis was. The central axis of world finance was not Asian-American but Euro-American. Indeed, of the six most significant pairwise linkages in the network of cross-border bank claims, five involved Europe.

European banking claims on the United States were the largest link in the system, followed by Asian claims on Europe and American claims on Europe. European claims on Asia exceeded the much commented upon Asian-American connections. Indeed, West European claims on emerging Eastern Europe alone were more than three times the size of American claims on Asia. It was also noticeable that oil- and gas-rich Middle Eastern investors preferred to channel their funds through Europe rather than directly to the United States. This was a pattern already established in the 1970s and only reinforced by the aggressive politics of Bush’s “War on Terror.” The European financial centers offered a safe channel through which funds from Asia and the Middle East were then sluiced into more speculative investments in the United States. It was not for nothing that China preferred to channel many of its claims on the United States through Belgium. In the process, the European financial system came to function, in the words of Fed analysts, as a “global hedge fund,” borrowing short and lending long. 16

What this suggests is a further crucial development of the argument. If it is misleading to construct our image of financial globalization around the Sino-American trade balance, to imagine it as centered on US securitization with outsiders being “sucked in” misses the point too. In fact, the entire structure of international banking in the early twenty-first century was transatlantic. The new Wall Street was not geographically confined to the southern end of Manhattan. It was a North Atlantic system. The second node, detached from but integrally and inseparably connected to New York, was the City of London. 17 In the nineteenth century, in the age of the gold standard and the British Empire, London had been the capital of global finance in its own right. From the 1950s, the City of London made a new role for itself as the main hub for offshore global dollar financing.

III

In the aftermath of World War II, the Bretton Woods monetary system had sought to restrict speculative capital flows. This gave the US Treasury and the Fed controlling roles. The aim was to minimize currency instability and to manage the global shortage of dollars. But it meant that the US authorities had to operate the kinds of controls that we now associate with China. This was a fetter on private banking. From the 1950s, with connivance of the UK authorities, the City of London developed as a financial center that sidestepped those constraints. 18 British, American, European and then Asian banks too began to use London as a center for unregulated deposit taking and lending in dollars. Among the first to avail themselves of these “eurodollar” accounts were Communist states that wanted to keep their export earnings safe from meddling by the US Treasury. They set a trend. By the 1960s eurodollar accounts in London offered the basic framework for a largely unregulated global financial market. As a result, what we know today as American financial hegemony had a complex geography. It was no more reducible to Wall Street than the manufacture of iPhones can be reduced to Silicon Valley. Dollar hegemony was made through a network. It was by way of London that the dollar was made global. 19

Driven by the search for profit, powered by bank leverage, offshore dollars were from the start a disruptive force. They had scant regard for the official value of the dollar under Bretton Woods and it was the pressure this exercised that helped to make the gold peg increasingly untenable. When the final collapse of Bretton Woods coincided in 1973 with the surge in OPEC dollar revenue, the rush of offshore money through London’s eurodollar accounts became a flood. By the early 1980s both Britain and the United States had abolished all restrictions on capital movements and this was followed in October 1986 by Thatcher’s “Big Bang” deregulation. The City of London was thrown open to outside investment, sacrificing guildlike structures that dated back centuries to the imperative of creating a genuinely global financial center. Within a decade the UK’s own investment banks had been swallowed by their American and European competitors. 20 American, Asian and European capital flooded in. This involved not only regulatory change and huge financial flows but the physical reconfiguration of the medieval heart of the City of London. To house the gigantic new offices and electronic trading desks needed by global banks, Canadian real estate moguls undertook the construction of a massive new office complex in the abandoned postindustrial docklands of Canary Wharf. In April 2004 Chancellor Gordon Brown ceremonially opened the new Lehman offices at 25 Bank Street. 21 Meanwhile, the emerging hedge fund industry found a comfortable new home in Mayfair, where the American insurer AIG would choose to locate its later notorious Financial Products division.

For many of the most fast-paced global transactions, it was London, not Wall Street, that was the location of choice. By 2007, 35 percent of the global turnover in foreign exchange, running at a staggering $1 trillion per day, was conducted between computer systems in the City of London. 22 European banks were the biggest players in the business. London was also the hub for the over-the-counter (OTC) interest rates derivatives business, a means of hedging against the risk of interest rate fluctuations and an essential complement to repo deals. Of an annual turnover in interest rate derivatives in excess of $600 trillion, London claimed 43 percent, to New York’s 24 percent. 23

A decade after Thatcher’s Big Bang, with Britain’s native banking industry under intense competitive pressure, Tony Blair’s New Labour government set about further streamlining the City’s regulatory system. 24 Nine specialist regulators were combined into a single agency, the Financial Services Authority (FSA). It set a new low bar for financial oversight. Tony Blair’s chancellor, Gordon Brown, boasted that the FSA offered “not only light but limited regulation.” 25 The FSA was mandated to achieve its “goals in the most efficient and effective way.” “[N]ot damaging the competitive position of the United Kingdom” was its top priority. 26 The FSA was required to apply cost benefit analysis to its own interventions and benchmark its operations against other countries. 27 Perhaps not surprisingly, given this mandate, the FSA’s staff was a fraction of that of its US counterparts. As Howard Davies, the FSA’s first chair, put it in the libertarian language of the day: “The philosophy of the F.S.A. from when I set it up has been to say, ‘Consenting adults in private? That’s their problem.’” 28 The sort of thing that you could do in London but not in New York is exemplified by “collateral rehypothecation.”

In a repo, the main flexible source of funds for investment banks, other banks acting as “broker-dealers” took securities as collateral in exchange for cash. What were they to do with their large stockpiles of collateral? Why not use this collateral as collateral in further repo loans, this time on behalf of the broker itself, a so-called reverse repo? In the United States, under regulations that went back to 1934, such rehypothecation of collateral was strictly limited to no more than 140 percent of the collateral being held. In the UK there was no limit on rehypothecation. As a result, according to investigations by a team of analysts from the IMF, the City of London came to function as a “platform for higher leveraging not available in the United States.” The scale of this activity was enormous. According to the IMF team, trading in and out of London the main European and US banks achieved a collateral multiplication of 400 percent, amounting to roughly $4.5 trillion in additional funding, effectively out of thin air. 29

The UK’s liberalization not only freed up UK markets but acted as a crowbar to dislodge regulation worldwide. A transatlantic feedback loop drove regulation down on both sides. 30 The notorious US deregulation decisions taken by the Clinton administration in the late 1990s, which overturned the last remaining financial restrictions of the New Deal era, were not taken in a vacuum. The 1999 law was not called the Financial Services Modernization Act for nothing. There was a distinct vision of modern finance that the US industry was chasing and it was defined by global competition, above all by the City of London. In promoting the legislation, Senator Charles Schumer (D-NY) insisted “the future of America’s dominance as the financial center of the world” was at stake. If Congress did not pass the bill, London, Frankfurt or Shanghai would take over. 31 New York, certainly, stood to benefit, but that should not mislead one into thinking in terms of national champions. No one had been more active in shaping the global marketplace in London than expat American bankers working for the London offices of the major Wall Street firms. What Wall Street wanted was license to bring back home the adventurous practices developed among “consenting adults” in London.

Nor was it only Americans in London. European politicians and cultural critics might be skeptical of freewheeling “Anglo-Saxon” finance. But this downplays the extent to which Europeans coconstructed global finance. From the 1980s onward, Swiss, German, French and Dutch banks began to buy into the City of London with aggressive acquisitions. It was, more often than not, their springboard for a venture into US markets. In 1989 Deutsche Bank acquired Morgan Grenfell Group before buying Bankers Trust in the United States in 1999, and Scudder Investments, a US asset management firm, in 2002. Shortly thereafter, Germany’s leading bank declared English to be its official working language. Credit Suisse was unusual in starting with the acquisition of First Boston in 1990 before reorganizing itself as CSFB in 1996–1997, the same year that it acquired the London firm BZW from Barclays. Germany’s Dresdner Bank bought Kleinwort Benson in 1995 before buying the small but highly influential New York investment bank Wasserstein Perella in 2001. In the 1980s City of London insider Hoare Govett sold out to Security Pacific before being snapped up by the expansive Dutch bank ABN AMRO, which would become the leading European issuer of ABCP before being acquired and dismembered by a pan-European consortium. The Swiss bank UBS-SBC acquired S. G. Warburg in London in 1995. In 1997 it followed this with the purchase of Dillon, Read & Co., an investment bank in New York. After abortive merger talks with Merrill Lynch in 1999, UBS bought out the asset manager PaineWebber. With its fixed-income and currency businesses booming, in June 2004 UBS’s CEO, Marcel Ospel, announced that his ambition was to make the Swiss bank into not only the premier wealth manager but the leading investment bank in the world. 32 UBS never reached that objective, but its giant Connecticut-based office did manage to make the bank into the third-largest issuer of CDO based on private label MBS after Merrill and Citigroup, and the leader in the riskiest mezzanine ABS segment.

