Also by Adam Tooze

The Deluge

The Wages of Destruction

Statistics and the German State

VIKING

An imprint of Penguin Random House LLC

375 Hudson Street

New York, New York 10014

Copyright © 2018 by Adam Tooze

Penguin supports copyright. Copyright fuels creativity, encourages diverse voices, promotes free speech, and creates a vibrant culture. Thank you for buying an authorized edition of this book and for complying with copyright laws by not reproducing, scanning, or distributing any part of it in any form without permission. You are supporting writers and allowing Penguin to continue to publish books for every reader.

LIBRARY OF CONGRESS CATALOGING-IN-PUBLICATION DATA

Names: Tooze, J. Adam, author.

Title: Crashed : how a decade of financial crises changed the world / Adam Tooze.

Description: New York : Viking, [2018] | Includes bibliographical references and index.

Identifiers: LCCN 2018025064 (print) | LCCN 2018026794 (ebook) | ISBN 9780525558804 (ebook) | ISBN 9780670024933 (hardcover)

Subjects: LCSH: Global financial crisis, 2008-2009. | Financial crises--Social aspects--History--21st century.

Classification: LCC HB3717 2008 (ebook) | LCC HB3717 2008 .T625 2018 (print) | DDC 332/.042--dc23

LC record available at https://lccn.loc.gov/2018025064

Graph illustrations by Daniel Lagin

While the author has made every effort to provide accurate telephone numbers, internet addresses, and other contact information at the time of publication, neither the publisher nor the author assumes any responsibility for errors or for changes that occur after publication. Further, the publisher does not have any control over and does not assume any responsibility for author or third-party websites or their content.

Version_1

For Dana

Contents

Also by Alan Tooze

Title Page

Copyright

Dedication

Acknowledgments

Introduction: The First Crisis of a Global Age

1. The “Wrong Crisis”

2. Subprime

3. Transatlantic Finance

4. Eurozone

5. Multipolar World

6. “The Worst Financial Crisis in Global History”

7. Bailouts

8. “The Big Thing”: Global Liquidity

9. Europe’s Forgotten Crisis: Eastern Europe

10. The Wind from the East: China

11. G20

12. Stimulus

13. Fixing Finance

14. Greece 2010: Extend and Pretend

15. A Time of Debt

16. G-Zero World

17. Doom Loop

18. Whatever It Takes

19. American Gothic

20. Taper Tantrum

21. “F*** the EU”: The Ukraine Crisis

22. #Thisisacoup

23. The Fear Projects

24. Trump

25. The Shape of Things to Come

Notes

Index

About the Author

Acknowledgments

This book was written with urgency and I am deeply grateful to those who have made it happen. Working with Sarah Chalfant and the Wylie Agency has been as smooth as ever. My editors Simon Winder and Wendy Wolf collaborated enthusiastically on the project. Melanie Tortoroli gave invaluable advice on early drafts. It is their work and that of the production team at Viking and Penguin that have carried this book across the line.

In getting the manuscript into shape I relied heavily on the careful editorial attention of Nick Monaco, Kevin James Schilling and Ella Plaut Taranto.

The project took shape as an undergraduate course taught at Yale and Columbia, where my teaching fellows included Ted Fertik, Gabe Winnant, Nick Mulder, Madeline Woker, David Lerer and Noelle Tutur. I am enormously grateful to all of them.

In addition, from an early stage, the manuscript was read and commented on by Ted Fertik, Grey Anderson, Stefan Eich, Anusar Farooqui, Nick Mulder, Hans Knundani and Nicholas Monaco. Wolfgang Proissel, Barnaby Raine and Dana Conley added their comments to particular chapters. These friends and interlocutors know individually and collectively how much I owe to them.

Pieces I cowrote with Stefan Eich and Danilo Scholz helped to further sharpen the argument.

In connection with the book I benefited enormously from conversations with an array of colleagues, witnesses and participants in the drama described here.

As part of the research I was privileged to interview Mario Monti, Giuliano Amato, Timothy Geithner and Giulio Tremonti. I am extremely grateful for the time they devoted to our conversations.

Through my role as director of the European Institute at Columbia I have been fortunate to try out arguments with Frans Timmermans, Pierre Moscovici, Pierre Vimont, Marco Buti and Moreno Bertoldi.

François Carrel-Billiard is my indispensable collaborator at the institute. It is a privilege to work with him.

Nathan Sheets and Patricia Mosser, veterans of the Fed, gave generously of their time.

Erik Berglof helped me to think through the East European crisis.

A dinner with Mervyn King arranged by Peter Garber proved very illuminating.

Perry Mehrling, Brad Setser, Mike Pyle, Clara Mattei, Martin Sandbu, Nicolas Véron, Cornel Ban, Gabriella Gabor, Shahin Vallée and Eric Monnet all offered invaluable input.

As ever, my old friends David Edgerton and Chris Clark provided an indispensable sounding board.

I have been fortunate to try the arguments of the book at workshops, conferences and seminars hosted in Berlin courtesy of the Hamburg Stiftung für Sozialgeschichte, at the Heidelberg Center for American Studies, the American Academy Berlin, Brown University, Stanford, the Eisenberg Institute University of Michigan, the European University Institute, NYU Florence, the New School, UCLA, the MaxPo conference, the German Historical Institute Paris, the FPLH workshop in London, as part of the Science Po public debt project and at the NYU Kandersteg workshop. I am grateful both to my hosts and other participants at all these events.

A memorial conference for Francesca Carnevali in Birmingham heard a version of the argument about Europe’s banks.

Presenting to a seminar of the Siemens Stiftung moderated by Knut Borchardt and attended by Jürgen Habermas was a particular honor.

Beyond the formal academy I have been extraordinarily fortunate to fall in with a brilliant and deeply informed crowd on Twitter and Facebook who have changed my understanding of how an intense, real-time debate can develop in the twenty-first century.

In the trajectory of my work this project marks a double departure. I have moved forward in time into the field of contemporary history. At the same time I have moved backward to reengage with a youthful preoccupation with economics. This double movement has reminded me of debts I owe to two teachers.

Alan Milward, my doctoral supervisor, was a brilliant but difficult man. Given my personal makeup, the engagement with him was particularly high risk. But I survived and Alan remains a towering figure in the field of modern European history. I don’t know whether he would have agreed with my take on the eurozone crisis, but I feel Alan’s presence.

Wynne Godley was a mentor and teacher of a very different kind. Spontaneously warm and generous in spirit, he took me under his cape in my first year at King’s and introduced me, and a group of my contemporaries, to what, at the time, was a highly idiosyncratic brand of economics. In so doing he provided a model of intellectual warmth and vitality. And he confirmed doubts that had been gestating in me about the IS-LM model that was my first great love in economics. Wynne introduced me to the importance of looking “beyond the flows” and insisting on stock-flow consistency in macro models. I don’t think this book, written almost thirty years later, would have been the same without his early influence.

Writing a book is an emotional, intellectual and physical task. It is work I do at home and there I owe everything to my partner, Dana Conley, whose love and support energized and sustained this project from start to finish. To have such an engaged, deeply intelligent, courageous, vivacious and loving companion, so open to me and to my world, is a blessing beyond words.

Puppy Ruby—a marvelous gift from Dana—added joy, warmth, walks and endless distraction.

My daughter, Edie, has jolted dinner table conversation with a burst of political radicalism and sharp insights. When current events were robbing me of my senses, she offered precocious wisdom. Her energetic but grounded engagement with the world is a source of both inspiration and encouragement.

There is no doubt that these three forces are the keys to my current emotional stability. The fact that this book has not driven us apart but brought us closer together and given us things to talk about is my greatest personal satisfaction.

The fact that I can say all this is due in large part to the wise counsel of an outstanding psychoanalyst. He shall remain nameless. But everyone should be so lucky.

As Nicolas Véron put it to me one evening in Washington Square Park, making sense of what has happened since 2008 is a collective undertaking. As a historian, it has been an extraordinary privilege to be included in that collective. I hope this book in some small way repays the welcome I have received.