All told, in 2007 the City of London was home to 250 foreign banks and bank branches, twice as many as operated out of New York. 33 But the European footprint in Wall Street was very substantial. Of the top twenty broker-dealers in New York, twelve were foreign owned and held 50 percent of the assets. 34 These were the competitors in the top tier. But European financial adventurism came in all shapes and sizes. And it was not confined to the City of London–Wall Street axis. From the 1980s Dublin set out to establish itself as a low-tax, low-regulation jurisdiction, attracting bankers from Europe and North America. A case in point was the German bank Depfa. Founded in 1922 at the time of the Weimar Republic by the government of Prussia to make subsidized housing loans, Depfa moved to Dublin’s International Financial Services Center in 2002 to take advantage of Ireland’s welcoming tax laws. Depfa soon became known across the world as an adventurous financer of infrastructure, providing credits to the Spanish city of Jerez, giving financial advice to Athens and financing a conference center in Dublin and a toll road between Tijuana and San Diego. The Irish-German bank invested the retirement fund of the teachers of the state of Wisconsin, as well as funding Vancouver’s Golden Ears Bridge project. By the time of the crisis, Depfa’s total assets as reported by credit-rating agency Moody’s had swollen to $218 billion, one-third the size of Lehman. 35 This astonishing expansion was not from Depfa’s own resources. It had precious few to begin with. Depfa grew like other market-driven modern banks. It borrowed to lend. And it made handsome profits doing so. So much profit, in fact, that it attracted the attention of Hypo Real Estate, the Munich-based mortgage lender. Hypo was looking to diversify its risk profile and in July 2007 finalized plans to buy out Depfa, taking the combined balance sheet of the two banks to more than 400 billion euros. 36

IV

As they had grown up in the nineteenth and twentieth centuries across the United States and Europe, modern banks had been regional and national in scope. They lived in close and often incestuous relations with national Treasuries, central banks and regulators. The reglobalization of banking unleashed from the 1950s raised basic questions of governance. The original impetus was to create zones of financial activity that were lightly regulated in offshore centers like London. But by the early 1970s at the latest it was clear that this transatlantic financial system had the potential for dangerous instability. 37 Furthermore, the competitive race for profit and market share among the banks in turn unleashed a regulatory race to the bottom. In 1984 Fed chair Paul Volcker proposed new rules to set minimum standards for bank capital, hoping thereby to prevent undercutting of relatively robust banks by less well-capitalized competitors, notably from Japan. For the resilience of a bank in the face of losses on its loan book, capital is the crucial criterion. The more capital a bank has, the more it is able to absorb losses. However, the larger a bank’s book of loans relative to its capital, the higher the rate of return it will be able to offer investors. That was the point of the elaborate legal structures designed to hold securitized assets off balance sheet, to minimize the capital invested and to maximize its leverage. Capital ratios were, therefore, one of the neuralgic points of bank governance. After years of deadlock, in September 1986 the Fed and the Bank of England reached a deal, which in July 1988 finally brought the Basel Committee to agreement on what was known as the Capital Accord, or Basel I. Henceforth, the minimum level of capital that a large international bank should aim to hold against normal business loans was set at 8 percent. 38

Almost as soon as the standard was set, the argument over its definition, implementation and consequences began. If the 8 percent rule had been imposed as a simple percentage, the effect would have been to encourage banks to make the most high-risk investments available in a frantic attempt to milk every cent of profit from every dollar of capital. It would have incentivized risk taking. So the Basel Committee provided for a basic system of risk weights, requiring no capital to be held against the low-risk, short-term debt of governments that were members of the OECD, the exclusive club of rich countries. 39 Mortgages and mortgage-backed securities were also favored with low-risk weights. But at the margin, the system continued to encourage risk taking. Furthermore, the lax provisions of Basel I enabled banks to hold substantial parts of their portfolio off balance sheet in special purpose vehicles (SPV) financed by ABCP. This was one of the main reasons why European banks were so active in ABCP. Their national regulators interpreted Basel I in such a way as to allow them to hold hundreds of billions of dollars of securities and fund them with short-term commercial paper, without needing to commit much of their capital. Not only was their capital stretched thin but the maturity mismatch was terrifying.

The obvious inadequacies of Basel I set in motion the search for a new framework that finally emerged in 2004 with the Basel II accord. But the transition from one regime to the other was telling. Whereas Basel I had been a conventional regulation aiming to impose standards on the industry from the outside, the chief ambition of Basel II was to align risk regulation with “best business practice” as defined by the bankers themselves. Basel II did require off balance sheet risks to be brought onto the banks’ own accounts. But at the same time, they were encouraged to apply their own risk-weighting models to those assets to decide how large their capital buffer needed to be. Far greater reliance was placed also on the credit evaluations issued by the private credit rating agencies. 40 Though Basel II notionally maintained the 8 percent capital requirement, once the big banks applied their proprietary risk-weighting models, they found that they could sustain larger balance sheets than ever before. Under Basel I mortgage assets had been rated as relatively safe and counted only 50 percent for purposes of calculating the necessary capital. Rather than tightening those regulations as a way of moderating the real estate boom, Basel II cut the capital weight of mortgage assets to 35 percent, which made it far more attractive to hold high-yielding mortgage-backed assets. 41 Precisely as the private label securitization boom was about to accelerate, the regulations lightened. 42

One method of massaging the figure down was to purchase default insurance against risky assets in the portfolio. The key supplier of default insurance for “regulatory capital relief” was the American insurance giant AIG and its Financial Products offices in London and Paris. By the end of 2007 it was providing insurance for $379 billion in assets held by major European banks, led by ABN AMRO ($56.2 billion), Danish bank Danske ($32.2 billion), German bank KfW ($30 billion), French mortgage lender Crédit Logement ($29.3 billion), BNP Paribas ($23.3 billion) and Société Générale ($15.6 billion). 43 AIG’s insurance allowed them to save a total of $16 billion in regulatory capital, further increasing leverage, profits and bonus payments. 44

Rather than imposing intrusive inspections and external audits, Basel II placed heavy emphasis on self-regulation, disclosure and transparency. “Well-informed” market judgments would do the work of oversight better than “arbitrary” regulatory decisions. After all, rational investors could have no interest in exposing themselves to the risk of catastrophic loss, or so the reasoning went. They would price bank shares accordingly, sending a clear signal as to which banks were safe and which were not. The regulators were utterly subservient to the logic of the businesses they were supposed to be regulating. The draft text of what would become the Basel II regulations was prepared for the Basel Committee by the Institute of International Finance, the chief lobby group of the global banking industry. 45

Nor was the Basel framework well designed to drive standards upward. Both Basel I and Basel II enshrined the principle of “home country rules.” This required signatories to the system to accept the regulations of all other parties as adequate. So banks from lax areas of supervision were free to operate according to their domestic norms in lucrative American and European markets. By the same token, it excused the City of London and New York from responsibility for onerous oversight of the hundreds of foreign banks that congregated in their precincts. 46 The Fed further amplified the effect by declaring in January 2001 that the US banking operations of foreign financial holding companies that were considered adequately capitalized in their home countries would not need to meet separate capital adequacy rules in the United States. 47 Despite the huge scale of their American operations, the European banks were not required to hold adequate capital actually in the United States.

Not surprisingly, given how forgiving its provisions were, European regulators encountered little resistance as they pushed ahead to implement Basel II. It was a framework that Europe’s expansive banks could happily live with. The SEC and the New York Fed, which oversaw America’s investment banks, took a similar view. Tellingly, it was the FDIC, the American deposit insurance agency that oversaw medium and small American banks, that raised objections. The FDIC’s chair, Sheila Bair, an outspoken midwestern Republican appointee, was incredulous that big banks were effectively being given license to “set their own capital requirements.” 48 It would give them a huge competitive advantage over their smaller competitors. The FDIC estimated that the introduction of Basel II would permit big banks to reduce their capital by 22 percent. In 2006 Blair threw whatever political weight she could muster into a delaying action. With Bernanke as the new Fed chair she negotiated a compromise under which the short-term reduction in capitalization due to the introduction of Basel II should not exceed 15 percent per bank before 2011. 49 Partly, as a result, if we take leverage—the ratio of bank balance sheet to bank capital—as the basic indicator of banking risk, a considerable gap emerged between the United States and the Europeans ahead of the crisis. According to the calculations of the Bank for International Settlements (BIS), Deutsche Bank, UBS and Barclays, three of the most aggressive European players in global financial markets, all boasted leverage in excess of 40:1, compared with an average of 20:1 for their main American competitors. In 2007, even before the crisis struck with full force, leverage at Deutsche and UBS touched 50:1. 50 Even allowing for differences in the ways in which Europeans and Americans account for bank balance sheets, the gap was significant.

To the American banks this did not seem fair. In response their industry lobby pushed hard to level the playing field. In February 2007 New York mayor Michael Bloomberg traveled to London, where he met with the chair of the UK’s FSA, and used the London platform to lobby for further deregulation in the United States. “The FSA is an example of the kind of streamlined and responsive regulatory framework Congress must implement if New York City is to remain the financial capital of the world,” the mayor intoned. Bloomberg wasn’t the only one making the trip. That same month the Financial Times reported that Citigroup had “reshuffled its management in a move that gave greater influence to London-based executives, with five receiving global responsibility for their areas and the global head of commodities moving to London. Merrill Lynch, J.P. Morgan and Lehman Brothers also gave global management roles to executives based in the UK.” 51 It was with these pressures in mind that Bloomberg and Senator Charles Schumer in May 2007 put their names to a McKinsey & Company report warning that New York’s position as the world’s leading financial center was under threat unless it fell into line with international standards. “The findings are clear: . . . our regulatory framework is a thicket of complicated rules, rather than a streamlined set of commonly understood principles, as is the case in the United Kingdom and elsewhere.” 52

Of course at every stage in the construction of global capital markets, think tanks, economists and lawyers contributed ideas and argumentation to justify the next move. Technological change gave banks massive new information-processing capacity. The complex financial instruments they produced exuded an energizing charisma. 53 The clannish society of the bankers created a social force field of common assumptions and an overweaning superiority complex. They were the masters of the universe. They could not fail. But the basic driver of expansion and change was the competitive search for profit, played out in the force field of financial engineering, transnational capital movement and competitive deregulation between Wall Street, the City of London and Basel. It was not that the key players were completely oblivious to risk. But they believed in their capacity to manage it and were totally committed to maximizing the rate of return. So every regulation and every restriction on leverage was subject to second-guessing and subversion by the overwhelming force of competition and the unfettered movement of capital that had been gathering steam since the 1960s.

What if the regulations failed? What if there was a comprehensive crisis of the transatlantic financial system? No one wanted to ask that question. In the rescue of the emerging markets in the 1990s it was Washington that had taken the lead. The US Treasury and the IMF acted in concert. Though they had faced determined criticism and foot-dragging from the Europeans, their resources were up to the task of bailing out Mexico or South Korea. 54 Would that be the case if it were the transatlantic financial system that suffered a circulatory failure? The sums involved were enormous, denominated not in the billions or even hundreds of billions but in trillions. In the last instance, US banks could expect support from the bottomless resources of the Fed. But the question was particularly pressing for European banks operating a multicurrency balance sheet. In case of emergency, where would they get the dollars they needed? Who would be their lender of last resort?

The global Financial Stability Forum (FSF), a group set up in the wake of the 1990s financial crises, had been edging around the question since 2000. At the Bank of England, John Gieve was keen to run “table exercises” to game the scenario of a major international banking failure. But he met with little enthusiasm. Bank of England governor Mervyn King, a thoroughbred macroeconomist, was little interested in the technical issues of financial stability. “There was no real appetite on the US side to get into discussing particular examples. We were offering to put HSBC or Barclays on the table, with real balance sheets, and maybe in return, they would do Citi or Lehman. But that never got off the ground.” 55 Would Europe’s central banks have the dollar reserves necessary to backstop the European financial system? It was an old-fashioned question, seemingly out of season in a world of limitless global liquidity. 56 But when the question was put by analysts from the BIS, the answer was sobering. In the balance sheets of the European banks at the end of 2007 there was a mismatch between dollar assets (lending) and dollar liabilities (funding by way of deposits, bonds or short-term money market borrowing) of $1.1–1.3 trillion. 57

The only central banks that held these kinds of sums were in China and Japan. Against the backdrop of a sanguine view about financial markets, their “hoarding” of dollars was widely seen as a sign of insecurity, an aftereffect of the trauma of the 1997 crisis. 58 It is telling that no one troubled to ask the question of what the adequate level of reserves would be for a European country with a gigantic globalized banking system. As it turns out, given the scale of the banking business in their jurisdictions, the level of foreign exchange reserves held by the Swiss and British central banks was astonishingly low—less than $50 billion each. To backstop the sprawling banking system of the eurozone, the European Central Bank had little more than $200 billion on hand. What did this say about their assumptions about both financial risk and financial sovereignty? When asked later how he justified such minimal reserve holdings prior to the crisis, one of the most outspoken central bankers of the period paused for a minute, smiled at a point well taken and then said quite simply: “Given our long history of relations with the Fed, we didn’t expect to have any difficulty getting hold of dollars.” In other words, there was a presumption that collaboration would be forthcoming and in an emergency the Fed would provide Europe, and London in particular, with the dollars it needed. Given the scale of the offshore dollar business there could be no other answer. But for that same reason, it was also an astonishingly audacious assumption, an expectation so exorbitant that it was better left unspoken.

Chapter 4

EUROZONE

I f Europe preferred not to highlight its role in the “American” financial crisis of 2008, covering its tracks was made easier by the fact that from 2010 Europe was consumed by its own “authentically” European crisis. The eurozone crisis followed directly on the footsteps of Wall Street and the US mortgage bust. But as conventionally understood, it is as if the Wall Street crisis and the eurozone disaster belong to different worlds. Whereas the US crisis involved overextended banks and mortgage borrowers impelled by greed and financial excess, the eurozone crisis would revolve around quintessentially European themes of public finance and national sovereignty. It would pit Greeks against Germans and reawaken memories of World War II. Both crisis narratives play to type: mercenary Americans, squabbling European nationalisms. But was it merely bad luck that the two crises followed so closely upon each other? Was it merely bad luck that the same banks were involved in both? If the buildup to the American crisis was less all-American than is generally credited, how “European” were the problems of the eurozone?

I

As the twenty-first century began, the Europeans could certainly be forgiven for being preoccupied with questions of politics and institution building. With the introduction of the euro as a single currency between 1999 and 2002 and the expansion of the EU to include much of Eastern Europe in 2004, they were embarked on truly dramatic experiments, which were driven as much by political and geopolitical considerations as by economics. 1