New York City

January 2018

Introduction

THE FIRST CRISIS OF A GLOBAL AGE

T uesday, September 16, 2008, was the “day after Lehman.” It was the day global money markets seized up. At the Federal Reserve Board in Washington, DC, September 16 began with urgent plans to sluice hundreds of billions of dollars into the world’s central banks. On Wall Street all eyes were on AIG. Would the global insurance giant make it through the day, or would it follow the investment bank Lehman into oblivion? A shock wave was rippling outward. Within weeks its impact would be felt on factory floors and in dockyards, financial markets and commodity exchanges around the world. Meanwhile, in Midtown Manhattan, September 16, 2008, was the opening day of the sixty-third meeting of the UN General Assembly.

The UN building, on East Forty-second Street, is not where financial power is located in New York. Nor did the speakers at the plenary session that began on the morning of September 23 dwell on the technicalities of the banking crisis. But what they did insist on talking about was its wider meaning. The first head of government to speak was President Lula of Brazil, who energetically denounced the selfishness and speculative chaos that had triggered the crisis. 1 The contrast with President George W. Bush, who followed him to the rostrum, was alarming. Bush seemed not so much a lame duck as a man out of touch with reality, haunted by the failed agenda of his eight-year presidency. 2 The first half of his address spiraled obsessively around the specter of global terrorism. He then took solace in the favorite neoconservative theme of the advance of democracy, which he saw culminating in the “color revolutions” of Ukraine and Georgia. But that was back in 2003/2004. The devastating financial crisis raging just a short walk away on Wall Street merited only two brief paragraphs at the end of the president’s speech. The “turbulence” was, as far as Bush was concerned, an American challenge to be handled by the American government, not a matter for multilateral action.

Others disagreed. Gloria Macapagal Arroyo, president of the Philippines, spoke of America’s financial crisis as having unleashed a “terrible tsunami” of uncertainty. It was spreading around the globe, “not just here in Manhattan Island.” Since the first tremors had shaken the financial markets in 2007, the world had repeatedly reassured itself that the “worst had passed.” But, again and again, “the light at the end of the tunnel” had revealed itself as “an oncoming train hurtling forward with new shocks to the global financial system.” 3 Whatever America’s efforts at stabilization were, they were not working.

One after another, the speakers at the UN connected the crisis to the question of global governance and ultimately to America’s position as the dominant world power. Speaking on behalf of a country that had recently lived through its own devastating financial crisis, Cristina Fernández de Kirchner of Argentina was not one to hide her Schadenfreude. For once, this was a crisis that could not be blamed on the periphery. This was a crisis that “emanated from the first economy of the world.” For decades, Latin America had been lectured that “the market would solve everything.” Now Wall Street was failing and President Bush was promising that the US Treasury would come to the rescue. But was the United States in a fit state to respond? “[T]he present intervention,” Fernández pointed out, was not just “the largest in memory,” it was being “made by a State with an incredible trade and fiscal deficit.” 4 If this was to stand, then the “Washington Consensus” of fiscal and monetary discipline to which so much of the emerging world had been subjected was clearly dead. “It was a historic opportunity to review behaviour and policies.” Nor was it just Latin American resentment on display. The Europeans joined the chorus. “The world is no longer a unipolar world with one super-Power, nor is it a bipolar world with the East and the West. It’s a multipolar world now,” 5 intoned Nicolas Sarkozy, speaking as both president of France and president of the European Council. “The 21st century world” could not be “governed with the institutions of the 20th century.” The Security Council and the G8 would need to be expanded. The world needed a new structure, a G13 or G14. 6

It was not the first time that the question of global governance and America’s role in it had been posed at the United Nations in the new millennium. When the French president spoke at the UN against American unilateralism, no one could ignore the echoes of 2003, Iraq and the struggles over that disastrous war. It was a moment that had bitterly divided Europe and America, governments and citizens. 7 It had revealed an alarming gulf in political culture between the two continents. Bush and his cohorts on the right wing of the Republican Party were not easy for bien-pensant, twenty-first-century citizens of the world to assimilate. 8 For all their talk of the onward march of democracy, it wasn’t even clear that they had won the election that first gave them power in 2000. In cahoots with Tony Blair, they had misled the world over WMD. With their unabashed appeals to divine inspiration and their crusading zeal they flaunted their disregard for the conception of modernity in which both the EU and the UN liked to dress themselves—enlightened, transparent, liberal, cosmopolitan. That was, of course, its own kind of window dressing, its own kind of symbolic politics. But symbols matter. They are essential ingredients in the construction of both meaning and hegemony.

By 2008 the Bush administration had lost that battle. And the financial crisis clinched the impression of disaster. It was a stark historical denouement. In the space of only five years, both the foreign policy and the economic policy elite of the United States, the most powerful state on earth, had suffered humiliating failure. And, as if to compound the process of delegitimatization, in August 2008 American democracy made a mockery of itself too. As the world faced a financial crisis of global proportions, the Republicans chose as John McCain’s vice presidential running mate the patently unqualified governor of Alaska, Sarah Palin, whose childlike perception of international affairs made her the laughingstock of the world. And the worst of it was that a large part of the American electorate didn’t get the joke. They loved Palin. 9 After years of talk about overthrowing Arab dictators, global opinion was beginning to wonder whose regime it was that was changing. As Bush the younger left the stage, the post–cold war order that his father had crafted was crumbling all around him.

Only weeks before the General Assembly opened in New York, the world had been given two demonstrations of the reality of multipolarity. On the one hand, China’s staggering Olympic display put to shame anything ever seen in the West, notably the dismal Atlanta games of 1996, which had been interrupted, it is worth recalling, by a pipe bombing perpetrated by an alt-right fanatic. 10 If bread and circuses are the foundation of popular legitimacy, the Chinese regime, bolstered by its booming economy, was putting on quite the show. Meanwhile, as the fireworks flared in Beijing, the Russia military had meted out to Georgia, a tiny aspirant to NATO membership, a severe punishment beating. 11 Sarkozy came to New York fresh from cease-fire talks on Europe’s eastern border. It was to be the first of a series of more or less open clashes between Russia and the West that would culminate in the violent dismemberment of Ukraine, another aspiring NATO member, and feverish speculation about Russia’s subversion of America’s 2016 presidential election.

The financial crisis of 2008 appeared as one more sign of America’s fading dominance. And that perspective is all too easily confirmed, when we return to the crisis from the distance of a decade, in the wake of the election of Donald Trump, the heir to Palin, as president. It is hard now to read the UN speeches in 2008 and their critique of American unilateralism without Trump’s truculent inaugural of January 20, 2017, ringing in one’s ears. On that overcast Friday, from the steps of the Capitol, the forty-fifth president summoned the image of America in crisis, its cities in disorder, its international standing in decline. This “carnage,” he declared, must end. How? Trump’s answer boomed out: He and his followers, that day, were issuing a “decree, to be heard in every city, in every foreign capital, and in every hall of power. From this day forward, a new vision will govern our land. From this day forward, it’s going to be only America first, America first . . .” 12 If America was indeed suffering a profound crisis, if it was no longer supreme, if it needed to be made “great again,” truths that for Trump were self-evident, then it would at least “decree” its own terms of engagement. This was the answer that the right wing in American politics would give to the challenges of the twenty-first century.

The events of 2003, 2008 and 2017 are all no doubt defining moments of recent international history. But what is the relationship among them? What is the relationship of the economic crisis of 2008 to the geopolitical disaster of 2003 and to America’s political crisis following the election of November 2016? What arc of historical transition do those three points stake out? What does that arc mean for Europe, for Asia? How does it relate to the minor but no less shattering trajectory traced by the United Kingdom from Iraq to the crisis of the City of London in 2008 and Brexit in 2016?