As far as the euro is concerned, the story again goes back to the early 1970s and the collapse of Bretton Woods. Between 1945 and 1971, the Europeans did not have to worry about intra-European currency issues. The dollar tied to the gold reserve in Fort Knox was the anchor of the global system. Once Nixon abandoned the gold peg in August 1971, Europe faced a problem. Fluctuating exchange rates would disrupt the tightly integrated trading networks that had brought Europe together. On the other hand, efforts to create a zone of exchange-rate stability by pegging the European currencies against one another reopened the basic question of power. In a European Monetary System, whose currency would replace the dollar as the anchor, as the “key currency”? The stresses might have been manageable if capital movement had been constrained, limiting speculative attacks. But by the early 1980s the freewheeling habits of the eurodollar business had become the global norm. Huge surges of hot money between currencies put extreme pressure on the more financially fragile states and conferred an intolerable degree of influence on Germany’s conservative central bank. From the early 1970s the Budesbank’s anti-inflationary stance and the resulting strength of the Deutschmark constrained not only Germany’s own government in Bonn but the governments of all of the rest of Europe too. By 1983 even France’s Socialist administration under François Mitterrand was forced to give in. After a series of messy devaluations between 1981 and 1983, Paris abandoned its effort at social democracy in one country and adopted instead a hard-currency policy of “franc fort.” Interest rates would be set at whatever level was necessary to hold the franc against the Deutschmark, even if that meant borrowers paying 18 percent or more. Far from seeking to restrict capital movement, European officials at international organizations like The OECD pushed for further liberalization. The pressures generated by unrestricted capital movements across Europe’s fixed exchanges in turn provided a powerful argument for those who favorerd ever closer European integration. 2 How else were the weaker members of the European Monetary System to regain even a modicum of control over the conduct of monetary policy? By the late 1980s plans were afoot, driven above all by Jacques Delors, the president of the European Commission, and his supporters in the French Socialist Party, for another round of negotations over monetary integration. Given the national interests at stake those would most likely have gone nowhere had it not been for the sudden end to the cold war. The fall of the Berlin Wall in 1989 and German chancellor Helmut Kohl’s irresistible push for national reunification threatened to make Germany even more dominant. A currency union and irrevocable economic unification seemed to both Kohl and Mitterrand the best way of securing a much larger Germany in a peaceful and stable continent. 3 As a price of surrendering the Deutschmark, the Germans exacted the promise that the new European Central Bank would continue the conservative heritage of the Bundesbank. But a joint central bank board would give a voice to all the other member states, and monetary union would end the ruinous cross-country pressure exercised by financial markets.

It was a spectacularly ambitious undertaking. The monetary union came into full effect in 2001. There was a single European central bank. There were fiscal rules limiting deficits and setting debt ceilings (known as the Stability and Growth Pact). But the euro was clearly unfinished. 4 There was no unified economic policy. No unified regulatory structure for banking. Nor, however, was there much urgency in moving to further integration. In its early years, the new currency zone performed tolerably well. European growth accelerated. After an initial hike in prices following the adoption of the single currency, inflation remained moderate. Capital markets were calm.

Despite this benign atmosphere, there were two problems that preoccupied experts both inside and outside the eurozone. The first was whether preexisting imbalances in intra-European trade would narrow or expand over time. 5 The fear was that the lack of currency adjustment could lead to cumulative divergence as less competitive regions fell further and further behind. Second, there was the risk of asymmetric external shocks. 6 A bust in tourism would hurt Greece far more than Germany. A collapse in Chinese import demand would damage Germany in a way that it would not hurt Ireland. American critics, in particular, warned that Europe’s labor markets did not have the flexibility or mobility of their American counterparts. 7 And if people would not move, faced with a crisis, Europe would need a common system of benefits, taxes and spending to allow funds to flow from the more prosperous to the more hard-hit regions. Along with labor mobility, it was this backbone of social security, disability and unemployment benefits that held the gigantic diversity of the US economy from Alabama to California together. Worryingly, there was plenty of self-congratulation in Brussels in the early 2000s but little urgency about building the overarching mechanism of fiscal redistribution and burden sharing that would be necessary to see the eurozone through a recession, let alone a major financial crisis.

Getting to the moment of unification had required huge efforts from many members of the eurozone. Italy, in particular, imposed severe belt tightening. 8 The collective effort of the 1990s to stabilize Italy’s finances shaped a generation of Italian technocrats and politicians who would go on to play a key role in European politics, among them Mario Monti, economist, EU commissioner and future prime minister of Italy, and Mario Draghi, the future head of the ECB. 9 It was another Italian economist, Romano Prodi, who as president of the commission oversaw the introduction of the new currency. But having mastered Italy’s acute financial political crisis of 1992–1993 and achieved euro membership, there was little energy left in Rome for further initiatives. The victory of Silvio Berlusconi’s Forza Italia in the 2001 elections was a sign of the times. Far from making progress toward further European integration, holding the line on the budget criteria set in the Maastricht Treaty was hard enough. In 2003 France and Germany both exceeded the agreed limit of a 3 percent budget deficit, but Brussels shrank from imposing sanctions on such heavyweights. To fiscal disciplinarians this raised the alarm. Would the EU’s central institutions ever have the political courage to impose themselves on larger members? For others the more pressing question was what was wrong with Germany.

Germany’s entry into the euro did not go well. The other members made sure to settle on competitive exchange rates against the Deutschmark. Germany’s exports took a hit. Its rule-busting budget deficits reflected its anemic growth. The world’s media labeled Germany the “sick man of Europe.” 10 Germans themselves talked of a “blockierte Gesellschaft” (blocked society). 11 The response from Gerhard Schroeder’s Red-Green coalition, which governed Germany from 1998 to 2005, was unexpectedly energetic. For years Germans had suffered from painfully high levels of long-term unemployment, exacerbated by the sudden deindustrialization of the former GDR. In 2005 joblessness would peak at 10.6 percent. To combat this scourge, between 2003 and 2005 the Schroeder government announced a national restructuring program titled Agenda 2010. Its main thrust was a multiphase program of labor market liberalization and benefit cuts, designed by a committee headed by VW’s head of human resources, Peter Hartz. 12 The fourth and final phase of cuts, Hartz IV, became synonymous with a new German “reform” narrative. The unemployed were returned to work. Wage restraint restored German competitiveness. The reward came already in 2003 when Germany could boast of being the world export champion (Exportweltmeister).

Agenda 2010 would come to define a new bipartisan self-understanding of Germany’s political class. 13 Having accomplished the enormous task of reunification, Germany had overcome its internal difficulties and “reformed” its way back to economic health. It is a narrative that is superficially compelling and it would have significant implications for how Berlin approached the crisis of the eurozone, but it does not withstand close scrutiny. Hartz IV certainly drove millions of people more or less willingly off long-term unemployment benefits into a range of insecure jobs. This helped to hold down wages for unskilled workers, such as cashiers and cleaning workers. In the first ten years of the euro, despite soaring productivity, half of German households experienced no wage growth at all. This shortened unemployment rolls. It also increased pretax inequality and lowered Germany’s wages relative to its European neighbors. But as to the competitiveness of German exporters, the significance of Hartz IV is far less obvious. 14 German companies do not win export orders by shaving the wages of unskilled workers. A far more important source of competitive advantage came from outsourcing production to Eastern Europe and Southern Europe. Added to which there was the boost from the global recovery of the early 2000s.

While its economic impact has been exaggerated, what Hartz IV did transform was German politics. The blue-collar electorate and the left wing of the SPD never forgave Schroeder for Hartz IV. 15 The left wing split from the SPD to unify with the former Communists of the East. The result was a new party known as Die Linke, which gathered almost 10 percent of the electorate. Together, Die Linke, the SPD and the Greens were a powerful political force. Red-Red-Green was capable of winning a majority. But the bitter divisions between them over Agenda 2010 made a broad-based center-left coalition difficult to imagine. The result was to hand the political initiative to their opponents. The decisive force in European politics for the next decade and beyond would be German Christian Democracy and its leader, Angela Merkel.

Merkel has come to be seen as the figurehead of Europe’s political center—oscillating between conservative stances on economic and financial policy and cultural modernization. 16 When she first emerged on the political scene her profile was harder edged. In the 2005 election that brought her to power, Merkel ran on a strong promarket platform. It was unpopular and she subsequently softened her stance. But there is little doubt that the 2005 agenda expressed the chancellor’s basic personal vision. It can be summarized in three numbers: 7, 25 and 50. As Merkel is fond of pointing out, Europe has 7 percent of the world’s population and 25 percent of global GDP. But it is responsible for 50 percent of global social spending. 17 This, as Merkel sees it, is not sustainable. Germany’s growth is steady, but slow at best. Germany’s population, along with that of much of Europe, is aging. What has to give is government spending. Fiscal consolidation is the deep continuity of Merkel’s administrations. As she announced in her first speech at Davos in January 2006: “To understand the social market economy as a NEW social market economy in the twenty-first century we must first of all reorder the priorities of politics toward an understanding of politics that is directed ahead, toward future generations. For us in Germany that means first of all clearing up our financial situation, our budgets. We have a demographic problem. We know that we have too few young people and nevertheless we live at the expense of the future by running up debts. That means that we rob future generations of their room for investment and development and that is immoral.” 18

Needless to say, this was music to the ears of business lobbyists concerned to see taxation and state spending held in check. But Angela Merkel’s first government was a grand coalition with the defeated SPD. 19 Fiscal consolidation, like Hartz IV, commanded a consensus across the center ground of German politics. The finance ministry was claimed by Peer Steinbrück, an acolyte of the legendary SPD chancellor of the 1970s and 1980s, Helmut Schmidt. 20 Steinbrück was profoundly committed to a supply-side, anti-Keynesian vision of economic policy. For him restoring “fiscal room” was not merely a matter of financial stability. The ossification of the government budget under the impact of quasi-automatic entitlement spending and interest payments was indicative of a broader problem affecting the developed world: the crisis of democratic politics and democratic participation. What choice could political parties offer to voters if the room for budgetary maneuver was restricted by “entitlement spending,” debt service and low tax rates to 1 percent of GDP one way or another? One could of course go the route of the Cheney wing of the Republicans and simply blow up the deficit. But if one was not willing to take that risk, one was forced into the center ground. In a proportional representation system like Germany’s, this led to disaffection among the voters and the splintering of the party political landscape, with the once-dominant CDU and SPD huddling together in the center. Merkel’s grand coalition was indicative of the impasse. It was not for nothing that “postdemocracy” became one of the buzzwords of German political discussion in the early 2000s. 21 For Steinbrück, paradoxically, present-day discipline was a promise of freedom to come.

Beyond these high-minded considerations, German fiscal strategy was also driven by more basic calculations of electoral advantage. Over the two decades since unification, West Germany had poured more than a trillion euros into reconstruction and regional subsidies for the East. 22 In 2005–2006, as Merkel’s grand coalition took office, the mood in the western Länder, and particularly the rich southern states, was resentful. They had been conscripted into a gigantic act of solidarity with the East. Now they had had enough. Capping deficits was a not-so-covert promise to the rich southern states to rebalance priorities away from the needy and indebted eastern and northern members of the Bund. Fatefully for the future of the eurozone, the problem of fiscal control was cast by German politics already from the early 2000s as one of equity within a federal transfer union. Well before the Greek crisis broke, the most prosperous regions of West Germany had made clear their refusal to take responsibility for other people’s debts, German or otherwise. The argument that the debts “shouldered by the West” to pay for spending “in the East” had generated huge orders for West German business—in effect exports within Germany from West to East—cut no ice. After 2010 the same argument would cut no ice at the European level either. What the most influential voters and voices in German public opinion wanted was simple: discipline all around. In 2006 a commission was set up to devise a new federal fiscal settlement. The idea, following the Swiss example of 2001, was to adopt a “debt brake” to block any further expansion of debt at the Bund, Länder or Commune level. Hammering out the multilevel political deal was slow work. But Steinbrück and the Federal Ministry of Finance were sanguine. As the global economic horizon began to darken in 2007–2008, the German finance ministry was projecting a budget surplus by 2011. 23

Of course, national politics and the drama of reunification gave a particular hue to the German discussions. But there is no need to construct a new narrative of the peculiarities of German history, or to search for some particular German trauma that will explain Berlin’s newfound preoccupation with fiscal rectitude. In fact, there are striking similarities between the debates in Germany and those in Rubinite circles in the United States. On both sides of the Atlantic, globalization, competitiveness and fiscal sustainability were key issues. Nor should this be surprising. The rise of China and the funding problems of the modern welfare state were common challenges. The Bush administration might have been political poison in Europe. But in the late 1990s, Clinton’s Democrats had been an inspiration for Gerhard Schroeder’s Red-Green coalition. 24 Merkel was nothing if not an Atlanticist. But if there was a common agenda, there were common blind spots too. For all the focus in the eurozone on the need to make labor responsive to the demands of global competition, for all the calls for common fiscal discipline, there was an almost total lack of recognition of the destabilizing forces unleashed by global finance. In Europe, as in the United States, it was politicians, workers and welfare recipients who were seen as the problem, not banks or financial markets.

II

If Europe did not have a common fiscal policy or labor market policy, it did at least have a common monetary policy. Its guardian was the ECB, headed from November 2003 by Jean-Claude Trichet. 25 This was precisely the bargain that Mitterrand had hoped for: a Frenchman in charge of Europe’s money. But the other side of the bargain was that the ECB’s operational DNA came from the Bundesbank. And Trichet was perfectly suited to play this dual role. He was a deeply conservative former head of the Banque de France. The ECB’s independence was his highest value and he guarded it jealously. The ECB’s constitution provided plenty of safeguards. Its deliberations were shielded from public scrutiny by minimal transparency requirements. To prevent it from being put to work as a vehicle of fiscal policy, it was banned from monetizing newly issued government debt. Unlike the Fed, which had a dual mandate for price stability and maximum employment, the ECB had price stability as its only target.

All this made the ECB the most remote of all the modern central banks. 26 To call it apolitical would be a misnomer, because it, in fact, entrenched a conservative bias against inflation as the unquestionable doxa of Europe. Nor would it be fair to say that anti-inflation politics were the ECB’s only ambition. It also wanted to promote Europe as a financial center and the euro as a reserve currency, and that meant actively developing European debt markets. Specifically, it meant importing to Europe the American model of a repo market for government debt. Being able to repo government securities made them much more attractive as assets. This was a lesson that France had learned in the 1980s. Faced with the financial pressures exercised by Germany, France had actively promoted the market for its own debt by offering American-style repo facilities. 27 The easier it was to trade French debt for instant liquidity, the more actively it would be purchased and the more accepting the market would be of France’s borrowing requirements. Over the resistance of the Bundesbank, repo was adopted as a core operational model by the ECB. Unlike the more traditional central banks, like the Bank of England or the Fed, the ECB did not hold large quantities of government debt. It managed Europe’s financial system by repoing a wide range of bonds including both private debt and public bonds. 28 Rather than the ECB, it was Europe’s banks that bought their governments’ debt. But they did so with the understanding that if they needed cash in a hurry, the bonds could be exchanged with the ECB on a repurchase basis. The terms of the repo and the size of the ECB haircut were the basic regulating variables in the unified financial system of the eurozone. In this respect, market logic was internal to the operation of the ECB to a degree that was not the case at either the Fed or the Bank of England.

If it had wished to maximize pressure on Europe’s government to preserve fiscal discipline, the ECB could have adopted a discriminatory system of nationally specific repo haircuts, imposing tougher conditions on less credible peripheral eurozone borrowers. Haircuts in the bilateral repo market in the United States varied widely across different types of bonds. A higher haircut would require banks to hold more capital against their bond holdings and shrink their portfolios of that debt. In Europe in the late 1990s, Greece had had to offer far higher interest rates to attract lenders than had Germany. But instead of discriminating, the ECB took the view that a single currency implied a single rate. It would repo the bonds of all European sovereigns on the same terms. 29 Unsurprisingly, this produced a dramatic convergence of yields as investors bid up the price of higher-yielding debts from countries like Greece, Italy, Portugal and Spain, which in the eyes of the ECB were now equivalent to Bunds, Germany’s rock-solid government bonds. The result was a self-reflexive loop in which the ECB relied on markets to exercise discipline over public borrowers while the markets came to assume that the ECB’s “one bond” policy implied an implicit European guarantee for even the weakest borrowers.

The result was that Greece and Portugal could borrow on terms that were better than ever before in their history, and one might have expected this to produce a huge surge in new public borrowing. Reading some commentary on the eurozone crisis, one might imagine that this was indeed what happened. 30 But, despite the unprecedentedly low interest rates, there was, in fact, no public debt boom after 2001. Certain countries borrowed more than others. But overall, the Maastricht rules limiting deficits exercised an effective restraint, especially when one considers the inducement to borrow provided by the convergence of yields. Despite the profound ambiguity of the institutional structure, the sense of calm was preserved by the fact that no major public borrower was grossly abusing the situation. Indeed, as economic growth moved into a higher gear, the ratio of public debt to GDP across the eurozone fell by 7 percent. 31

The countries that failed to meet the eurozone’s budget rules were a mixed bag. Portugal had the most rapidly rising public debt ratio and its budgeting was undeniably lax. But when it joined the euro, its debt was at a low level. Unfortunately, Lisbon made the mistake of entering at an uncompetitive exchange rate. The sharp deterioration in the debt-to-GDP ratio that followed was due as much to a deceleration in growth as it was to irresponsible borrowing. 32 Greece was the other reprobate. In the 1990s, to qualify for eurozone membership, Greece, like Italy, had eked out primary surpluses (on the budget excluding debt service). Even with interest costs running at 11.5 percent of GDP, this had held the deficit in check. After the formation of the eurozone, Greek borrowing costs and debt service charges fell by more than half. It could have been the opportunity for a substantial fiscal consolidation. Instead, Athens let its tax revenue decline. The primary surpluses evaporated and the deficit expanded to 5.5 percent, twice the Maastricht limit. This was bearable only because nominal income growth was so rapid. 33 What made Greece’s situation dangerous, however, was not the pace of borrowing after 2001 but the debts built up in the 1980s and 1990s, when modern Greek democracy had been established on the back of a huge surge in government spending and expensive borrowing. 34 In 2000 Greece’s debt already amounted to 104 percent of GDP.