The contention of this book is that the speakers at the UN in September 2008 were right. The financial crisis and the economic, political and geopolitical responses to that crisis are essential to understanding the changing face of the world today. But to understand their significance we have to do two things. We have to place the banking crisis in its wider political and geopolitical context. And, at the same time, we have to get inside its inner workings. We have to do what the UN General Assembly in September 2008 could not do. We have to grapple with the economics of the financial system. This is a necessarily technical and at times perhaps somewhat coldhearted business. There is a chilly remoteness to much of the material that this book will be dealing with. This is a choice. Tracing the inner workings of the Davos mind-set is not the only way to understand how power and money operated in the course of the crisis. One can try to reconstruct their logic from the boot prints they left on those they impacted or through the conformist and contradictory market-oriented culture that they molded. 13 But the necessary complement to those more tactile renderings is the kind of account offered here, which attempts to show how the circulation of power and money was understood to function—and not to function—from within. And this particular black box is worth prizing open, because, as this book will show, the simple idea, the idea that was so prevalent in 2008, the idea that this was basically an American crisis, or even an Anglo-Saxon crisis, and as such a key moment in the demise of American unipolar power, is in fact deeply misleading.

Eagerly taken up by all sides—by Americans as well as commentators around the world—the idea of an “all-American crisis” obscures the reality of profound interconnection. 14 In so doing, it also misdirects criticism and righteous anger. In fact, the crisis was not merely American but global and, above all, North Atlantic in its genesis. And in a contentious and problematic way it had the effect of recentering the world financial economy on the United States as the only state capable of meeting the challenge it posed. 15 That capacity is an effect of structure—the United States is the only state that can generate dollars. But it is also a matter of action, of policy choices—positive in the American case, disastrously negative in the case of Europe. Clarifying the scale of this interdependence and the ultimate dependence of the global financial system on the dollar is important not just for the sake of getting the history right. It matters also because it throws new light on the perilous situation created by the Trump administration’s declaration of independence from an interconnected and multipolar world.

I

To view the crisis of 2008 as basically an American event was tempting because that is where it had begun. It also pleased people around the world to imagine that the hyperpower was getting its comeuppance. The fact that the City of London was imploding too added to the deliciousness of the moment. It was convenient for the Europeans to shift responsibility across the channel and then across the Atlantic. In fact, it was a script prepared ahead of time. As we will see in the first section of this book, economists inside and outside America critical of the Bush presidency, including many of the leading macroeconomists of our time, had prepared a disaster script. It revolved around America’s twin deficits—its budget deficit and its trade deficit—and their implications for America’s dependence on foreign borrowing. The debts run up by the Bush administration were the bomb that was expected to go off. And the idea of 2008 as a distinctively Anglo-American crisis received a backhanded confirmation eighteen months later when Europe experienced its own crisis, which appeared to follow a rather different script, centered on the politics and the constitution of the eurozone. Thus the historical narrative seemed to neatly arrange itself with a European crisis following an American crisis, each with its own distinct economic and political logic.

The contention of this book is that to view the 2008 crisis and its aftermath chiefly through its impact on America is to fundamentally misunderstand and underestimate its economic and historical significance. Ground zero was America’s housing market, for sure. Millions of American households were among those hit earliest and hardest. But that disaster was not the crisis that had been widely anticipated before 2008, namely, a crisis of the American state and its public finances. The risk of the Chinese-American meltdown, which so many feared, was contained. Instead, it was a financial crisis triggered by the humdrum market for American real estate that threatened the world economy. The crisis spilled far beyond America. It shook the financial systems of some of the most advanced economies in the world—the City of London, East Asia, Eastern Europe and Russia. And it went on doing so. Contrary to the narrative popular on both sides of the Atlantic, the eurozone crisis is not a separate and distinct event, but follows directly from the shock of 2008. The redescription of the crisis as one internal to the eurozone and centered on the politics of public debt was itself an act of politics. In the years after 2010, it would become the object of something akin to a transatlantic culture war in economic policy, a minefield that any history of the epoch must carefully navigate.

If mapping this misunderstanding, charting the global financial crisis outward from its hub in the North Atlantic and presenting the continuity between 2008 and 2012, is the first challenge of this book, the second is to account for the way in which states did and did not react to the turmoil. The impact of the crisis was uneven but global in its reach, and by the vigor of their reactions, emerging market governments spectacularly confirmed the reality of multipolarity. The emerging market crises of the 1990s—Mexico (1995); Korea, Thailand, Indonesia (1997); Russia (1998); and Argentina (2001)—had taught how easily state sovereignty could be lost. That lesson had been learned. After a decade of determined “self-strengthening” in 2008, none of the victims of the 1990s were forced to resort to the International Monetary Fund. China’s response to the financial crisis it imported from the West was of world historic proportions, dramatically accelerating the shift in the global balance of economic activity toward East Asia.

One might be tempted to conclude that the crisis of globalization had brought a reaffirmation of the essential role of the nation-state and the emergence of a new kind of state capitalism. And that is an argument that would gain ever greater force in the years that followed, as the political backlash set in. 16 But if we look closely not at the periphery but at the core of the 2008 crisis, it is clear that this diagnosis is partial at best. Among the emerging markets, the two that struggled most with the crisis of 2008 were Russia and South Korea. What they had in common apart from booming exports was deep financial integration with Europe and the United States. That would prove to be the key. What they experienced was not just a collapse in exports but a “sudden stop” in the funding of their banking sectors. 17 As a result, countries with trade surpluses and huge currency reserves—supposedly the essentials of national economic self-reliance—suffered acute currency crises. Writ spectacularly larger, this was also the story in the North Atlantic between Europe and the United States. Hidden below the radar and barely discussed in public, what threatened the stability of the North Atlantic economy in the fall of 2008 was a huge shortfall in dollar funding for Europe’s oversized banks. And a shortfall in their case meant not tens of billions, or even hundreds of billions, but trillions of dollars. It was the opposite of the crisis that had been forecast. Not a dollar glut but an acute dollar-funding shortage. The dollar did not plunge, it rose.

If we are to grasp the dynamics of this unforecasted storm, we have to move beyond the familiar cognitive frame of macroeconomics that we inherited from the early twentieth century. Forged in the wake of World War I and World War II, the macroeconomic perspective on international economics is organized around nation-states, national productive systems and the trade imbalances they generate. 18 It is a view of the economy that will forever be identified with John Maynard Keynes. Predictably, the onset of the crisis in 2008 evoked memories of the 1930s and triggered calls for a return to “the master.” 19 And Keynesian economics is, indeed, indispensable for grasping the dynamics of collapsing consumption and investment, the surge in unemployment and the options for monetary and fiscal policy after 2009. 20 But when it comes to analyzing the onset of financial crises in an age of deep globalization, the standard macroeconomic approach has its limits. In discussions of international trade it is now commonly accepted that it is no longer national economies that matter. What drives global trade are not the relationships between national economies but multinational corporations coordinating far-flung “value chains.” 21 The same is true for the global business of money. To understand the tensions within the global financial system that exploded in 2008 we have to move beyond Keynesian macroeconomics and its familiar apparatus of national economic statistics. As Hyun Song Shin, chief economist at the Bank for International Settlements and one of the foremost thinkers of the new breed of “macrofinance,” has put it, we need to analyze the global economy not in terms of an “island model” of international economic interaction—national economy to national economy—but through the “interlocking matrix” of corporate balance sheets—bank to bank. 22 As both the global financial crisis of 2007–2009 and the crisis in the eurozone after 2010 would demonstrate, government deficits and current account imbalances are poor predictors of the force and speed with which modern financial crises can strike. 23 This can be grasped only if we focus on the shocking adjustments that can take place within this interlocking matrix of financial accounts. For all the pressure that classic “macroeconomic imbalances”—in budgets and trade—can exert, a modern global bank run moves far more money far more abruptly. 24

What the Europeans, the Americans, the Russians and the South Koreans were experiencing in 2008 and the Europeans would experience again after 2010 was an implosion in interbank credit. As long as your financial sector was modestly proportioned, big national currency reserves could see you through. That is what saved Russia. But South Korea struggled, and in Europe, not only were there no reserves but the scale of the banks and their dollar-denominated business made any attempt at autarkic self-stabilization unthinkable. None of the leading central banks had gauged the risk ahead of time. They did not foresee how globalized finance might be interconnected with the American mortgage boom. The Fed and the Treasury misjudged the scale of the fallout from the bankruptcy of Lehman on September 15. Never before, not even in the 1930s, had such a large and interconnected system come so close to total implosion. But once the scale of the risk became evident, the US authorities scrambled. As we shall see in Part II, not only did the Europeans and Americans bail out their ailing banks at a national level. The US Federal Reserve engaged in a truly spectacular innovation. It established itself as liquidity provider of last resort to the global banking system. It provided dollars to all comers in New York, whether banks were American or not. Through so-called liquidity swap lines, the Fed licensed a hand-picked group of core central banks to issue dollar credits on demand. In a huge burst of transatlantic activity, with the European Central Bank (ECB) in the lead, they pumped trillions of dollars into the European banking system.