Though the degree of Greece’s problems was not fully appreciated, it was a known problem case and it was small fry. More politically significant in the early 2000s was the violation of the Growth and Stability Pact rules by France and Germany. This definitely eroded the authority of fiscal discipline. But what were the economic consequences? There was ample demand in financial markets for German Bunds and France’s Treasurys, also known as OATs. Interest rates remained low. France maintained a level trade balance. Germany’s government ran up debt, but combined it with consumer and investment spending so repressed that it produced an ever-larger current account surplus. From the point of view of the eurozone’s macroeconomic balance, it would have been better if Germany had broken the fiscal rules more comprehensively.

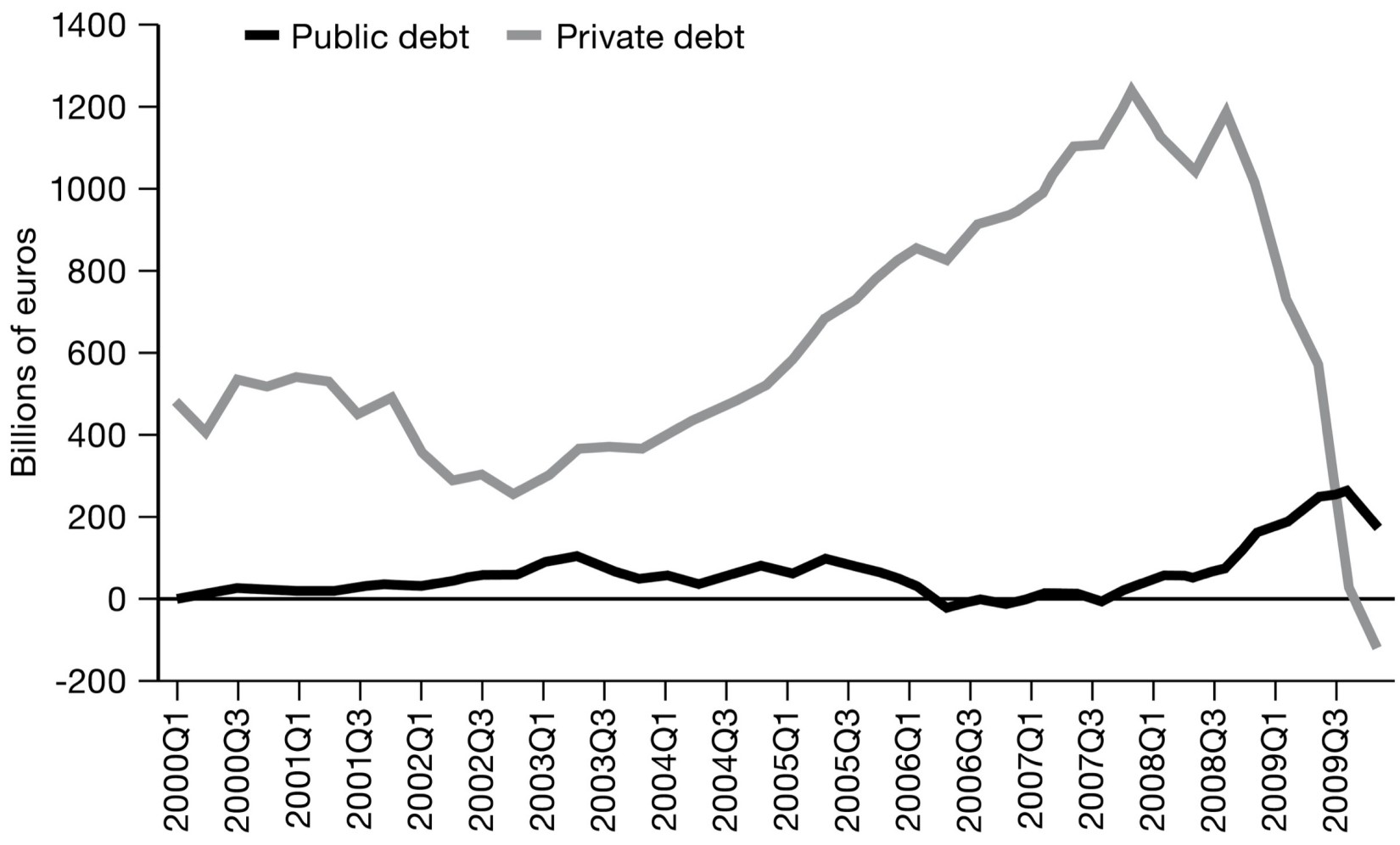

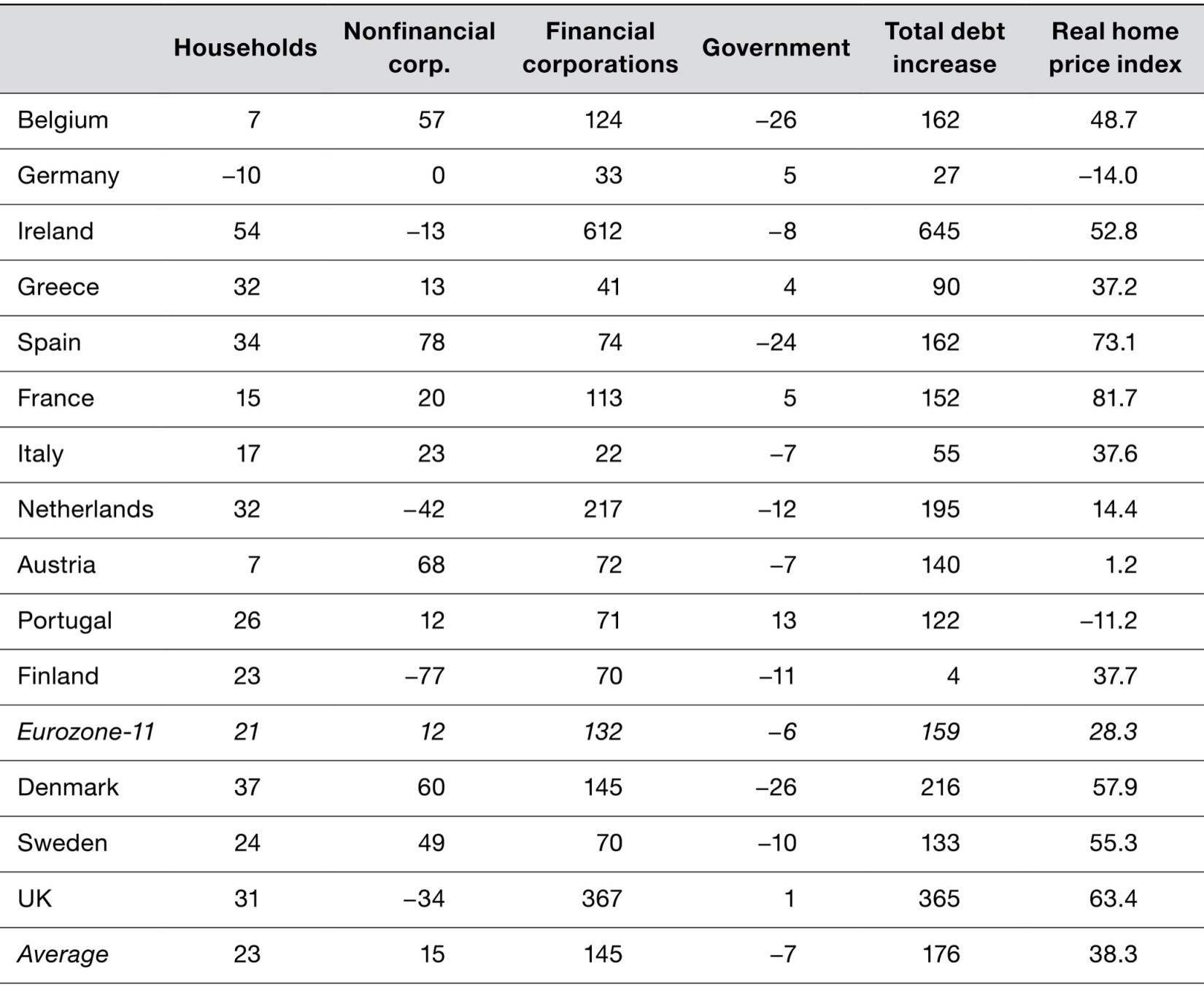

It may fly in the face of conservative assumptions about “democratic deficits” and the spendthrift habits of irresponsible politicians, but the formation of the eurozone without an ironclad fiscal constitution did not lead to a festival of unrestrained sovereign borrowing. The backdrop to the eurozone crisis was, indeed, a gigantic surge in debt, but it was in the private, not the public, sector. The eurozone played host to the same runaway, market-driven process of credit creation that European banks were contributing to so actively in the North Atlantic economy.