This response was surprising not only because of its scale but also because it contradicted the conventional narrative of economic history since the 1970s. The decades prior to the crisis had been dominated by the idea of a “market revolution” and the rollback of state interventionism. 25 Government and regulation continued, of course, but they were delegated to “independent” agencies, emblematically the “independent central banks,” whose job was to ensure discipline, regularity and predictability. Politics and discretionary action were the enemies of good governance. The balance of power was hardwired into the normality of the new regime of deflationary globalization, what Ben Bernanke euphemistically referred to as the “great moderation.” 26 The question that hung over the dispensation of “neoliberalism” was whether the same rules applied to everyone or whether the truth was that there were rules for some and discretion for others. 27 The events of 2008 massively confirmed the suspicion raised by America’s selective interventions in the emerging market crises of the 1990s and following the dot-com crisis of the early 2000s. In fact, neoliberalism’s regime of restraint and discipline operated under a proviso. In the event of a major financial crisis that threatened “systemic” interests, it turned out that we lived in an age not of limited but of big government, of massive executive action, of interventionism that had more in common with military operations or emergency medicine than with law-bound governance. And this revealed an essential but disconcerting truth, the repression of which had shaped the entire development of economic policy since the 1970s. The foundations of the modern monetary system are irreducibly political.

No doubt all commodities have politics. But money and credit and the structure of finance piled on them are constituted by political power, social convention and law in a way that sneakers, smartphones and barrels of oil are not. At the apex of the modern monetary pyramid is fiat money. 28 Called into existence and sanctioned by states, it has no “backing” other than its status as legal tender. That uncanny fact became literally true for the first time in 1971–1973 with the collapse of the Bretton Woods system. Under the Bretton Woods agreement of 1944, the dollar, as the anchor of the global monetary system, was tied to gold. This was itself, of course, no more than a convention. When it became too hard for the United States to live with—upholding it would have required deflation—on August 15, 1971, President Nixon abandoned it. This was a historic caesura. For the first time since the advent of money, no currency in the world any longer operated on a metallic standard. Potentially, this freed monetary policy, regulating the creation of money and credit as never before. But how much freedom would policy makers actually have after throwing off the “golden fetters”? The social and economic forces that had made the gold peg unsustainable even for the United States were powerful—at home the struggle for income shares in an increasingly affluent society, abroad the liberalization of offshore dollar trading in London in the 1960s. When those forces were unleashed in the 1970s without a monetary anchor, the result was to send inflation soaring toward 20 percent in the advanced economies, something unprecedented in peacetime. But rather than retreating from liberalization, by the early 1980s any restriction on global capital flows was lifted. It was precisely to tame the forces of indiscipline unleashed by the end of metallic money that the market revolution and the new neoliberal “logic of discipline” were inaugurated. 29 By the mid-1980s Fed chair Paul Volcker’s dramatic campaign to raise interest rates had curbed inflation. The only prices going up in the age of the great moderation were those for shares and real estate. When that bubble burst in 2008, when the world faced not inflation but deflation, the key central banks threw off their self-imposed shackles. They would do whatever it took to prevent a collapse of credit. They would do whatever it took to keep the financial system afloat. And because the modern banking system is both global and based on dollars, that meant unprecedented transnational action by the American state.

The Fed’s liquidity provision was spectacular. It was of historic and lasting significance. Among technical experts it is commonly agreed that the swap lines with which the Fed pumped dollars into the world economy were perhaps the decisive innovation of the crisis. 30 But in public discourse these actions have remained far below the radar. They have been displaced from discussion by controversies surrounding the bailouts of individual banks and subsequent waves of central bank intervention that went by the name of quantitative easing. Even in the memoirs of Ben Bernanke, for instance, the transatlantic liquidity measures of 2008 receive little more than a passing mention by comparison with the fraught politics of the AIG takeover or mortgage credit relief. 31

The technical and administrative complexities of the Fed’s actions no doubt contribute to their obscurity. But the politics go beyond that. The bank bailouts of 2008 provoked long-running and bitter recrimination and for good reason. Hundreds of billions of taxpayer funds were put in play to rescue greedy banks. Some interventions yielded a return. Others did not. Many of the choices made in the course of the bailouts were highly contentious. In the United States they would exacerbate deep rifts within the Republican Party, with dramatic consequences eight years later. But the problem goes beyond individual decisions and party political programs to the way in which we think and talk about the structure of the modern economy. Indeed, it goes directly back to the analytical agenda of reimagining international economics, forced on us by the crisis and articulated by the proponents of the macrofinancial approach. In the familiar twentieth-century island model of international economic interaction, the basic units were national economies that traded with one another, ran trade surpluses and deficits and accumulated national claims and liabilities. Those entities were made familiar by economists, who gave them an empirical, everyday reality in statistics for unemployment, inflation and GDP. And around them an entire conception of national politics developed. 32 Good economic policy was what was good for GDP growth. Questions of distribution—the politics of “who whom?”—could be weighed up against the general interest in “growing the size of the cake.” By contrast, the new macrofinancial economics, with its relentless focus on the “interlocking matrix” of corporate balance sheets, strips away all the comforting euphemisms. National economic aggregates are replaced by a focus on corporate balance sheets, where the real action in the financial system is. This is hugely illuminating. It gives economic policy a far greater grip. But it exposes something that is deeply indigestible in political terms. The financial system does not, in fact, consist of “national monetary flows.” Nor is it made up of a mass of tiny, anonymous, microscopic firms—the ideal of “perfect competition” and the economic analogue to the individual citizen. The overwhelming majority of private credit creation is done by a tight-knit corporate oligarchy—the key cells in Shin’s interlocking matrix. At a global level twenty to thirty banks matter. Allowing for nationally significant banks, the number worldwide is perhaps a hundred big financial firms. Techniques for identifying and monitoring the so-called systemically important financial institutions (SIFI)—known as macroprudential supervision—are among the major governmental innovations of the crisis and its aftermath. Those banks and the people who run them are also among the key actors in the drama of this book.

The stark truth about Ben Bernanke’s “historic” policy of global liquidity support was that it involved handing trillions of dollars in loans to that coterie of banks, their shareholders and their outrageously remunerated senior staff. Indeed, as we shall see, we can itemize precisely who got what. To compound the embarrassment, though the Fed is a national central bank, at least half the liquidity support it provided went to banks not headquartered in the United States, but located overwhelmingly in Europe. If in intellectual terms the crisis was a crisis of macroeconomics, if in practical terms it was a crisis of the conventional tools of monetary policy, it was by the same token a deep crisis of modern politics. However unprecedented and effective the Fed’s actions might have been, even for those politicians whose support for globalization was unfailing, its practical implications were barely speakable. Though it is hardly a secret that we inhabit a world dominated by business oligopolies, during the crisis and its aftermath this reality and its implications for the priorities of government stood nakedly exposed. It is an unpalatable and explosive truth that democratic politics on both sides of the Atlantic has choked on.

II

It should not be surprising, given what has been said, that the Europeans were only too happy to forget the entanglement of their global banks in the transatlantic crisis. In 2008 the British had their own national catastrophe to digest. In the eurozone, led by France and Germany, the 2008 financial crisis has vanished down a memory hole, closed over by the “sovereign debt crisis” of 2010 and after. 33 There is no appetite for acknowledging the dependence on the US Federal Reserve and little sense of obligation or deference either. In this respect too the Americans have lost their authority. The Europeans all too easily dismissed the American crisis fighting of 2008–2009 as yet another instance of the kind of improvisation and indiscipline that had got the world into trouble in the first place. It became the first stage in a transatlantic culture war over economic policy that culminated in the acrimonious debate about the crisis of the eurozone, which takes center stage in Part III of this book.

Given that they were essentially interrelated crises and that the first was much larger in scale and dramatic in speed, the contrast between the relatively effective containment of the global meltdown in 2008, described in Part II, and the spiraling disaster of the eurozone, narrated in Part III, is painful. Around Greek debt the Europeans constructed their own crisis with its own narrative. It had the politics of sovereign debt at its heart. But, as senior economic officials of the EU will now publicly admit, this had no basis in economics. 34 The sustainability of public debts may be a problem in the long term. Greece was insolvent. But excessive public debt was not the common denominator of the wider eurozone crisis. The common denominator was the dangerous fragility of an overleveraged financial system, excessively reliant on short-term market-based funding. The eurozone crisis was a massive aftershock of the earthquake in the North Atlantic financial system of 2008, working its way out with a time lag through the labyrinthine political framework of the EU. 35 As one leading EU expert closely associated with the EU’s bailout programs has put it: “If we had taken the banks under central supervision then already [in 2008], we would have solved the problem at a stroke.” 36 Instead the eurozone crisis expanded into a doom loop of private and public credit and a crisis of the European project as such.

How do we account for the strange morphing of a crisis of lenders in 2008 into a crisis of borrowers after 2010? It is hard not to suspect sleight of hand. While Europe’s taxpayers were put through the mill, the banks and other lenders got paid out of money pumped into the bailout countries. It is a short step from there to concluding that the hidden logic of the eurozone crisis after 2010 was a repetition of the 2008 bank bailouts, but this time in disguise. For one sharp-tongued critic it was the greatest “bait and switch” in history. 37 But the puzzle is that if this were so, if what was happening in the eurozone was a veiled rerun of 2008, then at least one might have expected to have seen American-style outcomes. As its protagonists were well aware, America’s crisis fighting exhibited massive inequity. 38 People on welfare scraped by while bankers carried on their well-upholstered lives. But though the distribution of costs and benefits was outrageous, at least America’s crisis management worked. Since 2009 the US economy has grown continuously and, at least by the standards set by official statistics, it is now approaching full employment. By contrast, the eurozone, through willful policy choices, drove tens of millions of its citizens into the depths of a 1930s-style depression. It was one of the worst self-inflicted economic disasters on record. That tiny Greece, with an economy that amounts to 1–1.5 percent of EU GDP, should have been made the pivot for this disaster twists European history into the image of bitter caricature.

It is a spectacle that ought to inspire outrage. Millions have suffered for no good reason. But for all our indignation we should give that point its full weight. The crucial words are “for no good reason.” 39 In the response to the financial crisis of 2008–2009 there was a clear logic operating. It was a class logic, admittedly—“Protect Wall Street first, worry about Main Street later”—but at least it had a rationale and one operating on a grand scale. To impute that same logic to the management of the eurozone is to give Europe’s leaders too much credit. The story told here is not that of a successful political conjuring trick, in which EU elites neatly veiled their efforts to protect the interests of European big business. The story told here is of a train wreck, a shambles of conflicting visions, a dispiriting drama of missed opportunities, of failures of leadership and failures of collective action. If there are groups that benefited—a few bondholders who got paid, a bank that escaped painful restructuring—it was on a small scale, totally out of proportion to the enormous costs inflicted. This is not to say that the individual actors in the drama—Germany, France, the IMF—lacked logic. But they had to act together and the collective result was a disaster. They inflicted social and political harm from which the project of the EU may never recover. But amid the outrage this shambles should inspire, we are apt to forget another of its long-term consequences. The botched management of the eurozone crisis coming on the heels of the transatlantic financial crisis of 2008–2009 was damaging not only for millions of Europe’s citizens. It had dramatic consequences for European business too, on whom willy-nilly those same people rely for jobs and wages.

Far from being beneficiaries of EU crisis management, business was one of its casualties, and the European banks above all. Since 2008, it is not just the rise of Asia that is shifting the global corporate hierarchy. It is the decline of Europe. 40 This might ring oddly to Europeans used to hearing boasts of Germany’s trade surplus. But as Germany’s own most perceptive economists point out, those surpluses are as much the result of repressed imports as of roaring export success. 41 The inexorable slide of corporate Europe down the global rankings is clear for all to see. Though we might wish otherwise, the world economy is not run by medium-sized “Mittelstand” entrepreneurs but by a few thousand massive corporations, with interlocking shareholdings controlled by a tiny group of asset managers. In that battlefield of corporate competition, the crises of 2008–2013 brought European capital a historic defeat. No doubt there are many factors contributing to this, but a crucial one is the condition of Europe’s own economy. Exports matter, but, as both China and the United States demonstrate, there is no substitute for a profitable home market. If we take the cynical view that the basic mission of the eurozone was not to serve its citizens but to provide European capital with a field for profitable domestic accumulation, then the conclusion is inescapable: Between 2010 and 2013 it failed spectacularly. And not first and foremost as a result of missing eurozone institutions, but as a result of choices made by business leaders, dogmatic central bankers and conservatively minded politicians.

Of course, we may not welcome a world organized this way. Europeans may warm to the spectacle of the European Commission as a consumer champion taking on global monopolists like Google and challenging Apple’s tax evasion. 42 But the fines levied on Silicon Valley are a tiny portion of those firms’ cash hoards. A rather different vision of the balance of power is suggested by those moments in 2016 when the financial world waited with bated breath to learn the size of the settlement that the US Department of Justice was going to impose on Deutsche Bank for mortgage fraud. Deutsche’s financial condition was understood to be so fragile that the US authorities held its fate in their hands. 43 A bank that for more than a century had been a powerhouse of Germany Inc. was at the mercy of the United States. In the wake of the crisis it was the last European investment bank with any global standing.

Europeans may wish to opt out of the global battle for corporate domination. They may even hope that they may thus achieve a greater degree of freedom for democratic politics. But the risk is that their growing reliance on other people’s technology, the relative stagnation of the eurozone and the consequent dependence of Europe’s growth model on exports to other people’s markets will render those pretensions to autonomy quite empty. Rather than an autonomous actor, Europe risks becoming the object of other people’s capitalist corporatism. Indeed, as far as international finance is concerned, the die has already been cast. In the wake of the double crisis, Europe is out of the race. The future will be decided between the survivors of the crisis in the United States and the newcomers of Asia. 44 They may choose to locate in the City of London, but after Brexit even that cannot be taken for granted. Wall Street, Hong Kong and Shanghai may simply bypass Europe.

If this were simply a drama of Europe’s self-inflicted wounds, it would be bad enough. But to write the history of the eurozone crisis as simply European would be barely less misleading than writing the history of 2008 as all-American. In fact, the eurozone crisis spilled over, repeatedly. At least three times—in the spring of 2010, in the fall of 2011 and then again in the summer of 2012—the eurozone was on the brink of a disorderly breakup with the distinct possibility of the sovereign debt crisis sucking in trillions of dollars of public debt. The idea that Germany or any other country would have been immune was fatuous. The resulting inversion of the fronts was spectacular. In 2008 it had been the worldly Europeans calling on the out-of-touch Bush administration to recognize the reality of globalism. Eighteen months later it was the centrist liberals of the Obama administration pleading for the eurozone to stabilize its financial system in the face of dogged and unheeding resistance from conservatives in Berlin and Frankfurt. Already in April 2010, in the judgment of the rest of the G20 and far beyond, the eurozone crisis was too dangerous and the Europeans too incompetent for them to be left to sort out their own affairs. To prevent Greece from becoming “another Lehman,” the Americans mobilized the IMF, that quintessential creation of mid-twentieth-century globalism, to rescue twenty-first-century Europe. That rescue in May 2010 stopped a further escalation, but it locked Europe, the IMF and the United States as an accessory into a nightmarish entanglement from which they still had not extricated themselves seven years later. Nor did it staunch the panic in bond markets. As late as the summer of 2012 the prospect of a major European sovereign debt crisis threatened the United States and the rest of the world economy. It was not until July 2012, with insistent urging from Washington and the rest of G20, that Europe stabilized, and it did so by means of what was generally taken to be the belated “Americanization” of the ECB. 45