Growth in Private and Public Debt in the Eurozone, 2000-2009 (year-on-year)

Source: Richard Baldwin and Daniel Gros, “The Euro in Crisis: What to Do?,” in Completing the Eurozone Rescue: What More Needs to Be Done (2010), 1–24, figure 3, http://voxeu.org/sites/default/files/file/Eurozone_Rescue.pdf .

III

As the Financial Times’s economic commentator Martin Sandbu has remarked, it was the euro’s “great misfortune” to be born “into the greatest private credit bubble of all time.” 35 To which one might add that it was not entirely a matter of bad luck. Giving Europe the scale necessary to cope with the wild fluctuations of global capital unleashed in the early 1970s was always the chief raison d’être of the European Monetary Union. But the global credit expansion of the early 2000s put anything hitherto experienced in the shade, and Europe’s banks were at the leading edge of the boom. French, German, Italian, Benelux, Spanish, Irish and British banks poured credit into profitable hot spots of growth. The eurozone allowed them to do so without regard to borders or currency risk. Cross-border lending within the eurozone exploded, rising even more rapidly than cross-border finance globally. 36 Europe’s bankers used the same array of modern banking techniques in the eurozone that they were putting to such profitable use in London and New York. Securitization had long been a method of mortgage finance in Europe. Notably in Germany, the Pfandbrief model had been a staple since the eighteenth century. But from the early 2000s, American-style securitization took off in Europe as well. In 2007 more than $500 billion in loans were securitized in Europe. In 2008 the total reached $750 billion in European asset-backed security issuance with UK and Spanish banks particularly active. 37

Once again, as in the case of America’s international finances, it is easy to deceive oneself about the direction of these intra-European flows. We have a clear map of the economic hierarchy of Europe in our heads. We know where the loans went—Greece, Spain, Ireland. We know that Germany was the main “surplus” and “creditor” nation. So does that mean that Germany financed the credit boom? Certainly it had the largest trade surplus and was thus the largest net exporter of capital. But as far as overall financial flows within Europe are concerned, that simple mental map is as misleading as the exclusive focus on Sino-American financial relations is on a global scale.

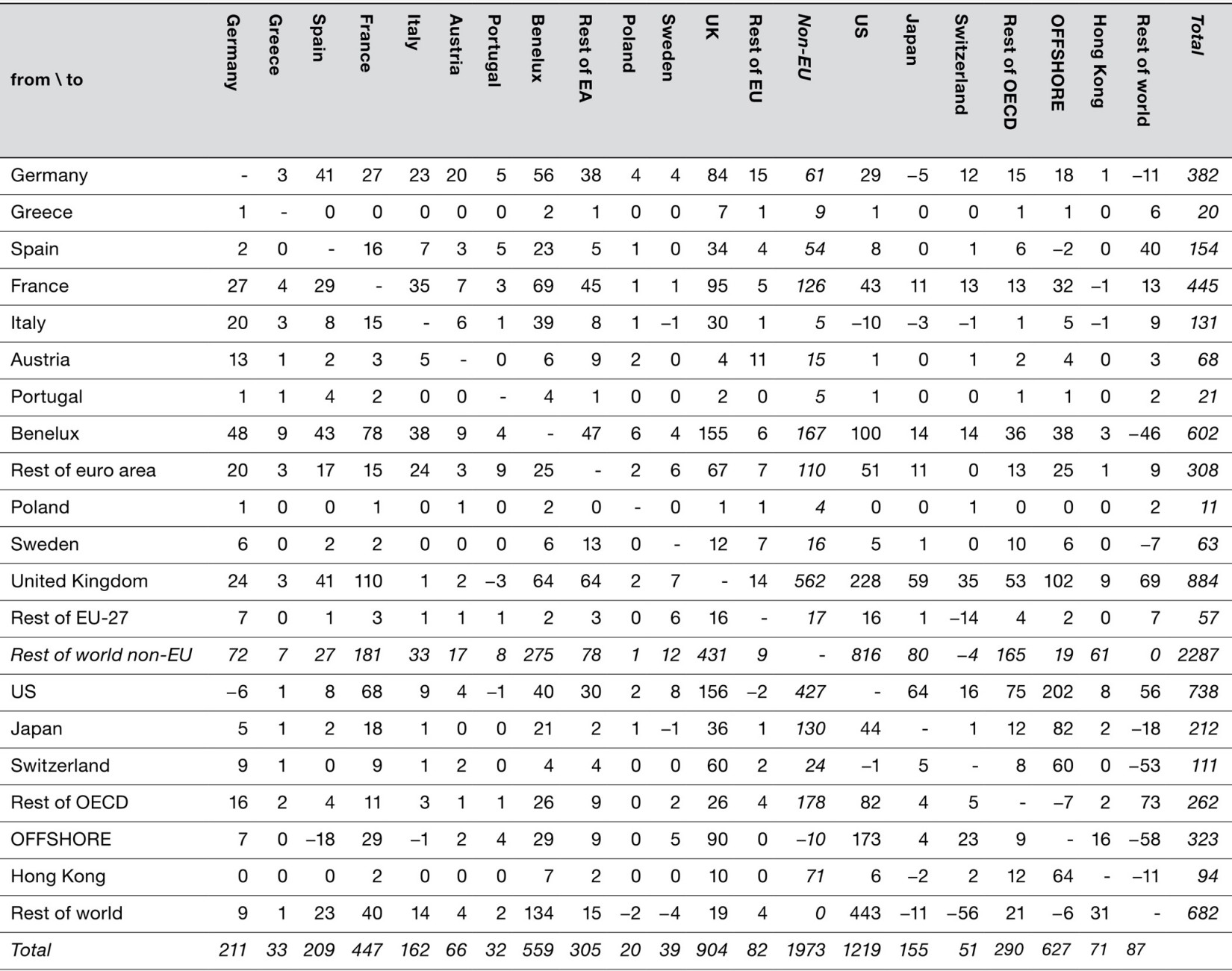

Thanks to the work of economists at the European Commission, we can map the flow of funds within Europe as part of the broader circulation of funds throughout the world economy. In the bottom right-hand quadrant of the following table, we see the outline of the world economy that we have mapped in previous chapters. But if we focus on intra-European flows, it is clear that Germany, despite its export prowess, did not dominate the European financial system. Germany was the largest net lender. Its status was like that of China in relation to the US economy. But financial flows within Europe no more mapped onto trade than they did in the world economy. Germany was a champion exporter of cars and machinery, but in banking and finance others led the field. The UK, France, the Benelux and Ireland (the latter hidden within the category “Rest of Euro area”) were the key hubs for financial flows. The City of London, home to banks from around the world, including all the leading German banks, stands out as the major financial partner for every eurozone member, even though it was not a member of the currency union. France and the Benelux were particularly important because they served as channels through which funds flowed into the eurozone from the outside. American and other lenders from the rest of the world clearly preferred to do business with well-known French, Dutch and Belgian counterparties, who then channeled the funds to the European periphery. France was a major financial hub, not because it had a huge trade surplus but because it had large, ambitious banks that were willing to borrow to lend: 445 billion euros flowed out of France and 447 billion flowed in, leaving a net imbalance of merely 2 billion euros. At the same time, 602 billion euros flowed out of the Benelux banking centers and 559 billion flowed in. The Dutch trade surplus made up the difference.