III

If one stopped the clock in the fall of 2012, the difference to the scene four years earlier in New York would have been remarkable. Despite the unpromising start, it would have been churlish to deny that American corporate liberalism, as embodied by the Obama administration, had prevailed once again. Indeed, even today, our sense that the financial crisis had an ending, that at some point in the not too distant past something like normality was restored, depends on looking back to the fall of 2012. At that point the acute threat of a comprehensive crisis was ended. And a sign of that restored normality was the fact that America had not been dethroned. Obama’s reelection in November 2012 clinched it. The Palin tendency had been stopped in its tracks. Internationally, the emerging markets were booming, helped along by the Fed’s generous supply of dollars. The EU was playing catch-up. Whereas in 2008 Obama had put distance between himself and the Bush-Cheney years by adopting a tone of modesty and caution, in 2012 he resumed a classic exceptionalist narrative. America was “indispensable.” The phrase coined in the Clinton era had a new lease on life. 46 There was a revival in big-picture foreign policy thinking. The new frontier was the “trade” treaties of TTIP and TPP, in reality gigantic projects of commercial, financial, technical and legal integration with geopolitical intent. Insofar as the first Obama term had been disappointing, this could be laid at the door of conservative opposition. That was depressing but predictable. Modernity and the global capitalism that gave it so much of its dynamic are demanding pacesetters; foot-dragging from conservatives is only to be expected. But in the end history moves on. Even in Europe, pragmatic managerialism in the end prevailed over conservative dogma.

If we are to understand the last ten years historically, we have to take this moment of renewed complacency seriously. Given subsequent events, our retrospective view is easily clouded by a combination of rage, indignation and fear. But at the time the sense of self-confidence restored was real enough and it left an intellectual legacy. It was the moment when the first surveys of the crisis began to be written. The most optimistic insisted that The System Worked . 47 Another declared that 2008 had turned out to be The Status Quo Crisis . 48 The more pessimistic version argued that we lived in a Hall of Mirrors . 49 Precisely because the crisis had been contained so early and effectively, it had produced a false sense of stability. That in turn had sapped the energy necessary for fundamental reform. And this meant that there was an acute risk of repetition. But repetition is not the same as continuation or extension. What all of these narratives took for granted—both the more and the less pessimistic versions—was the fact that the 2008–2012 crisis was over. That was also the basis on which this book was begun. It was intended to be an anniversary retrospect on a crisis that had reached closure. The tasks that seemed urgent in 2013 were to explain the interconnected history of Wall Street and the eurozone crisis, to do justice to the transnational quality of the crisis—its effects across Eastern and Western Europe and Asia—to highlight the indispensable role of the United States in anchoring the response to the crisis and the novel tools that the Fed had deployed, to chart the painful and protracted inadequacy of the European response and to cast light on an intense but underappreciated period of transatlantic financial diplomacy. All of that is still worth doing. But it has now taken on a new and more ominous meaning. Because it is only if we get to grips with the inner workings of the dollar-based financial system and its fragility that we can understand the risks that lurk in the situation of 2017. If Trump’s presidency marks the nadir of American political authority, that is all the more troubling given the deep functional dependence on the United States revealed not only by 2008 but by the eurozone crisis as well.

What we have to reckon with now is that, contrary to the basic assumption of 2012–2013, the crisis was not in fact over. What we face is not repetition but mutation and metastasis. As Part IV of this book will chart, the financial and economic crisis of 2007–2012 morphed between 2013 and 2017 into a comprehensive political and geopolitical crisis of the post–cold war order. And the obvious political implication should not be dodged. Conservatism might have been disastrous as a crisis-fighting doctrine, but events since 2012 suggest that the triumph of centrist liberalism was false too. 50 As the remarkable escalation of the debate about inequality in the United States has starkly exposed, centrist liberals struggle to give convincing answers for the long-term problems of modern capitalist democracy. The crisis added to those preexisting tensions of increasing inequality and disenfranchisement, and the dramatic crisis-fighting measures adopted since 2008, for all their short-term effectiveness, have their own, negative side effects. On that score the conservatives were right. Meanwhile, the geopolitical challenges thrown up, not by the violent turmoil of the Middle East or “Slavic” backwardness but by the successful advance of globalization, have not gone away. They have intensified. And though the “Western alliance” is still in being, it is increasingly uncoordinated. In 2014 Japan lurched toward confrontation with China. And the EU—the colossus that “does not do geopolitics”—“sleepwalked” into conflict with Russia over Ukraine. Meanwhile, in the wake of the botched handling of the eurozone crisis, Europe witnessed a dramatic mobilization on both Left and Right. But rather than being taken as an expression of the vitality of European democracy in the face of deplorable governmental failure, however disagreeable that expression may in some cases be, the new politics of the postcrisis period were demonized as “populism,” tarred with the brush of the 1930s or attributed to the malign influence of Russia. The forces of the status quo gathered in the Eurogroup set out to contain and then to neutralize the left-wing governments elected in Greece and Portugal in 2015. Backed up by the newly enhanced powers of the fully activated ECB, this left no doubt about the robustness of the eurozone. All the more pressing were the questions about the limits of democracy in the EU and its lopsidedness. Against the Left, preying on its reasonableness, the brutal tactics of containment did their job. Against the Right they did not, as Brexit, Poland and Hungary were to prove.

IV

Distance in time, historians like to tell themselves, is a tonic. It permits the detachment and sense of perspective that are commonly touted as virtues of the discipline. But that depends on where time takes you. History writing does not escape the history it attempts to reconstruct. The more pertinent question to ask is not how much time must pass before history can be written, but what has happened in the interim and what, at the time of writing, is expected to happen next. This book, for one, would have been easier to write and might be clearer in its conclusions if it had been finished even closer to the time of the events it begins by describing. It may be easier to write a book like this ten years from now, though given the current train of events, that may be unduly optimistic. Certainly, the tenth anniversary of 2008 is not a comfortable vantage point for a Left-liberal historian whose personal loyalties are divided among England, Germany, the “Island of Manhattan” and the EU. Things could be worse, of course. A ten-year anniversary of 1929 would have been published in 1939. We are not there, at least not yet. But this is undoubtedly a moment more uncomfortable and disconcerting than could have been imagined before the crisis began.

Among the many symptoms of unease and crisis that have afflicted us in the wake of Donald Trump’s victory is the extraordinary uncouth variety of postfactual politics that he personifies. He doesn’t tell the truth. He doesn’t make sense. He doesn’t speak coherently. Power appears to have become unmoored from the basic values of reason, logical consistency and factual evidence. What has caused this degeneration? One can cite a complex of factors. Certainly unscrupulous political demagoguery, the debasement of popular culture and the self-enclosed world of cable TV and social media are part of the problem, as is Trump’s personality. But to attribute our current state of postfactuality to Trump and his cohorts is to succumb only to further delusion. 51 As this book will show, what the history of the crisis demonstrates are truly deep-seated and persistent difficulties in dealing “factually” with our current situation. It isn’t just those denounced as populists who have a problem with truth. It goes far wider and far deeper and it affects the center as much as the margins of mainstream politics. We do not need to go back to the notoriously misleading and incoherent case made for the war against Iraq and its fawning media coverage. It was the current president of the European Commission who announced in the spring of 2011: “When it becomes serious, you have to lie.” 52 At least, one might say, he knows what he’s doing. If we believe Jean-Claude Juncker, a posttruth approach to public discourse is simply what the governance of capitalism currently demands.

The loss of credibility is flagrant and it is comprehensive. The damage goes deep. To say that liberals should simply “pick yourself up, dust yourself off, and start all over again,” as the Depression-era song goes, that if America has failed we should look for leadership to a fresh-faced president of France or the relentlessly reliable chancellor of Germany, is either simple-minded or disingenuous. It does no justice to the scale of the disasters since 2008, or to the failure of the lopsided politics prevailing in both Europe and America to offer an adequate response to the crisis. It does no justice to the extent of our political impasse, with the center and the Right having failed and the Left massively obstructed and self-obstructing. Nor does it acknowledge that some losses are irreparable and that sometimes the appropriate response is not just to keep on going but, instead, to linger for a while, to pick over the ruin of our expectations, to tally up the broken identifications and disillusionments. There is a certain immobility in such an effort at reconstruction. But even as we look back, we can rely on the restless dynamic of global capitalism to force us onward. It is already tugging. As we shall see in the final chapter, the next moments of economic challenge and crisis are already upon us, not in America or in Europe but in Asia and the emerging markets. Looking back is not an act of refusal. It is simply a contribution to the necessary collective effort of coming to terms with the past, of figuring out what went wrong. To do that there is no substitute for digging into the workings of the financial machine. It is there that we will find both the mechanism that tore the world apart and the reason why that disintegration came as such a surprise.

Part I

GATHERING STORM

Chapter 1

THE “WRONG CRISIS”

O n April 5, 2006, the youthful junior senator from Illinois, Barack Obama, took time out from discussion of an India nuclear deal on Capitol Hill to attend the opening of a new think tank project at Brookings. 1 The Brookings Institution is widely regarded as the most influential social science research center in the world. Obama’s Brookings appearance was an audition that would define his presidency. 2 The keynote he delivered was for a new initiative—the Hamilton Project—launched by Robert Rubin, one of the kingmakers of the Democratic Party. Rubin personified the link forged in the 1990s between centrist Democrats and globally minded bankers that reshaped the American economic policy agenda. In 1993 Rubin had moved from his position at the top of Wall Street, as cochairman at Goldman Sachs, to serve as the first head of the National Economic Council, which Bill Clinton had called into existence as a counterpart to the National Security Council. Two years later Rubin was appointed Treasury secretary. Alongside Rubin presiding over the Brookings meeting in April 2006 was a youthful economist by the name of Peter Orszag, also a veteran of the Clinton administration, who would go on to become Obama’s budget director. It was from among the veterans of Rubin’s Treasury that Obama would recruit virtually his entire economics team in 2008. Twelve months ahead of the financial crisis, two and a half years before Obama took office, the launch of the Hamilton Project presents the worldview of some of his most influential advisers in microcosm. It reveals both what they could see and what they could not.

I

Having returned to the business world in 1999, Rubin was worried about the drift in Washington. Globalization had been the central challenge of the 1990s. In the new millennium it was even more so. But two years into President Bush’s second term, the policies of the Republican administration were putting America at risk. Rather than mitigating the pressures of global competition, they were dividing American society. This risked provoking both an antiglobalization backlash and a catastrophic financial crisis that would call into question America’s monetary stability and the global standing of the dollar.

Not that Rubin and his circle were doing badly out of a world of globalization. After the Treasury, Rubin had retired to an influential sinecure as a nonexecutive chairman of the board at Citigroup. Orszag, who started his career bouncing back and forth among academia, government and consulting, would in due course end up at Citigroup too. But for average Americans the story was different. There had been good moments. The Clintonites still celebrated the 1990s and the twin booms of tech and Wall Street. But since the 1970s wages had not kept up with productivity. For the meritocrats of the Hamilton Project it was clear where the finger of blame pointed. America’s schools were failing to give its young people the education essential to stay ahead of the game. The first reports issued by the Hamilton Project bristled with proposals to improve the recruitment of teachers and make better use of kids’ summer vacations. 3 It was the kind of nuts-and-bolts, “evidence-based,” nonideological approach to productivity improvement that dominated economic policy discussion of the era. Its purpose, however, was eminently political. As Obama put it in his keynote:

“When you invest in education and health care and benefits for working Americans, it pays dividends throughout every level of our economy. . . . I think that if you polled many of the people in this room, most of us are strong free traders and most of us believe in markets. Bob [Rubin] and I have had a running debate now for about a year about how do we, in fact, deal with the losers in a globalized economy. There has been a tendency in the past for us to say, well, look, we have got to grow the pie, and we will retrain those who need retraining. But, in fact, we have never taken that side of the equation as seriously as we need to take it. . . . Just remember . . . [t]here are people in places like Decatur, Illinois, or Galesburg, Illinois, who have seen their jobs eliminated. They have lost their health care. They have lost their retirement security. . . . They believe that this may be the first generation in which their children do worse than they do.” 4

This was a betrayal of the American Dream of endless uplift, and that risked spilling over into a political backlash. As Obama put it: “Some of that, then, will end up manifesting itself in the sort of nativist sentiment, protectionism, and anti-immigration sentiment that we are debating here in Washington. So there are real consequences to the work that is being done here. This is not a bloodless process.” 5

Amid the fears about globalization and the risk of populist revolt already evident in 2006, there was one note of economic nationalism that Obama himself was not afraid to strike: “When you keep the deficit low and our debt out of the hands of foreign nations, then we can all win.” Alongside global competitiveness, the other preoccupation that defined the Hamilton team was the question of debt.

As Clinton’s Treasury secretary, Robert Rubin’s great boast was to have turned the deficits of the Reagan era into substantial budget surpluses. Since then under the Republicans, America was headed fast in the wrong direction. In June 2001, in the wake of the dot-com bust and a disputed election, the Bush administration had delivered a tax cut estimated to cost the federal government $1.35 trillion over ten years. 6 This paid off key constituencies, but it also wiped out Rubin’s surpluses and it did so deliberately. The Republicans had convinced themselves that surpluses tended to encourage more government spending. Their approach was the obverse, what Republican strategists of the Reagan era first dubbed “starving the beast.” 7 By entrenching tax cuts and courting a fiscal crisis they would create an irresistible imperative to slash spending, curb entitlements to social welfare and shrink the footprint of government.

The problem was that the spending cuts that were supposed to follow the tax cuts never happened. The terrorist attack of September 11, 2001, put America on a war footing. The Bush administration responded with a huge surge in defense and security spending. In a manner horribly reminiscent of Vietnam, it then plunged America into the Iraq quagmire. In 2006, as the Hamilton group met, Iraq was on the edge of a bloody sectarian civil war. The question now was how to get out. Iraq was not only demoralizing and humiliating. It was also hugely expensive. The Bush administration did its best to keep the costs of the war off the regular budget. So a cottage industry of Democratic Party experts set itself to doing the sums. By 2008 the bill for Afghanistan and Iraq alone was at least $904 billion. Less conservative estimates put the bill as high as $3 trillion. It was certainly more than the United States had spent on any war since World War II. 8

Of course it could have been paid for. 9 America was far richer than it was at the time of Pearl Harbor. But the Bush administration was not only not going to reverse its tax cuts; in May 2003 it doubled down, introducing a further round of tax relief. Given that the military budget was sacrosanct and the rest of discretionary expenditure was not large enough to make a difference, the Republicans proposed to close the gap with grossly inequitable cuts to welfare “entitlements.” Those, however, could not pass the Senate, where the Republican majority was wafer thin and “moderates” held the balance. It was this logjam that turned Rubin’s budget surplus of $86.4 billion in 2000 into a record deficit of $568 billion in 2004 with no end in sight. 10