Cross-Border Financial Flows Within the Eurozone and the World Economy: Annual Averages, 2004–2006 (in billions of euros)

Note: Estimated gross flows (net asset acquisitions) of direct, portfolio and “other” investments (excluding financial derivatives).

Source: A. Hobza and S. Zeugner, “The ‘Imbalanced Balance’ and Its Unravelling: Current Accounts and Bilateral Financial Flows in the Euro Area,” European Commission Economic Papers 520 (2014): table A.2.

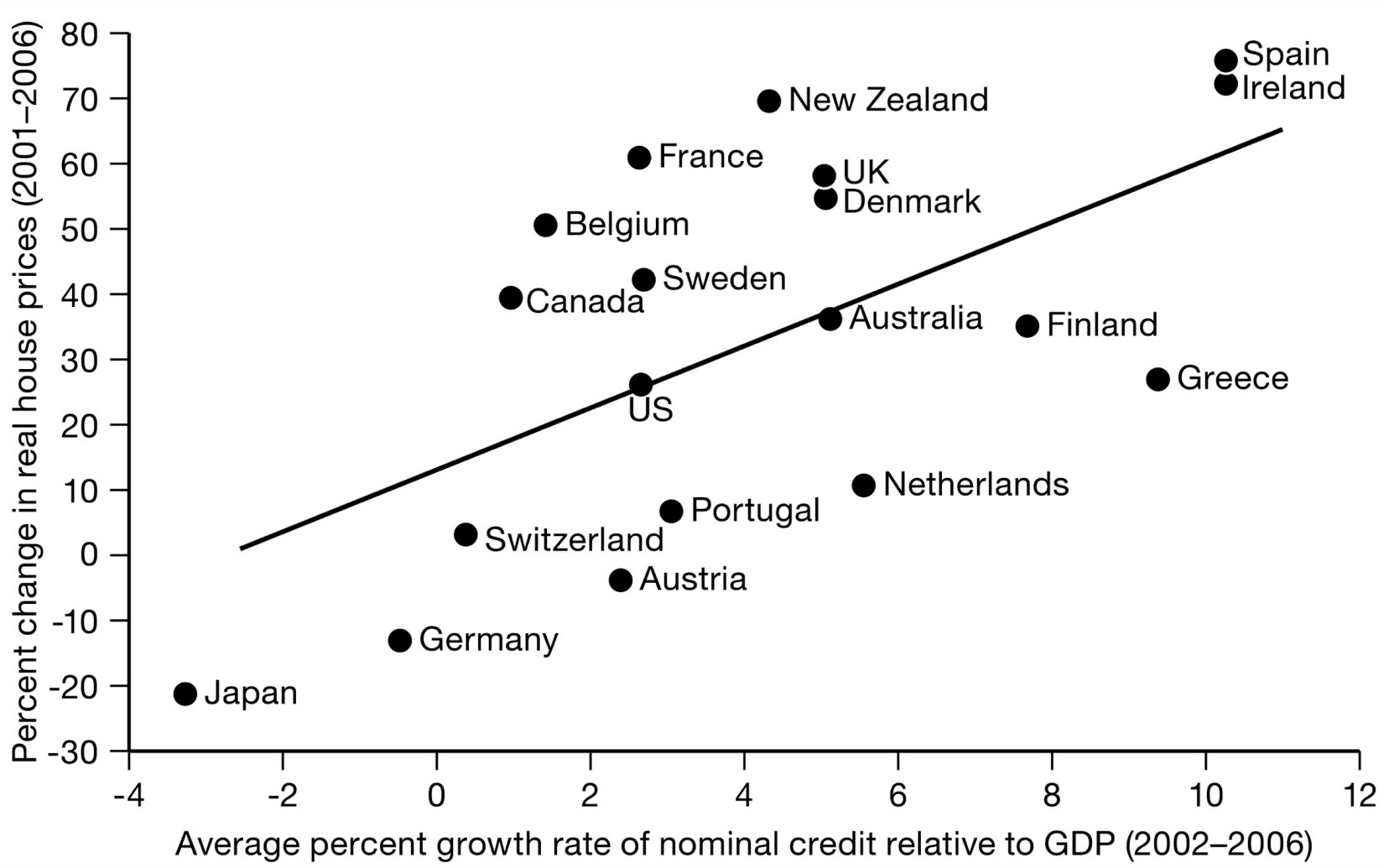

The flow of funds around Europe, as around the global economy, was driven not by trade flows but by the business logic of bankers, who sought out the cheapest funding and the best returns. The upward spiral of asset prices and balance sheets that drove the US boom was even more pronounced in Europe. Between 2001 and 2006, Greece, Finland, Sweden, Belgium, Denmark, the UK, France, Ireland and Spain all experienced real estate booms more severe than those that energized the United States. In Ireland and Spain, the combination of credit growth and house price inflation was truly explosive.

It was these credit-fueled booms that drove the trade and fiscal imbalances of the eurozone, rather than the other way around. The huge influx of credit from all over the world to a hot spot like Spain inflated economic activity there. This generated healthy tax revenues for Madrid, which proudly boasted a fiscal surplus. It also generated export orders for Germany. Foreign demand gave a boost to the languishing German economy, raising incomes and profits. 38 But German households and businesses did not want to spend their income increment in Germany, on either consumption or investment. The German government borrowed, but not enough to soak up the difference. Through interbank markets, surplus liquidity in the north helped to fund business ventures around Europe. Some of that, not surprisingly, went to Spain. At the end of the day the accounts balanced. Germany’s savings appear as the counterpart to Spain’s trade deficit. But accounting identity is not the same as causal relationship. It wasn’t Germany’s excess savings, or its exports, that produced the boom in Spain. It was the lopsided credit-fueled boom that produced the demand imbalances, the trade flows and the savings imbalances. Europe’s banking system provided elastic intermediation. Had Germany’s domestic economy been in more robust shape, Germany’s demand for imports would have been larger, and the trade imbalances within the eurozone might have been smaller. A somewhat larger fraction of the Spanish economy might have been directed toward producing goods for export to Germany rather than supplying the domestic boom. But there is no reason to think that a smaller flow of net savings from a more rapidly growing Germany would have done much to slow the credit-fueled upswing in Ireland or Spain. In modern finance, credit is not a fixed sum constrained by the “fundamentals” of the “real economy.” It is an elastic quantity, which in an asset price boom can easily become self-expanding on a transnational scale.

Real House Prices and Growth Rate of Nominal Credit Relative to GDP

Source: Prakash Kannan, Pau Rabanal and Alasdair M. Scott, “Macroeconomic Patterns and Monetary Policy in the Run-up to Asset Price Busts,” IMF Working Papers (November 2009), figure 2.

Where does Greece, the country that would become the epicenter of the eurozone crisis, fit in this picture? It is present, but vanishingly small. Of the annual flux in cross-border funding within the eurozone between 2004 and 2006, which on average came to c. 1.8 trillion euros, Greece accounted for 33 billion euros. That is less than 2 percent, proportional to Greece’s weight in eurozone GDP. Of that flow of funds, a larger share than was the case in Ireland and Spain went to the Greek state. But Greece too experienced a property boom on a par with the United States. The red flag in Greece was not the annual inflow of capital after 2001 but the fact that the new borrowing was being added to huge stocks of debt already accumulated in prior decades. What would happen if the flow of funds was abruptly cut off was a worrying question, but given Greece’s tiny size, it was hardly headline grabbing.

It would later be said that the ECB should have done more to dampen the boom in Ireland and Spain. And it is clearly true that this was made more difficult by the fact that it set one interest rate for the entire eurozone. In effect, by setting low rates, the ECB prioritized the need to stimulate the German economy over restraining the boom in the periphery. It was a reasonable decision. Germany’s economy is far bigger. Furthermore, given the rates of return that beckoned in the hot spots of the European economy, it is wishful thinking to imagine that the ECB could have curbed the boom with a rate hike. If the EU’s business statistics are to be believed, investment in Spanish tourism and real estate offered rates of return of 30 percent or more. Little wonder that investment crowded in. 39 In a world of globalized finance, the ECB could no more limit the flow of funds to such a hot spot than the Fed could choke off the capital inflow to the United States. Ireland’s banks were a case in point. They sourced their funding wholesale in the City of London, outside the ECB’s immediate purview. 40