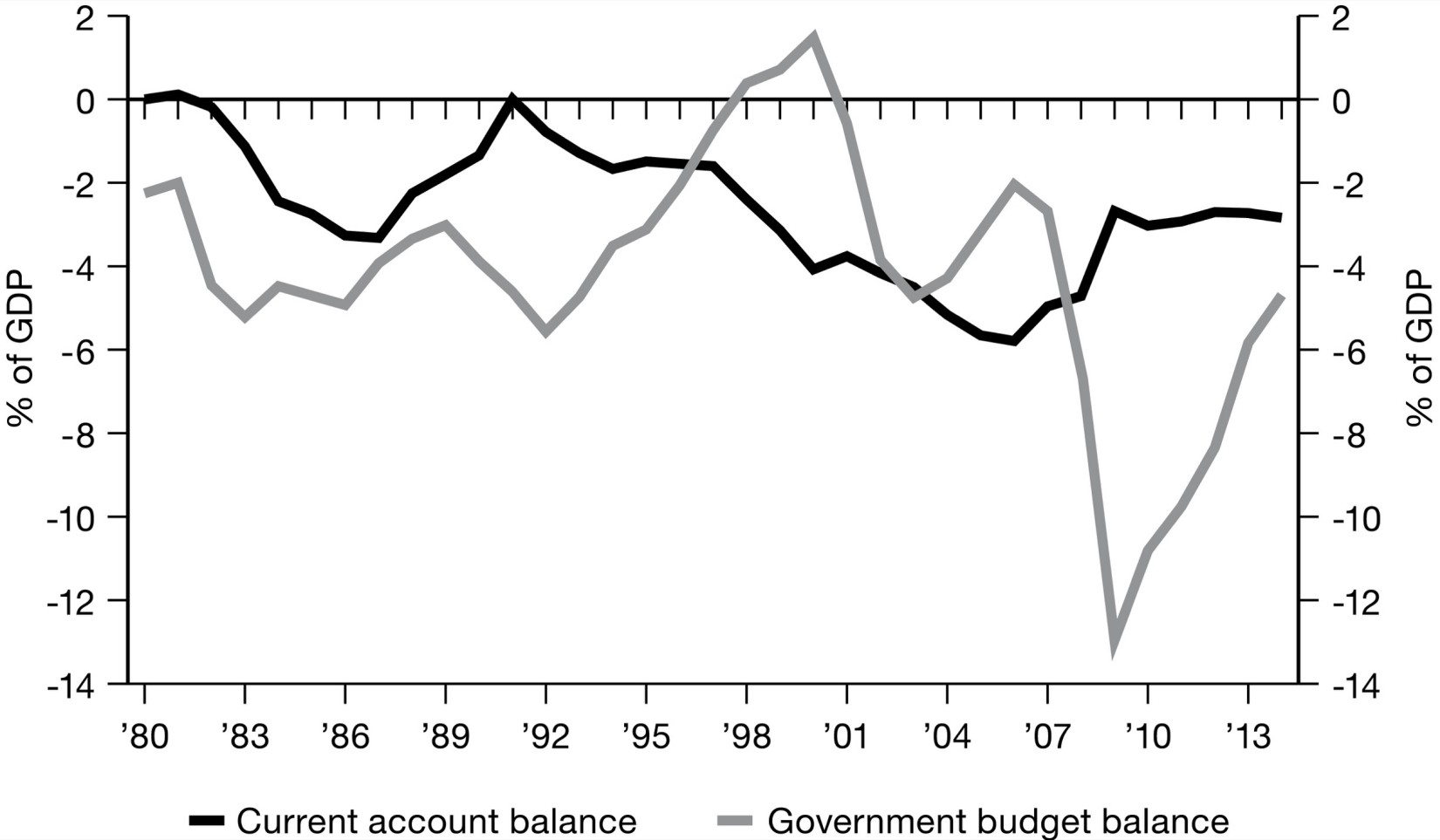

American’s Twin Deficits

Sources: Office of Management and Budget and Bureau of Economic Analysis.

The original inspiration for the Hamilton Project was a paper written in 2004 by Orszag and Rubin sounding the alarm. 11 First, the Bush deficits would drive up interest rates and squeeze private investment. Further down the line lurked a far more serious scenario. “Substantial deficits projected far into the future can cause a fundamental shift in market expectations and a related loss of confidence both at home and abroad,” Rubin and Orszag drily remarked. “The unfavorable dynamic effects that could ensue are largely if not entirely excluded from the conventional analysis of budget deficits. This omission is understandable and appropriate in the context of deficits that are small and temporary; it is increasingly untenable, however, in an environment with deficits that are large and permanent. Substantial ongoing deficits may severely and adversely affect expectations and confidence, which in turn can generate a self-reinforcing negative cycle among the underlying fiscal deficit, financial markets, and the real economy.” Conventional analysis, in short, was not sufficiently alarmist. What it did not “seriously entertain” was the possibility that America was headed toward “fiscal or financial disarray.”

Veterans of the Clinton administration knew what they were talking about when they invoked a “negative cycle” of “underlying fiscal deficit, financial markets, and the real economy.” This, in their view, is what they had inherited from the high-spending Reagan and Bush administrations. In 1993, faced with a bond market sell, Clinton had shelved ambitious plans for a stimulus. 12 Egged on by Rubin and Fed chair Alan Greenspan, deficit reduction became a mantra of the Clinton team. Chief political adviser James Carville was left to ruminate: “I used to think if there was reincarnation, I wanted to come back as the president or the pope or a .400 baseball hitter. But now I want to come back as the bond market. You can intimidate everybody.” 13

In the 1980s and 1990s, the so-called bond vigilantes had their day in the sun. Ten years later they were still in the market. Indeed, the bond funds were bigger than ever. But, as Obama had hinted, domestic investors were not what most worried the Rubinite crowd. Foreign investors were the key concern. The Bush administration’s deficits were financed overwhelmingly by bond buying from abroad. As Orszag and Rubin’s paper remarked, United States Treasurys were still seen as the safest investment in the world. There was no chance of default or a sudden burst of inflation. “But if that expectation were to change and investors had difficulty seeing how the policy process could avoid extreme steps, the consequences could be much more severe than traditional estimates suggest.” Nor was it just the Clinton crowd that worried. In 2003 the nonpartisan Congressional Budget Office saw fit to remind its audience of an extreme scenario in which foreign investors stopped buying US securities, the dollar plunged and interest rates and inflation shot up. “Amid the anticipation of declining profits and rising inflation and interest rates, stock markets could collapse and consumers might suddenly reduce their consumption. Moreover, economic problems in the United States could spill over to the rest of the world and seriously weaken the economies of US trading partners.” 14

The scale of America’s deficits made it vulnerable to bond market pressure. The fact that foreign investors might suddenly turn away from Treasurys evoked the nightmare of a sudden stop to external financing of America’s imbalances. But it was the identity of the foreign investors that infused the scenario with real terror. Until the 1980s the major foreign investors in the United States had been European. Then Japan, with its giant trade surpluses, had taken over. Still, in the new century it was one of America’s largest creditors. But in the 1990s, with a surging yen and a domestic economy crippled by a devastating real estate bust, Japan’s competitive threat had faded. Since the millennium, globalization had acquired a new Asian face. In April 2006, when Obama spoke about keeping our “debt out of the hands of foreign nations,” everyone knew it was China and its Communist regime that he was talking about.

II

Since the 1970s China had been a cornerstone of US geopolitics. Nixon and Kissinger had unhinged the fronts of the cold war by breaking China out of the Soviet embrace. Now the Soviet Union had faded from view, and the European theater of the cold war had faded along with it. The Pacific was the new horizon of American power and China the future rival. For the first time since the rise of Nazi Germany, the United States faced a power that was, at one and the same time, a potential geopolitical competitor, a hostile political regime type and a capitalist economic success story. The fact that Obama came to the Brookings meeting from talks about a nuclear deal with India was a telling coincidence. America was looking for new allies in Asia. But what mattered more than nukes, at least as far as the Hamilton crowd was concerned, was economics.

The Clinton administration had midwifed China into globalization. In November 1995, Washington encouraged Beijing’s application to join the newly founded World Trade Organization (WTO). America had done this before, of course, with Western Europe after 1945, with Japan and East Asia in the 1950s and 1960s and with Eastern Europe in the 1990s. Opening markets was good for American business, for American investors and for American consumers. America’s economic interests were so widespread that they were de facto identical with global capitalism. 15 By the mid-1990s Washington had abandoned any frontal challenge to the Chinese Communist regime over human rights, the rule of law or democracy. Instead, globalists of both the Democratic and Republican parties wagered that the powerful and impersonal force of commercial integration would in due time make China into a biddable and congenial “stakeholder” in the world order. 16

China’s growth was spectacular. Huge profits were to be made for American investors. American manufacturers like GM would stake their future on China. 17 After a brief storm over the Taiwan Strait in 1995–1996, diplomatic relations calmed. But China’s sheer size made it a contender. With the Tiananmen crackdown of 1989, the Communist Party had signaled its intent not to abandon its one-party leadership. Since then it had fashioned a popular ideology that was as much nationalist as Communist. 18 If Washington was betting on international trade and globalization to “Westernize” China, the Chinese Communist Party took the other side of the bet. 19 The party’s leaders wagered that supercharged growth would not weaken them but would consolidate their position as the successful helmsmen of their nation’s spectacular comeback. Beijing took advantage of trading opportunities. But it never subscribed to fully open markets. It decided who would invest and on what terms. It controlled movement of funds in and out. That, in turn, allowed the People’s Bank of China to fix its exchange rate, and since 1994 it had done so by pegging against the dollar.